About Indirect Costs

The debate that has continued since the inception of the earned value concepts in the 1960s has been: “Who should report on and analyze the cost variances attributable to indirect costs?”

This blog is the first in the series of blogs to help answer this question. This blog covers a few fundamentals about how indirect cost rates are established to set the stage. Part 2 will discuss how indirect rates are applied and how project personnel display indirect costs for internal or performance reporting. Part 3 will conclude the discussion on the indirect cost variance analysis process. It covers what the EIA-748 Standard for Earned Value Management Systems (EVMS) and related government agency guides have to say on the subject as well as discussing options for determining who is responsible for indirect cost variance analysis.

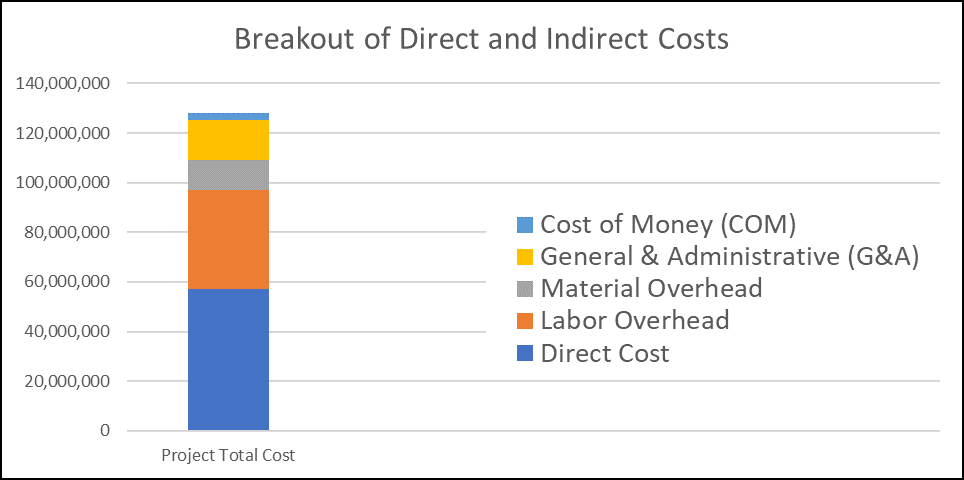

We are frequently asked by our clients who should be responsible for indirect cost variance analysis – and with good reason. When you consider indirect costs (or overheads) are often 100% or more of a project’s direct costs, that means over 50% of in-house work effort is attributable to indirect costs. That’s a major contributor to a project’s total cost, as illustrated in Figure 1.

It also matters to executive management, the customer, project managers, and control account managers (CAMs) when indirect rate changes impact variances to date and estimates at completion (EACs), potentially causing a significant variance at completion or VAC (the VAC is equal to the budget at completion (BAC) minus EAC). While indirect pool managers plan and control indirect costs, project managers and potentially CAMs are required to monitor and control all project costs, whether direct or indirect. They need to understand the root cause of the cost variances to date so they can develop corrective action plans to minimize impacts caused by indirect rate changes and prevent unpleasant surprises.

Because indirect cost pools are so large, a small percentage increase in an indirect cost pool can result in a significant project cost variance that impacts the project’s EAC. For example, a 1% unfavorable indirect cost variance might seem low – certainly not breaking a variance threshold on a particular project because variance percentages are typically established at a level where all costs (direct and indirect) are added together. On a project with $100M in indirect costs, however, that 1% equates to $1M. An unfavorable variance definitely matters to executive management because it impacts a company’s profit margins. It matters to the customer – they may need to modify the project’s scope of work or funding profile when an increase in indirect costs is significant. It also impacts the project manager and the CAMs. When the to-date and forecasted indirect rate increase is significant, they may need to make adjustments at the detail level to reduce their direct cost estimate to complete (ETC) to stay within the project’s contract target cost (CTC).

Who establishes and maintains the indirect cost rates?

Finance or accounting is usually responsible for establishing and maintaining the contractor’s direct and indirect rates. Indirect rates are established for the different “pools” of shared indirect costs applied to the project direct costs, as Figure 1 illustrates.

Indirect costs typically include labor and material overheads, general and administrative (G&A) overheads, and sometimes cost of money (COM). The accounting structure determines the categories of indirect cost applied to the project direct cost elements such as labor, material, subcontract, and other direct costs (ODCs). The pool structure determines how those indirect costs are summarized or displayed for analysis and reporting. These structures are unique to each contractor and how they have set up their accounting system.

Finance and accounting, with the help of executive or functional managers, typically prepare a budget plan for the pools of indirect costs that reflect the contractor’s firm and potential direct business base. This includes the current fiscal year and a set time frame for upcoming fiscal years such as the next three to five years.

Finance or accounting requests the firm and potential business base forecasts from the project offices and business development personnel as part of this indirect cost budget planning process. Proposals with a high probability of winning the contract are incorporated into this calculation. There is often a vice president or functional manager responsible for establishing the indirect pool budget and managing the resources that incur costs related to the pool.

Finance or accounting then produces a Forward Pricing Rate Proposal (FPRP), and eventually a Forward Pricing Rate Agreement (FPRA) is achieved with the appropriate US Government agent. This process of establishing the indirect rates is described in a Cost Accounting Standards Board (CASB) Disclosure Statement or similar accounting procedure. These rates are applied at a very detailed level to the appropriate direct cost elements per the CASB Disclosure Statement. The detailed resource cost elements are summarized into the usual direct cost element categories of labor, material, subcontract, and ODCs for performance analysis and reporting.

Finance or accounting provides the current approved direct and indirect rates to proposal managers for pricing their cost estimates as well as to project managers for establishing Performance Measurement Baselines (PMBs) for any new projects, and for developing project EACs. These current rates are likely to change over time. The current rate is also applied to actual direct costs incurred so as to reflect current cost conditions. These current rates are recorded in the official books of record in the accounting system.

Maintaining and Forecasting the Indirect Cost Rates

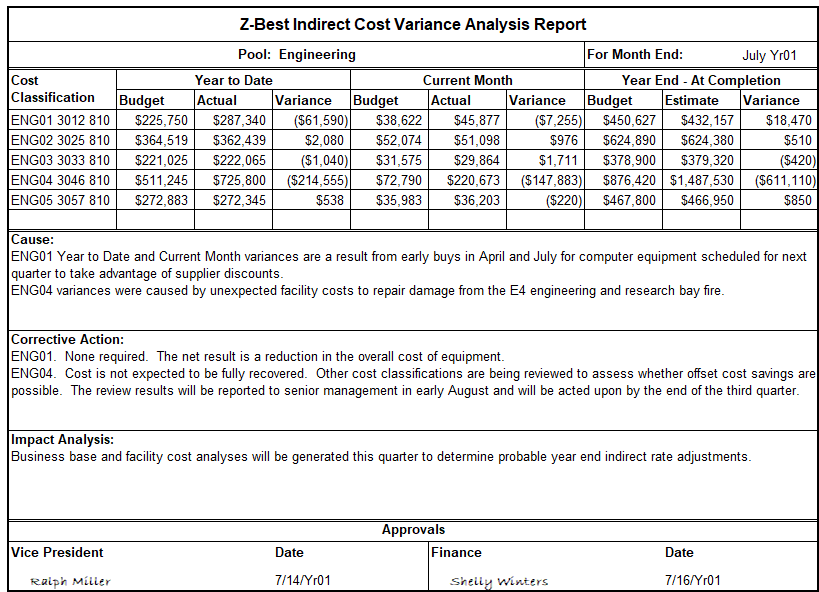

Finance or accounting, with the help of executive or functional managers responsible for the indirect pools, perform routine corporate level indirect cost analysis comparing their indirect cost budget plan to the actual costs. As part of this assessment, they determine whether the current indirect rates are under or over running and require adjustment for the current or upcoming fiscal years. An example of a monthly pool manager’s variance analysis report is illustrated in Figure 2.

The direct and indirect rates are updated on a regular basis, at a minimum annually, sometimes twice a year, or quarterly depending on the contractor. There are a multitude of factors finance and accounting consider when they are assessing whether the rates need to be adjusted. For example:

- Is the business base (or volume) increasing or decreasing? This can impact the percentage of carried indirect costs the projects incur. The business base consists of the existing projects and the sales forecast for new contracts or likely follow-on work effort from existing contracts. An increase or decrease in the business base/volume has a direct impact on when the different types of resources are required as well as on the skill mix of labor resources. As a result of their analysis, executive management may direct human resources (HR) to take specific actions to hire or layoff personnel. Similarly, they may direct procurement to issue purchase orders to suppliers or issue stop work orders to subcontractors.

- Actual costs being incurred in the various indirect cost pools. For example, the company may be experiencing a spike in shipping costs or raw materials. Perhaps employee health care costs or property insurance premiums have increased. Perhaps new pension regulations mean they need to make a one-time adjustment for that set-aside. Executive management may direct the indirect pool managers to take specific actions to mitigate the indirect cost increases.

- Executive and indirect pool management decisions that impact the indirect cost pools. These are in addition to responding to the financial/accounting indirect cost variance analysis. For example, they may decide to sell or purchase a new facility. They may decide to sell off a portion of the business, or acquire another company to pursue additional business. Or, they could direct all employees to cease all nonessential business travel for the current fiscal year.

Any time corporate management adjusts the indirect rates up or down, there is some level of impact to projects. This is conveyed to the project managers in some form, usually with a memorandum of the coming change to the rates that should be used for proposal pricing or project ETCs. The revised rates may also be applied to budget values when the scope of work for future work effort is modified.