Indirect Cost Variance Analysis Process

The debate that has continued since the inception of the earned value concepts in the 1960’s has been: “Who should report on and analyze the cost variances attributable to indirect costs?”

This blog is the third in the series of blogs to help answer this question. The first blog covered a few fundamentals about how indirect cost rates are established to set the stage. The second blog discussed how indirect rates are applied and how project personnel display indirect costs for internal or performance reporting. This blog concludes the discussion on the indirect cost variance analysis process. It covers what the EIA-748 Standard for Earned Value Management Systems (EVMS) and related government agency guides have to say on the subject as well as discussing the best option for determining who is responsible for indirect cost variance analysis.

Throughout a project’s execution phase, project managers and control account managers (CAMs) conduct their respective performance analysis at varying levels of detail to identify significant cost and schedule variances as well as variances at completion (VAC). They use variance thresholds to focus on the work elements where challenges or problems are occurring. As needed, they identify the root cause of the variance and determine the best path forward to mitigate or otherwise reduce the impact of an unfavorable variance.

This effort includes performing additional analysis not just by the direct elements of cost (labor, material, subcontract, or other direct costs (ODCs)), but also by the indirect costs applied to those direct cost elements to identify the root cause. For example, the CAMs check for labor variances (rate or efficiency/volume) and material variances (price or usage) to identify any potential issues. As a side note, remember the rates used to calculate earned value are the same rates used for budget values. Likewise, actual costs are collected into the same direct cost elements of cost and indirect cost pools as the budget plan elements of cost. Those actual rates may vary from the budget/earned value rates.

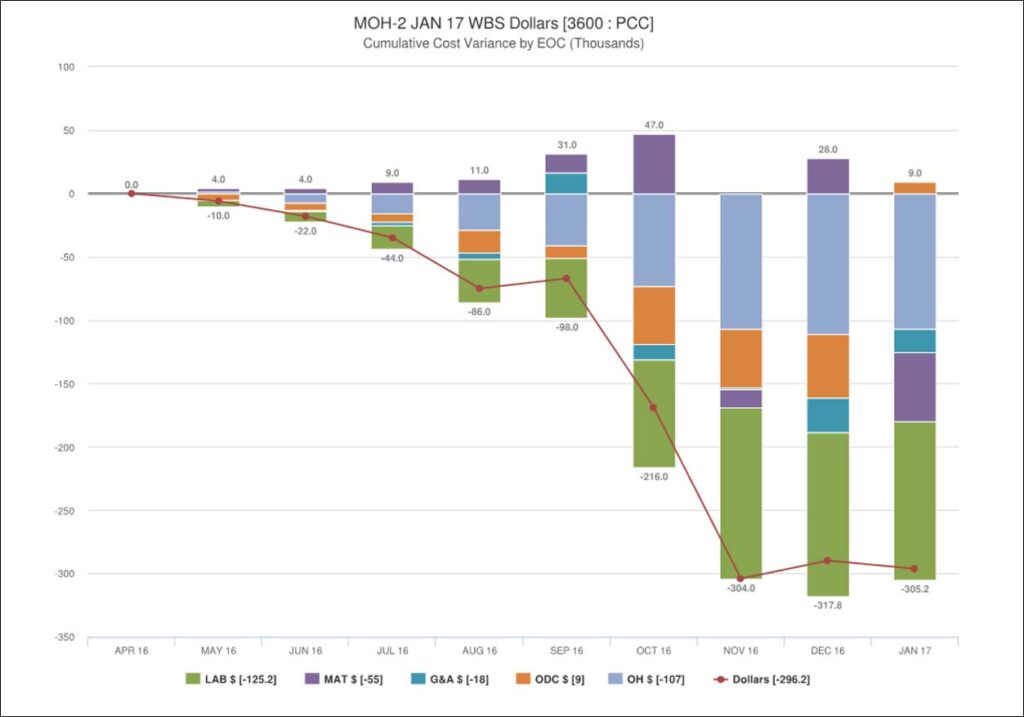

At the total project level, a project manager performs indirect element of cost analysis. They need to assess whether indirect costs are contributing to the project’s cost variances and quantify the impact. Since indirect costs are directly related to the base time phased direct costs, it follows the variances for the element of cost categories are similarly skewed. Figure 1 shows an example (produced from Encore Analytics Empower) of a contract with the variances attributable to the elements of cost (see previous 3-part blog: Planning and Managing EVM by Elements of Cost (EOC)). The indirect cost variances tend to vary with the changes in the direct costs base and/or indirect elements of cost over time at a pool level. While not common, these could be different from month to month (the lightest blue shaded boxes in Figure 1) when annual, semi-annual, or quarterly rate adjustments occur (the project manager would be notified when these occur).

The project manager and CAMs are also responsible for completing their variance analysis reports. These include the Integrated Program Management Report (IPMR) Format 5 (Explanation and Problem Analysis) or Integrated Program Management Data and Analysis Report (IPMDAR) Performance Narrative Report. As part of this analysis, they need to discuss whether rate changes are impacting the project’s current and cumulative cost and schedule variances, as well as the calculated EAC (cumulative to date actual costs plus ETC).

Customers often require additional indirect cost detail on the formal performance reports when thresholds are exceeded. The narrative reports are used to address those indirect cost pool base versus rate variances. Project managers and CAMs (when indirect costs are displayed as part of their budgets), need base versus rate variance analysis from finance or accounting. Finance or accounting is responsible for establishing the indirect cost rates to date and forecasting what the indirect rates will be for future fiscal years.

Who is responsible for the indirect cost variance analysis?

Back to our original question: “Who should report on and analyze the cost variances attributable to indirect costs?” Can the EIA-748 Standard for Earned Value Management Systems (EVMS) 32 guidelines provide any guidance? There are also various government agencies that place EVMS requirements on contracts. Do their policies, compliance business practices, or standard operating procedures provide any guidance?

The fact is, the EIA-748 Guidelines, dating back to the Cost/Schedule Control Systems Criteria (C/SCSC) in the 1960s, have never specified the level where the management and analysis of indirect costs must occur. The founders of the earned value concept realized there are several levels of management where indirect rates are applied versus the level at which they are displayed for management.

The EIA-748 Standard for EVMS (Rev D) Guidelines say the following:

4. Identify the organization or function responsible for controlling overhead (indirect costs). 13. Establish overhead budgets for each significant organizational component of the company for expenses, which will become indirect costs. Reflect in the program budgets, at the appropriate level, the amounts in overhead pools that are planned to be allocated to the program as indirect costs. 19. Record all indirect costs which will be allocated to the program consistent with the overhead budgets. 24. Identify budgeted and applied (or actual) indirect costs at the level and frequency needed by management for effective control, along with the reasons for any significant variances.

The Defense Contract Management Agency (DCMA) Cross Reference Checklist (CRC) sub-questions for these guidelines do not specify any particular level where these actions must occur, and do not even mention the control account level. For example, for the Guideline 4 sub-questions, they reference “the management position” assigned the responsibility and authority for controlling indirect costs. For one of the Guideline 24 sub-questions, they ask: “Are the variances between budgeted and actual indirect costs identified and analyzed at the level of assigned responsibility for their control (indirect pool, department, etc.)?”

Likewise, the Department of Energy’s (DOE) detailed Compliance Review Checklist is equally non-specific on the level of management where these actions occur. Below are excerpts from that DOE document with text highlighted for reference.

| E.1 | E.1 – Indirect Account Organization Structure |

| E.1.1 | Indirect procedures must clearly identify managers who are assigned responsibility and authority for establishing budgets and controlling indirect costs and who have the authority to approve expenditure of resources. |

| E.1.3 | The management process for establishing and controlling indirect cost rates should be documented to ensure responsibility is clear. |

| E.2 | E.2 – Indirect Budget Management |

| E.2.2 | The contractor must establish indirect (i.e., overhead, burden, cost of money, and G&A expense) budgets at the appropriate organizational level for each pool and cost sub‐ element. |

| E.2.3 | Contractor recurring DOE rate performance reviews should be conducted on a regular basis (i.e. monthly, quarterly, etc.) to ensure effective control and management of the indirect expenses and indirect budgets. |

| E.3 | E.3 – Record/Allocate Indirect Costs |

| E.3.2 | Periodically, reviews must be made to assure that indirect costs are being charged to the appropriate indirect pools and by the appropriate incurring organization. |

| E.3.3 | If incurred indirect costs vary significantly from budgets, periodic adjustments must be made to prevent the need for a significant year‐end adjustment. |

| E.4 | E.4 – Indirect Variance Analysis |

| E.4.1 | This guideline requires a monthly documented indirect cost analysis to be performed by those assigned responsibility, comparing indirect budgets to indirect actual costs and explaining the cause of resultant variance(s). |

| E.4.4 | The contractor should define thresholds for each budget category and a process for management by exception for indirect performance and analysis. |

It is not by accident the Guidelines and supporting questions/attributes do not specify any one way all contractors have to manage, analyze, and report on indirect cost variances. Indirect costs can be handled in a number of different ways. The Guidelines have always been designed to give contractors the flexibility to manage their projects within the bounds of those Guidelines.

So, what is a best answer?

While contractors may choose other viable options, a best practice is for the corporate entity responsible for controlling those indirect costs to do the indirect cost variance analysis at the pool levels. They control the rates, know the reason for variances, and can forecast what the rates will be over time. As the first blog in this series pointed out, finance or accounting is responsible for establishing and maintaining the direct and indirect rates based on the contractor’s firm and potential direct business base (or volume).

The designated higher level management entity should also be responsible for providing the necessary indirect cost variance analysis, rate impacts and narrative details to the project managers. The project managers need to be aware of corporate actions and potential indirect rate revisions that impact the range of EACs they need to prepare for the IPMR or IMPDAR submittals. This communication is essential so they have the data and narrative text necessary for managing their project, as well as for producing their performance reports explaining the source and impact of indirect cost variances on the project’s EAC to their customer.

While not a hard requirement, many contractors elect to include both direct and indirect costs in the CAM control account work authorizations. This does not make the CAMs responsible for these indirect costs since they have little to no control over the indirect rates – they simply apply the current or forecast rates that accounting provides. But this format does provide for the necessary visibility CAMs must have regardless in order to conduct the expected variance analysis, inclusive of an assessment of all cost elements (direct and indirect) and price/usage analysis, in order to explain impacts on performance and on their EACs. (See previous blog: EVMS Variance Analysis — EVMS Analysis and Management Reports.) They then forward these to higher level management to incorporate and to provide the rationale for the variances and to determine any corrective action to mitigate the problems.

Another important advantage of providing CAMs fully burdened budgets, earned value, and actual cost data broken out by the direct and indirect cost elements includes but is not limited to facilitating “make to buy” and “buy to make” decisions because a CAM has an apples-to-apples cost comparison as noted in the second blog.

Need help sorting out the best levels for reporting and managing your direct and indirect costs? Call us today at (714) 685-1730.