Using Earned Value Management (EVM) Performance Metrics for Evaluating EACs

by Humphreys & Associates | May 1, 2023 5:02 am

A previous blog, Maintaining a Credible Estimate at Completion (EAC), discussed why producing a realistic EAC is essential to managing the remaining work on a contract. Internal management and the customer need visibility into the most likely total cost for the contract at completion to ensure it is within the negotiated contract cost and funding limits.

As noted in the earlier blog, one common technique to test the realism of the EAC is to compare the cumulative to date Cost Performance Index (CPI) to the To Complete Performance Index (TCPI).

Example of Using the Metrics for Evaluating Data

One example of documented guidance to industry for evaluating the realism of the EAC is the DOE Office of Project Management (PM) Compliance Assessment Governance (CAG) 2.0, and the related DOE EVMS Metric Specifications they use to assess the quality of schedule and cost data. This blog highlights the use of this guidance and how any contractor can incorporate similar best practices to verify EACs at a given WBS element, control account, or project level are realistic.

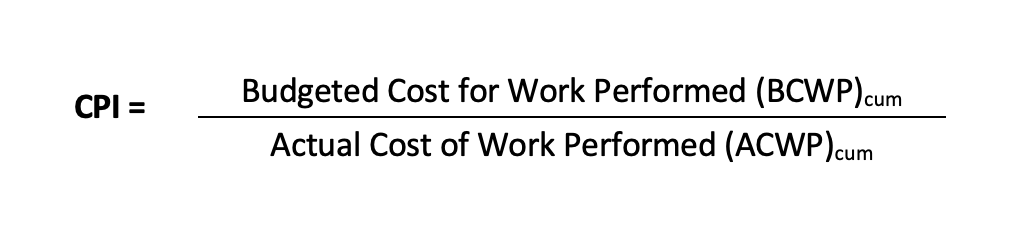

To refresh, the CPI is the efficiency at which work has been performed so far for a WBS element, control account, or at the total project level. The formula for the cumulative to date CPI is as follows.

Best practice tip: To ensure a valid CPI calculation, verify the BCWP and ACWP are recorded in the same month for the same work performed.

The TCPI provides the same information, however, it is forward looking. While the CPI is the work efficiency so far, the TCPI is the efficiency required to complete the remaining work to achieve the EAC. The formula for the TCPI is as follows.

Best practice tip: To ensure a valid TCPI, verify the BCWP and ACWP are recorded in the same month for the same work performed, and the BAC and EAC are for the same work scope. In other words, the scope of work assumptions are the same for the budget and remaining cost. This is why anticipated changes should not be included in the EAC.

The DOE uses the CPI in two of their assessment metrics and the TCPI in one, however, these are critical metrics partly because they are the only ones used to assess two different data evaluations: 1) commingling level of effort (LOE) and discrete work, and 2) EAC realism.

Commingling LOE and Discrete Work

The first use of CPI (no TCPI in this metric) falls under the Budgeting and Work Authorization subprocess. The primary purpose is to evaluate the effect of commingling LOE and discrete work scope has on control account metrics. The basic premise for this metric is that if the CPI for the LOE scope is significantly different than that for the discrete, the mixture of LOE in that control account is likely skewing overall performance reporting.

Here is the formulation DOE uses.

Source URL: https://blog.humphreys-assoc.com/evm-performance-metrics-evaluating-eacs/