This chapter looks at how risk is evaluated when developing an Earned Value Management System.

Video Contents

You can use the links below to jump to a specific part of the video. 0:00 – A Closer Look at Risk 0:25 – Risk Drives Other Concerns 0:59 – Types of Risk 1:19 – Risk Opportunities 1:38 – Risk Analysis and Selective Controls 1:54 – Balance Cost with Benefit

More EVMS Training

If you liked this video you can purchase the entire course below. This video is an excerpt from the Department of Defense (DOD) version of this eLearning module. We also offer the same course customized for the Department of Energy’s (DOE) specific Earned Value Management (EVM) implementation/requirements, as well as a version of the course customized for NASA’s EVM implementation/requirements.

Not sure what the different requirements are between the DOE and NASA? Can’t remember if Cost and Software Data Reporting (CSDR) is required for an NSA contract? Check out our easy to read Earned Value Management Systems Document Matrix

The debate that has continued since the inception of the earned value concepts in the 1960s has been: “Who should report on and analyze the cost variances attributable to indirect costs?”

This blog is the second in the series of blogs to help answer this question. The first blogcovered a few fundamentals about how indirect cost rates are established to set the stage. This blog discusses how indirect rates are applied and how project personnel display indirect costs for internal or performance reporting. Part 3 concludes the discussion on the indirect cost variance analysis process. It covers what the EIA-748 Standard for Earned Value Management Systems (EVMS) and related government agency guides have to say on the subject as well as discussing the best option for determining who is responsible for indirect cost variance analysis.

There are a number of variables at the project or detail work element level related to indirect costs we often encounter when working with our clients. These variables can influence the level of visibility into how the indirect costs are impacting the project’s total cost. For example:

Accounting may only provide a summary or “wrap” set of direct or indirect rates to the project offices to apply to the project’s base budget or estimate to complete (ETC) values. The rate details may be unknown to project personnel since they are provided a “composite” rate for planning a performance measurement baseline (PMB), actual cost accumulation, and later for estimating ETCs.

The control account level work authorizations may or may not include indirect costs. The control account managers (CAMs) may or may not have visibility into the total cost for the work effort they are responsible for.

The level of detail the customer is requesting the contractor to display the indirect costs for performance reporting.

Applying the Indirect Rates at the Detail Level

The current approved direct and indirect rates are applied at the lowest level where the CAMs are planning their work resource requirements. This is usually at the work package level where the CAMs plan their time phased budget labor hours, material quantities or direct cost, subcontract, or other direct costs (ODCs) that match when the work package activity is scheduled to occur. This helps the CAMs to determine what direct and indirect cost factors make up their total cost for their control account.

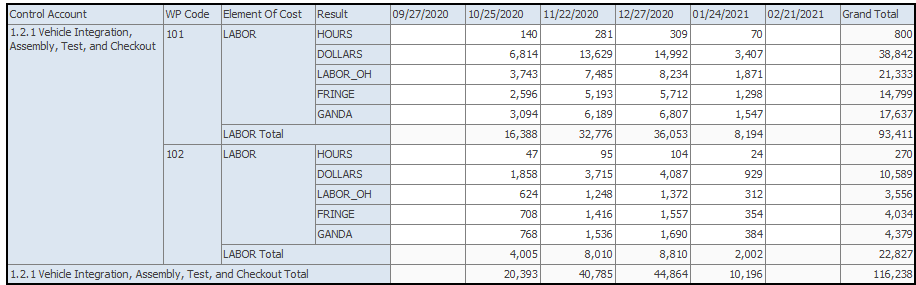

Example Control Account Analysis of Time Phased Direct and Indirect Costs

An example output a CAM could use to analyze their budget time phased element of cost details is illustrated in Figure 1 (produced from ProjStream MaxTeam ). Assuming the CAM has indirect costs in their control accounts, a similar approach is used for their time phased ETC.

Figure 1: Example Control Account Analysis of Time Phased Direct and Indirect Costs

Why is this level of detail useful to the CAMs and project managers? When they are planning to process a baseline change request (BCR) for future work budget, or if they modify their ETC, they can quickly see the impact of changing an element of cost. Examples include switching from make to buy or buy to make, increasing or decreasing hours, changing the duration of an activity, or swapping out labor resources (a different skill mix) on the associated indirect costs.

How Direct and Indirect Costs are Displayed for Use on a Project

While it may seem obvious, it is worthwhile to point out that project personnel:

Do not control how indirect costs are applied. The corporate Cost Accounting Standards Board (CASB) Disclosure Statement or similar accounting procedure controls this. Finance or accounting provides the current set of approved direct and indirect rates the project offices are directed to use.

Do control their base direct costs (labor hours, material quantities or direct cost, subcontract, or ODCs). The approved direct labor rates and indirect rates are applied to these base direct cost values.

Do control how the indirect costs are displayed for internal use or performance reports.

Project direct and indirect cost information can be summarized and displayed at various levels of detail that project personnel can use as needed. The purpose of the following simplified “dollarized” responsibility assignment matrices (RAMs) is to illustrate different ways internal budget data could be displayed to provide some level of visibility into the project’s indirect costs.

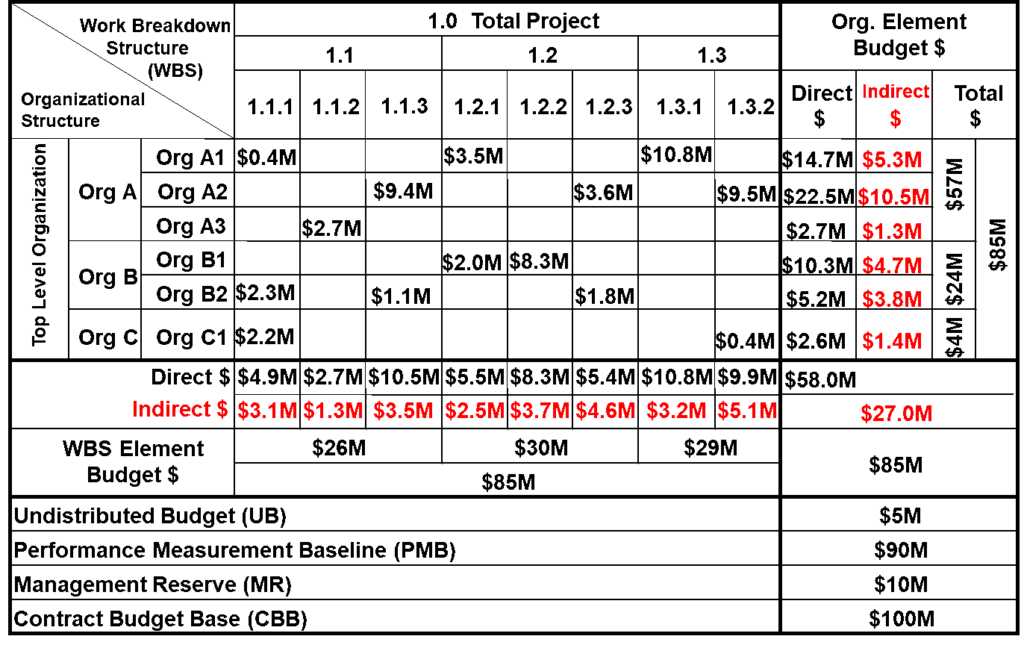

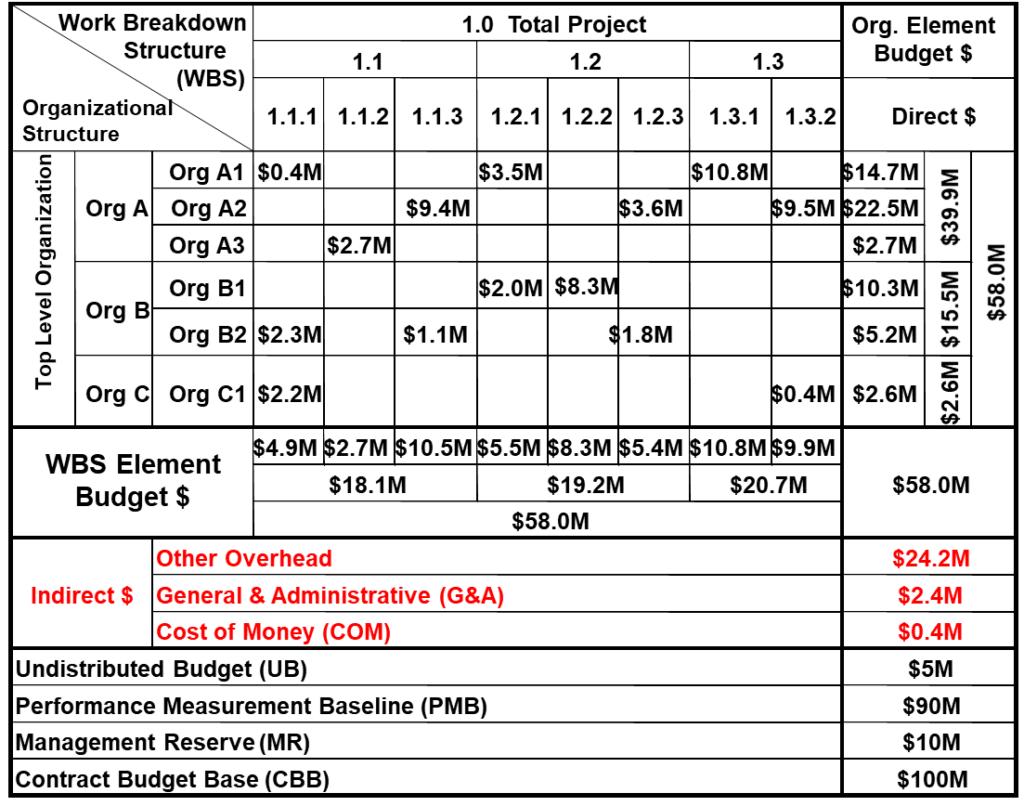

Indirect Costs Displayed at WBS and Organizational Structure Elements

In Figure 2, the total indirect cost amounts are shown at the WBS reporting elements (1.1.1, 1.1.2, etc.), and also by the organizational elements (Org A1, Org A2, etc.). This provides a project manager visibility into the indirect budgets at these levels. What this RAM does not provide visibility into is the different types of indirect costs that make up the total amounts planned. This could include the various categories of the indirect costs so a project manager could compare the amount of labor indirect, material indirect, general and administrative (G&A) indirect, and cost of money (COM) that are contributing to the total amounts planned. When that level of visibility is desired, Figure 3 illustrates an alternate approach.

Figure 2: Indirect Costs Displayed at WBS and Organizational Structure Elements

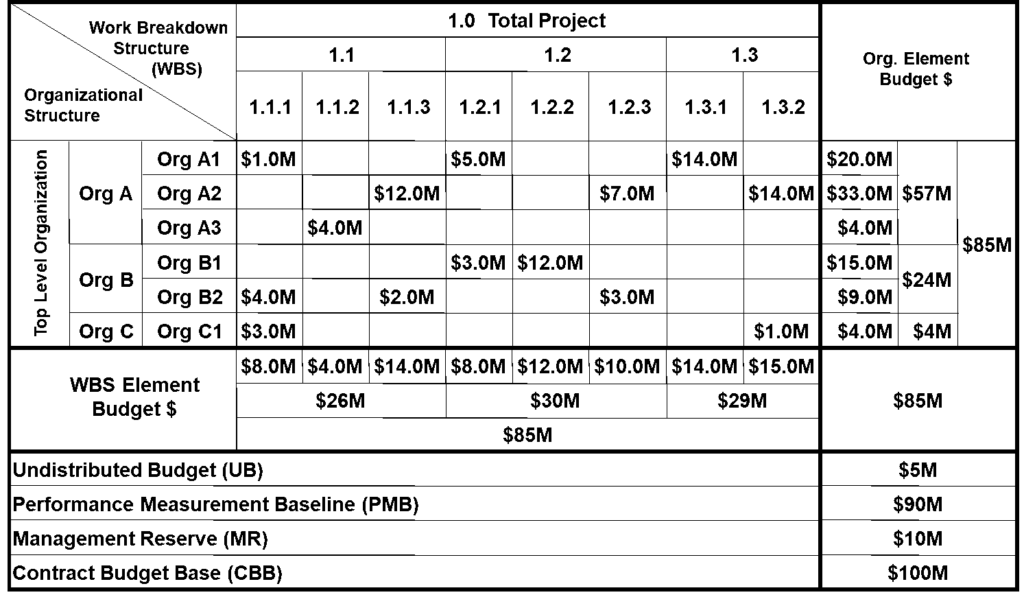

Indirect Costs Displayed at the Total Project Level

Figure 3 does not separate out the indirect costs by WBS elements or organizational elements. Instead, it displays the total amounts for each indirect cost pool (summary lines for other overheads, G&A, and COM). The amounts shown at the control account level are only the direct cost budgets assigned to the CAMs in their work authorization documents, which total $58.0M (shown in the lower right corner). Based on how this data is displayed, the expectation would be the CAMs are managing just their direct cost budgets. This approach (total project level) does not provide visibility into the indirect costs at the various WBS or organizational structure element levels.

Figure 3: Indirect Costs Displayed at the Total Project Level

Fully Burdened RAM

In Figure 4, the entire $85M budget assigned to the CAMs is fully burdened (includes direct and indirect costs). This would be reflected in their work authorization documents. Based on how the data are displayed, the expectation would be the CAMs are managing, analyzing, and reporting on not only the direct costs, but also on the indirect costs for their scope of work. This method, however, gives no visibility into how much of each control account is direct cost versus indirect cost in the RAM. It would be necessary to drill down into the detail work package and resource assignment source data to determine the breakout of direct and indirect costs (see Figure 1).

Figure 4: Fully Burdened RAM

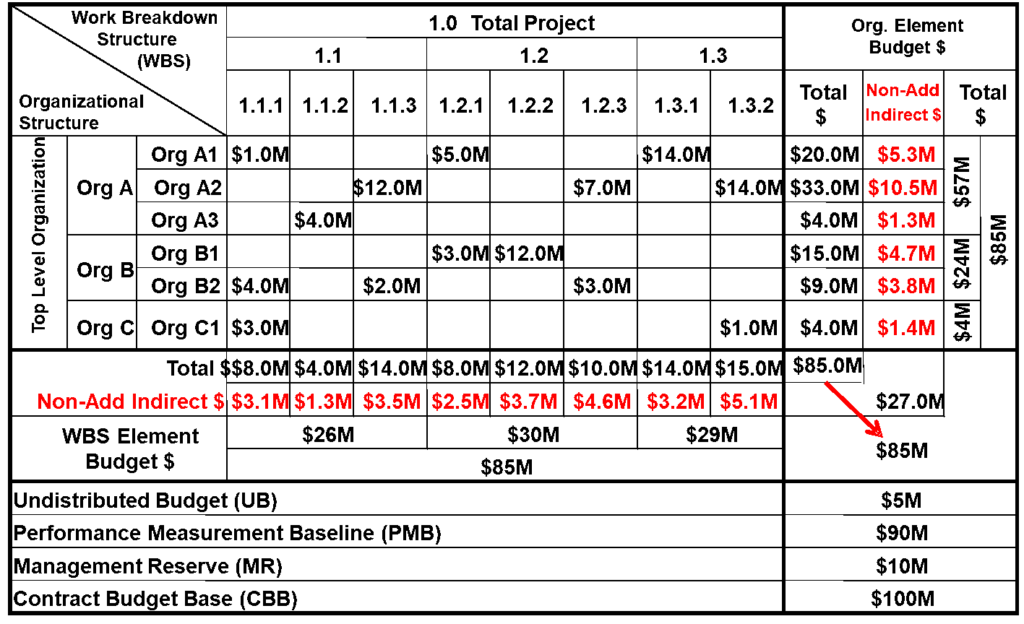

Fully Burdened RAM with Indirect Cost Summaries for WBS and Organizational Elements

What if the project manager takes a different approach to provide some visibility into the indirect costs? In Figure 5, the body of the RAM reflects the fully burdened (direct and indirect budgets) similar to Figure 4. Additionally, it also provides the total indirect cost summary for each major WBS element and organizational element, in what are called “Non-Add” entries.

Figure 5: Fully Burdened RAM with Indirect Cost Summaries for WBS and Organizational Elements

Indirect Cost Details in Project Performance Reports

How the project indirect cost information is summarized and displayed also applies to the formal contract performance reports. Customers often tailor the reporting requirements by specifying how they expect indirect costs to be separated out on the Integrated Program Management Report (IPMR) Formats 1, 2, and 7 or provided in the Integrated Program Management Data and Analysis Report (IPMDAR) Contract Performance Dataset (CPD) for visibility into the project’s direct and indirect costs.

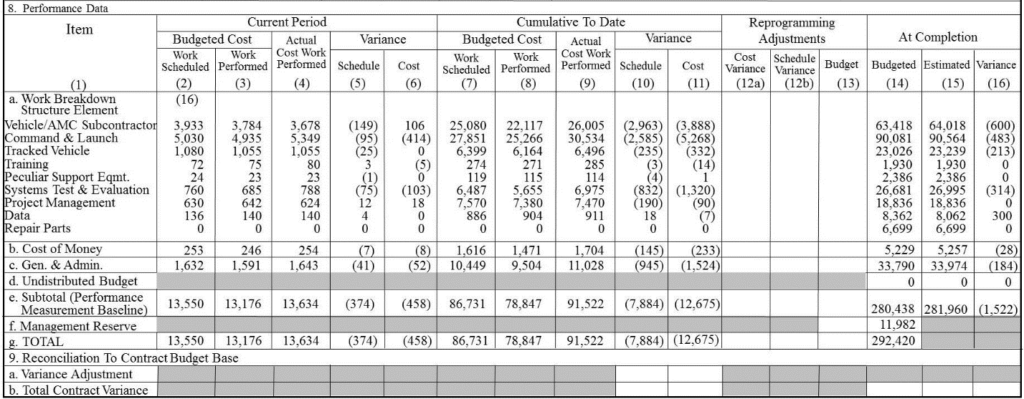

Example Partial IPMR Format 1

For illustration purposes, a partial example IPMR Format 1 is shown in Figure 6. This example illustrates the typical “default” detail in the body of the report (Block 8. Performance Data, a. Work Breakdown Structure Element). The columns include the direct costs plus other overheads (anything other than COM or G&A) for the WBS element rows. Rows 8. b. and 8. c. separate out the COM and G&A indirect costs at the project level.

Figure 6: Example Partial IPMR Format 1

This default layout provides limited visibility into the indirect costs of the project. Should the customer want more visibility into the contribution of the indirect costs on the project, tailoring options we often see specified in a contract include:

The body of the report displays the direct costs for the WBS elements and a summary line is added to provide visibility into indirect costs other than the COM and G&A, which are displayed at the total project level.

Similar to option 1, the body of the report displays the direct costs for the WBS elements. Instead of one summary line for the other indirect costs, there is a summary line for each indirect pool, as defined in the contractor’s CASB Disclosure Statement. For example, an Engineering indirect cost row, Manufacturing indirect cost row, Material indirect cost row, and Service indirect cost row.

For each WBS element in the body of report, there are additional rows that break out the direct cost and the indirect cost categories. Sometimes the direct costs are also broken down into the major element of cost categories such as labor, material, subcontract, and ODC.

When the customer requires additional indirect cost detail in the formal performance reports, note that the applicable narrative report (IPMR Format 5 or the IPMDAR Performance Narrative Report) will need to include a discussion on significant cost variances for those indirect cost categories when applicable. This is discussed further in the next blog.

Part 3 of this series of blogs will discuss the cost and schedule variance analysis process and how to determine who should be responsible for indirect cost variance analysis.

The debate that has continued since the inception of the earned value concepts in the 1960s has been: “Who should report on and analyze the cost variances attributable to indirect costs?”

This blog is the first in the series of blogs to help answer this question. This blog covers a few fundamentals about how indirect cost rates are established to set the stage. Part 2 will discuss how indirect rates are applied and how project personnel display indirect costs for internal or performance reporting. Part 3will conclude the discussion on the indirect cost variance analysis process. It covers what the EIA-748 Standard for Earned Value Management Systems (EVMS) and related government agency guides have to say on the subject as well as discussing options for determining who is responsible for indirect cost variance analysis.

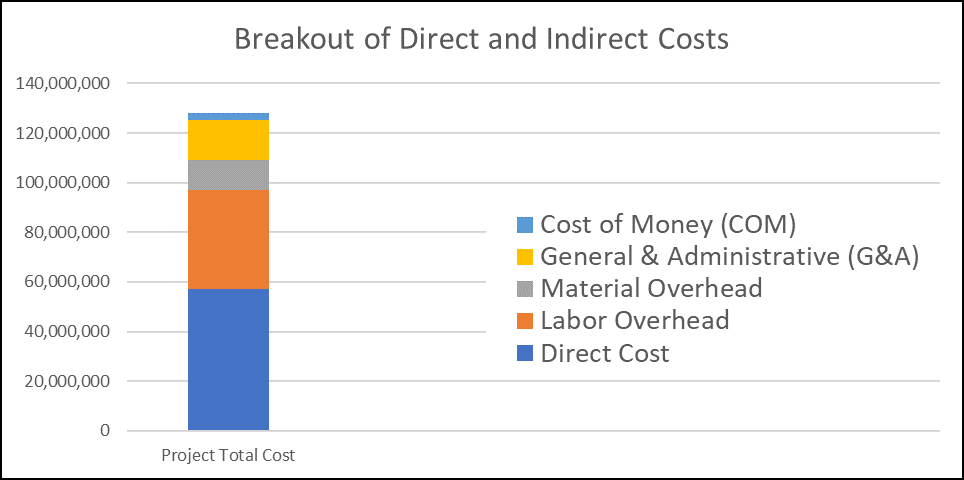

We are frequently asked by our clients who should be responsible for indirect cost variance analysis – and with good reason. When you consider indirect costs (or overheads) are often 100% or more of a project’s direct costs, that means over 50% of in-house work effort is attributable to indirect costs. That’s a major contributor to a project’s total cost, as illustrated in Figure 1.

Figure 1: Example of how indirect costs often contribute over 50% of in-house project’s total cost

It also matters to executive management, the customer, project managers, and control account managers (CAMs) when indirect rate changes impact variances to date and estimates at completion (EACs), potentially causing a significant variance at completion or VAC (the VAC is equal to the budget at completion (BAC) minus EAC). While indirect pool managers plan and control indirect costs, project managers and potentially CAMs are required to monitor and control all project costs, whether direct or indirect. They need to understand the root cause of the cost variances to date so they can develop corrective action plans to minimize impacts caused by indirect rate changes and prevent unpleasant surprises.

Because indirect cost pools are so large, a small percentage increase in an indirect cost pool can result in a significant project cost variance that impacts the project’s EAC. For example, a 1% unfavorable indirect cost variance might seem low – certainly not breaking a variance threshold on a particular project because variance percentages are typically established at a level where all costs (direct and indirect) are added together. On a project with $100M in indirect costs, however, that 1% equates to $1M. An unfavorable variance definitely matters to executive management because it impacts a company’s profit margins. It matters to the customer – they may need to modify the project’s scope of work or funding profile when an increase in indirect costs is significant. It also impacts the project manager and the CAMs. When the to-date and forecasted indirect rate increase is significant, they may need to make adjustments at the detail level to reduce their direct cost estimate to complete (ETC) to stay within the project’s contract target cost (CTC).

Who establishes and maintains the indirect cost rates?

Finance or accounting is usually responsible for establishing and maintaining the contractor’s direct and indirect rates. Indirect rates are established for the different “pools” of shared indirect costs applied to the project direct costs, as Figure 1 illustrates.

Indirect costs typically include labor and material overheads, general and administrative (G&A) overheads, and sometimes cost of money (COM). The accounting structure determines the categories of indirect cost applied to the project direct cost elements such as labor, material, subcontract, and other direct costs (ODCs). The pool structure determines how those indirect costs are summarized or displayed for analysis and reporting. These structures are unique to each contractor and how they have set up their accounting system.

Finance and accounting, with the help of executive or functional managers, typically prepare a budget plan for the pools of indirect costs that reflect the contractor’s firm and potential direct business base. This includes the current fiscal year and a set time frame for upcoming fiscal years such as the next three to five years.

Finance or accounting requests the firm and potential business base forecasts from the project offices and business development personnel as part of this indirect cost budget planning process. Proposals with a high probability of winning the contract are incorporated into this calculation. There is often a vice president or functional manager responsible for establishing the indirect pool budget and managing the resources that incur costs related to the pool.

Finance or accounting then produces a Forward Pricing Rate Proposal (FPRP), and eventually a Forward Pricing Rate Agreement (FPRA) is achieved with the appropriate US Government agent. This process of establishing the indirect rates is described in a Cost Accounting Standards Board (CASB) Disclosure Statement or similar accounting procedure. These rates are applied at a very detailed level to the appropriate direct cost elements per the CASB Disclosure Statement. The detailed resource cost elements are summarized into the usual direct cost element categories of labor, material, subcontract, and ODCs for performance analysis and reporting.

Finance or accounting provides the current approved direct and indirect rates to proposal managers for pricing their cost estimates as well as to project managers for establishing Performance Measurement Baselines (PMBs) for any new projects, and for developing project EACs. These current rates are likely to change over time. The current rate is also applied to actual direct costs incurred so as to reflect current cost conditions. These current rates are recorded in the official books of record in the accounting system.

Maintaining and Forecasting the Indirect Cost Rates

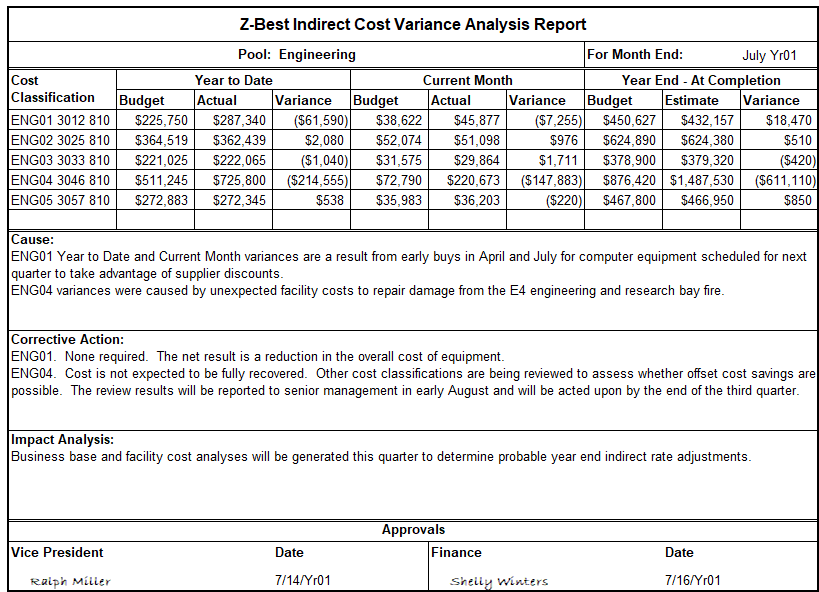

Finance or accounting, with the help of executive or functional managers responsible for the indirect pools, perform routine corporate level indirect cost analysis comparing their indirect cost budget plan to the actual costs. As part of this assessment, they determine whether the current indirect rates are under or over running and require adjustment for the current or upcoming fiscal years. An example of a monthly pool manager’s variance analysis report is illustrated in Figure 2.

Figure 2: Example of a monthly Indirect Cost Variance Analysis Report

The direct and indirect rates are updated on a regular basis, at a minimum annually, sometimes twice a year, or quarterly depending on the contractor. There are a multitude of factors finance and accounting consider when they are assessing whether the rates need to be adjusted. For example:

Is the business base (or volume) increasing or decreasing? This can impact the percentage of carried indirect costs the projects incur. The business base consists of the existing projects and the sales forecast for new contracts or likely follow-on work effort from existing contracts. An increase or decrease in the business base/volume has a direct impact on when the different types of resources are required as well as on the skill mix of labor resources. As a result of their analysis, executive management may direct human resources (HR) to take specific actions to hire or layoff personnel. Similarly, they may direct procurement to issue purchase orders to suppliers or issue stop work orders to subcontractors.

Actual costs being incurred in the various indirect cost pools. For example, the company may be experiencing a spike in shipping costs or raw materials. Perhaps employee health care costs or property insurance premiums have increased. Perhaps new pension regulations mean they need to make a one-time adjustment for that set-aside. Executive management may direct the indirect pool managers to take specific actions to mitigate the indirect cost increases.

Executive and indirect pool management decisions that impact the indirect cost pools. These are in addition to responding to the financial/accounting indirect cost variance analysis. For example, they may decide to sell or purchase a new facility. They may decide to sell off a portion of the business, or acquire another company to pursue additional business. Or, they could direct all employees to cease all nonessential business travel for the current fiscal year.

Any time corporate management adjusts the indirect rates up or down, there is some level of impact to projects. This is conveyed to the project managers in some form, usually with a memorandum of the coming change to the rates that should be used for proposal pricing or project ETCs. The revised rates may also be applied to budget values when the scope of work for future work effort is modified.

This video provides an overview of why Earned Value Management is a benefit to both the company implementing it and their customer.

Video Contents

You can use the links below to jump to a specific part of the video. 0:00 – Introduction 0:12 – EVMS Benefits to Customers 1:01 – EVMS Benefits to Companies 1:54 – Mutual Benefits of Earned Value

More EVMS Training

If you liked this video you can purchase the entire course below. This video is an excerpt from the Department of Defense (DOD) version of this eLearning module. We also offer the same course customized for the Department of Energy’s (DOE) specific Earned Value Management (EVM) implementation/requirements, as well as a version of the course customized for NASA’s EVM implementation/requirements.

Not sure what the different requirements are between the DOE and NASA? Can’t remember if Cost and Software Data Reporting (CSDR) is required for an NSA contract? Check out our easy to read Earned Value Management Systems Document Matrix

Earned Value Consulting

Earned value consulting is a process by which a consultant can help a company to better understand the financial implications of their projects. This understanding can then be used to make more informed decisions about whether or not to undertake a project, and also to ensure that the project is completed as efficiently as possible. The goal of earned value consulting is always to improve the bottom line for the company.

Looking to improve your company’s bottom line? Earned value consulting can help! Our experienced consultants can analyze your project costs and help you make informed decisions about whether or not to undertake a project. We’ll also help you stay on track during the project’s execution, ensuring that it stays within budget and on schedule. Contact us today to request a free consultation.

An overview of Earned Value Guidelines and Objectives. These are the key building blocks for a successful Earned Value Management System.

Video Contents

You can use the links below to jump to a specific part of the video. 0:05 – Helpful Earned Value Management System Elements 0:35 – EIA-748-C EVMS Guidelines 1:22 – EVMS Objectives 2:10 – Policy and Procedures 3:00 – Integrated Baseline Review (IBR)

More EVMS Training

If you liked this video you can purchase the entire course below. This video is an excerpt from the Department of Defense (DOD) version of this eLearning module. We also offer the same course customized for the Department of Energy’s (DOE) specific Earned Value Management (EVM) implementation/requirements, as well as a version of the course customized for NASA’s EVM implementation/requirements.

Not sure what the different requirements are between the DOE and NASA? Can’t remember if Cost and Software Data Reporting (CSDR) is required for an NSA contract? Check out our easy to read Earned Value Management Systems Document Matrix

In our second video in this series, we present an overview of Performance Measurement in an Earned Value Management System.

Video Contents

You can use the links below to jump to a specific part of the video. 0:05 – Earned Value Management Abbreviations used in Performance Measurement 0:39 – Variances in an Earned Value Management System 1:04 – What is Performance Measurement? 1:33 – Performance Measurement Objective 1:52 – Why is Communication the primary objective of Performance Measurement? 3:00 – The Problem of Too Much Data

More EVMS Training

If you liked this video you can purchase the entire course below. This video is an excerpt from the Department of Defense (DOD) version of this eLearning module. We also offer the same course customized for the Department of Energy’s (DOE) specific Earned Value Management (EVM) implementation/requirements, as well as a version of the course customized for NASA’s EVM implementation/requirements.

Not sure what the different requirements are between the DOE and NASA? Can’t remember if Cost and Software Data Reporting (CSDR) is required for an NSA contract? Check out our easy to read Earned Value Management Systems Document Matrix