The Earned Value Management System (EVMS) – Standard Surveillance Instruction (SSI) (latest revision February 2012) defines the Defense Contract Management Agency (DCMA) standardized methodology to conduct contractor surveillance on EVM Systems. This includes assessment of contractor processes and procedures to ensure the 32 EIA-748 Guidelines are being followed when contractually required.

Of the 32 Guidelines, sixteen are considered high-risk or foundational for EVM Systems. This means that if the requirements of those Guidelines are not met, considered noncompliant, the Earned Value Management System may not produce accurate, reliable and auditable data such that it provides the customer with the information necessary to reliably manage a program.

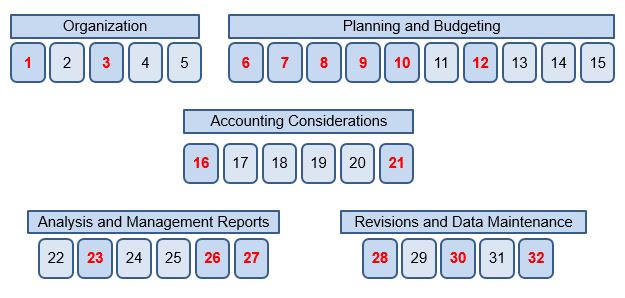

The 16 Foundational Guidelines are highlighted below in red.

Each year, the DCMA prepares a surveillance schedule which includes the five EVMS Areas and associated Guidelines to be reviewed and the programs/contracts involved. Of the 32 Guidelines, the 16 high-risk Guidelines are evaluated every year and all 32 Guidelines evaluated within a 3 year period. By concentrating on these 16 high-risk Guidelines, resources for both the Government and the contractor can be used more efficiently. Concerns with non-high risk Guideline(s) could be surfaced during reviews and these can then be scheduled for additional surveillance. Generally, a minimum of four surveillance events are planned covering the five EVMS Areas in a given year.

If guideline noncompliance were found in any of the high risk guidelines, this signifies that there are shortcomings in the system and the information produced from that system is not reliable for management purposes.

Although the Standard Surveillance Instruction requirements are that those Guidelines that are not foundational be reviewed by the DCMA at least every three years, it is still incumbent on the contractor to ensure that those Guidelines remain compliant.

The 16 foundational guidelines are:

ORGANIZATION

Guideline 1: Define the authorized work elements for the program.

Guideline 3: Provide for the integration of the company’s planning, scheduling, budgeting, work authorization and cost accumulation processes with each other, and as appropriate, the program Work Breakdown Structure (WBS) and the program organizational.

PLANNING AND BUDGETING

Guideline 6: Schedule the authorized work in a manner, which describes the sequence of work and identifies significant task interdependencies required to meet the requirements of the program.

Guideline 7: Identify physical products, milestones, technical performance goals, or other indicators that will be used to measure progress.

Guideline 8: Establish and maintain a time-phased budget baseline, at the Control Account level, against which program performance can be measured.

Guideline 9: Establish budgets for authorized work with identification of significant cost elements (labor, material, etc.) as needed for internal management and for control of subcontractors.

Guideline 10: To the extent it is practical to identify the authorized work in discrete work packages, establish budgets for this work in terms of dollars, hours, or other measurable units.

Guideline 12: Identify and control level of effort activity by time-phased budgets established for this purpose. Only that effort which is immeasurable or for which measurement is impractical may be classified as level of effort.

ACCOUNTING CONSIDERATIONS

Guideline 16: Record direct costs in a manner consistent with the budgets in a formal system controlled by the general books of account.

Guideline 21: For EVMS, the material accounting system will provide for:

- Accurate cost accumulation and assignment of costs to Control Accounts in a manner consistent with the budgets using recognized, acceptable, costing techniques.

- Cost performance measurement at the point in time most suitable for the category of material involved, but no earlier than the time of progress payments or actual receipt of material.

- Full accountability of all material purchased for the program including the residual inventory.

ANALYSIS AND MANAGEMENT REPORTS

Guideline 23: Identify, at least monthly, the significant differences between both planned and actual schedule performance and planned and actual cost performance, and provide the reasons for the variances in detail needed by program management.

Guideline 26: Implement managerial actions taken as a result of earned value information.

Guideline 27: Develop revised estimates of cost at completion based on performance to date, commitment values for material, and estimate of future conditions. Compare this information with the performance measurement baseline to identify variances at completion important to company management and any applicable customer reporting requirements including statements of funding requirements.

REVISIONS AND DATA MAINTENANCE

Guideline 28: Incorporate authorized changes in a timely manner, recording the effects of such changes in budgets and schedules. In the directed effort prior to negotiation of a change, base such revisions on the amount estimated and budgeted to the program organizations.

Guideline 30: Control retroactive changes to records pertaining to work performed that would change previously report amounts for actual costs, earned value, or budgets.

Guideline 32: Document changes to the performance measurement baseline.

For more information on these guidelines or to inquire about EVMS implementation and remediation, contact Humphreys & Associates.

Pingback: EVMS Variance Analysis — EVMS Analysis and Management Reports

Pingback: Summary Level Planning Packages (SLPPs) Misnomer and Alias - Humphreys & Associates