Incorporating Stop Work Orders Part 2 – Restarting the Work

Updated December, 2020

Stop Work Order (SWO) – Recap of Part 1

A SWO is a temporary suspension of work enabling the customer to re-evaluate the contracted work. The customer has a number of reasons to issue a Stop Work Order:

- A change in mission requirements eliminating the need for some or all of the contract scope,

- A need to complete some or all the work scope within funding limitations.

- Advancement in the state-of-the-art that alters the contract requirements.

- Production or engineering breakthroughs that change the current contractual approach.

- Realignment of programs that changes the emphasis on the current contract.

A Stop Work Order could affect the entire contract or could be focused on a specific deliverable item, component, or function. A key concept about Stop Work Orders is that they are temporary. The Federal Acquisition Regulations envision that Stop Work Orders are resolved within 90 days but allow that the timeframe can be different subject to customer and contractor agreement. The resolution of a Stop Work Order will result in a new contractual direction (a new contractual work order) to:

- Resume the contract (restart the stopped work – unchanged);

- Resume the contract with a revised work approach (technical, schedule, and/or cost);

- Delete a portion of the currently stopped work scope (Delete Work Order); or possibly

- Canceling the entire contract (contract termination order).

Besides Deleting Work Scope, What Else Can Happen with a Stop Work Order (SWO)?

Stop Work Orders, in addition to disrupting contract execution, create much administrative confusion and affect the Performance Measurement Baseline (PMB) in the Earned Value Management System (EVMS). Stop Work Orders typically result in one or more actions:

- Deleting work and its budget from the contract (covered in Part 1 of this article),

- Proposing/negotiating the new course of action,

- Implementing the revised approach in the PMB,

- Proposing/negotiating a Request for Equitable Adjustment, and/ or

- Preparing a framework for making a Claim against the customer.

Part 1 of this SWO article addressed the deleting of work scope and budget from the contract (partial deletion or contract cancelation). This Part 2 of the SWO article addresses the remaining actions involved in restarting the work (either existing or modified scope/ budget).

Stop Work Order (SWO) Decision – Resume Work

The SWO decision by the customer may be to resume the work on the contract – either with the existing scope or with a modified scope (reflecting deleted work or a reworking of the remainder of the contractual effort). Such starting and stopping of work on any contract will have cost impacts on the contractor and any involved subcontractors and vendors, such as:

- Termination costs

- Line shutdown / Startup costs

- Retooling costs

- Personnel costs (lay-off/ rehire)

- Inventory/ storage costs

- etc.

As discussed in Part 1, these costs should be isolated and accumulated by all affected parties in order to establish and justify any Claim or Request for Equitable Adjustment (REA) that may be required as part of the restarting of work.

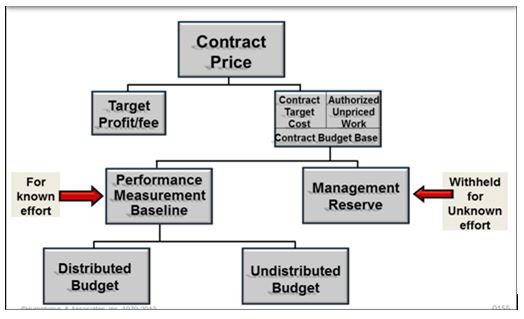

Treat the Stop Work Order as Authorized Unpriced Work (AUW).

The letter from the customer’s contracting officer that initiates the Stop Work Order typically contains direction to take several actions in addition to stopping the effort on some or all of the work scope. First, as indicated above, the customer is engaged in an evaluation exercise to plot a different course for the remaining contracted work. The customer usually requires assistance of the contractor to develop the following:

- Costs associated with what-if studies.

- Addressing revised technical parameters of the end item(s).

- Alternate technical approaches.

- Deliverable item quantity changes, deletions, additions, alternate schedules.

- Alternate funding profiles.

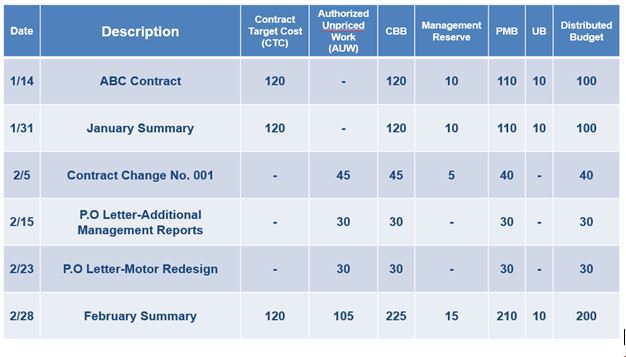

Even if the decision is to restart the work with no change in scope, a 90 day (or longer) delay in the work will likely have an impact on the schedule, cost, and even the technical approach required to complete the work. Since this information is directed by the customer in the Stop Work Order letter, it constitutes Authorized Unpriced Work. Second, the Stop Work Order letter, or a subsequent letter, will likely include a request for a proposal for the revised approach. Production of this proposal is directed by the contracting officer as a result of the Stop Work Order and also constitutes AUW. [NOTE: Contractors often establish a charge number to collect proposal preparation costs, but fail to treat the proposal as a work scope item and establish a budget for the proposal.] Once the contractor has established estimates for the work scope associated with the Stop Work Order, the Contract Budget Base Log should be updated for the Authorized Unpriced Work and included in Undistributed Budget, separately identified from the “stopped work” currently in UB. Alternatively, these costs could be included as part of a Request for Equitable Adjustment (REA) or as part of a legal Claim associated with costs of the SWO action.

Budgets should be distributed for any work associated with, or as a result of, the Stop Work Order.

The contractor should follow its EVMS procedures for authorizing and issuing work scope and budgets for any tasks that result from the Stop Work Order decision. It may be most effective to have a single control account assigned to the contractor program office with multiple work packages/charge numbers for the various tasks.

At various points in the Stop Work Order process, the contractor must wait for the customer.

Upon receipt of the information requested from the contractor, the customer evaluates the information, makes decisions about the contract path forward and/or additional funding, executes contractual actions which could include terminating, modifying, or restructuring the contract. The contractor should continue to track costs of these additional delays and contractual actions for any subsequent REA or Claim actions.

Replanning after Stop Work Order resolution follows the contractor’s EVMS procedures, just as done for the initial planning of the Performance Measurement Baseline (PMB).

In effect, because the contract work was closed out at the cumulative Budgeted Cost For Work Performed (BCWP) value, the Stop Work Order has wiped the slate clean for all future work. In the best case, the customer issues a fully negotiated contract modification when lifting the Stop Work Order; however, the reality is that the customer usually issues an Authorization to Proceed and sets the proposal negotiations for a later date. In either case, EVMS procedures should be followed, whether or not the authorization is unpriced work or a negotiated contract change. The contractor must perform at least the following steps:

- Revise the CWBS, its associated dictionary, and control account structure as necessary,

- Reissue Work Authorizations based on the modified contract,

- Develop the schedule and critical path,

- Plan the control account budgets,

- Issue budgets to Control Accounts for near term work until negotiations for the AUW conclude,

- Establish Management Reserve (as applicable),

- Update logs (CBB, MR, UB).

In summary, responding to the Stop Work Order and restarting the work, the contractor is to follow their EVMS procedures for planning and budgeting. The graphic below provides a roadmap for implementing a Stop Work Order.

within Earned Value Management Systems (EVMS)

The final steps are to continue on with the contract as negotiated through the SWO, and file any required REA for budget/ schedule consideration, or Claims for costs incurred associated with the SWO actions.

Incorporating Stop Work Orders Part 2 – Restarting the Work Read Post »

log")