Master Project Management with Earned Value Training

Embark on a journey to elevate your project management skills with our comprehensive Earned Value Training. This specialized training is meticulously designed to empower organizations and professionals to navigate through the intricate path of project management with precision and expertise.

Unlock the Power of Key Project Metrics

Delve into the core of project management by mastering the pivotal metrics such as Earned Value (EV), Planned Value (PV), and Actual Cost (AC). Our Earned Value Training ensures you gain in-depth knowledge and practical skills to utilize these metrics effectively, enabling you to keep your projects on track, within budget, and adhering to schedules.

Ensure Successful Project Execution with Informed Decisions

Learn how to gauge the health of your projects by deriving insightful data from key calculations and metrics. Our training equips you with the capability to make data-driven, informed decisions that pave the way for successful project execution, even amidst challenges and changing project landscapes.

Equip Your Team with Essential Project Management Skills

With a focus on both theoretical knowledge and practical application, our Earned Value Training is tailored to equip your project teams with the essential skills and knowledge to monitor, control, and steer projects effectively towards their goals while ensuring optimal resource utilization.

Deliver Value While Staying on Budget and Schedule

Immerse yourself in a learning experience that ensures you not only deliver projects that provide value but also ensures that they are executed within the stipulated budget and time frames. Navigate through the complexities of project management and ensure every project you handle is a testament to efficiency and effectiveness.

Enroll Now for a Future in Successful Project Management

Secure your spot in our Earned Value Training and embark on a path to becoming a proficient project manager. Enhance your career, boost your team’s productivity, and ensure every project you manage is executed successfully, adhering to all its planned parameters. Enroll now and steer your projects towards assured success!

This video provides an overview of why Earned Value Management is a benefit to both the company implementing it and their customer.

Video Contents

You can use the links below to jump to a specific part of the video. 0:00 – Introduction 0:12 – EVMS Benefits to Customers 1:01 – EVMS Benefits to Companies 1:54 – Mutual Benefits of Earned Value

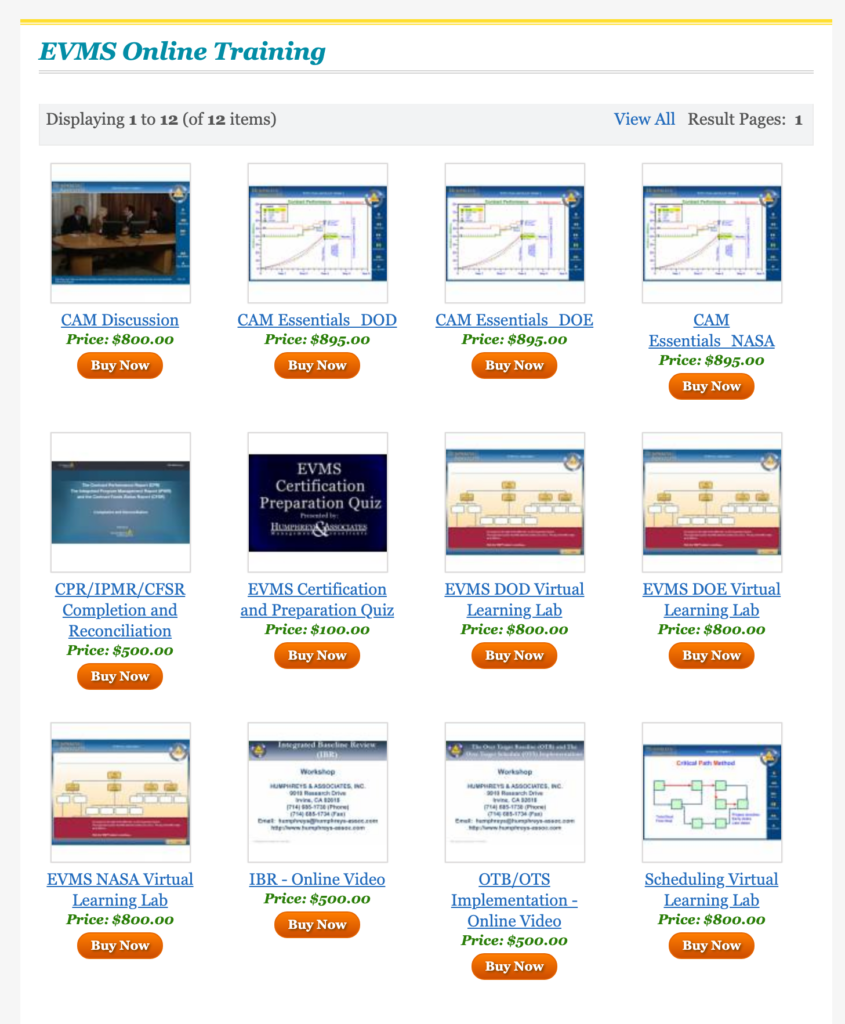

More EVMS Training

If you liked this video you can purchase the entire course below. This video is an excerpt from the Department of Defense (DOD) version of this eLearning module. We also offer the same course customized for the Department of Energy’s (DOE) specific Earned Value Management (EVM) implementation/requirements, as well as a version of the course customized for NASA’s EVM implementation/requirements.

Not sure what the different requirements are between the DOE and NASA? Can’t remember if Cost and Software Data Reporting (CSDR) is required for an NSA contract? Check out our easy to read Earned Value Management Systems Document Matrix

Earned Value Consulting

Earned value consulting is a process by which a consultant can help a company to better understand the financial implications of their projects. This understanding can then be used to make more informed decisions about whether or not to undertake a project, and also to ensure that the project is completed as efficiently as possible. The goal of earned value consulting is always to improve the bottom line for the company.

Looking to improve your company’s bottom line? Earned value consulting can help! Our experienced consultants can analyze your project costs and help you make informed decisions about whether or not to undertake a project. We’ll also help you stay on track during the project’s execution, ensuring that it stays within budget and on schedule. Contact us today to request a free consultation.

Do any (or many) of these situations apply to you?

The Project has to comply with the EIA-748 EVMS Standard! What is that? How do we do that?

You have a new contract of over $20 Million, and you need to get yourself, your staff, and all the Project personnel up to speed on your new contractual Earned Value requirement.

The RFP says the company must have an Earned Value Management (EVM) certification. How can we respond to the RFP?

Your contract is over $100 Million and now you must have and demonstrate a Certified Earned Value Management System (EVMS). How do you do that?

How do you get a compliant EVMS Description in the first place?

You reviewed company training materials and everything dealing with Earned Value is out of date; and it is going to cost thousands to update the materials and keep them up to date!

What are Control Account Managers (CAMs)? Must we have CAMs to do Earned Value? How do I get CAMs/Train them?

I used to have great CAMs, but none of my new CAMs can spell EV. How do I train them?

You Are Not Alone

If you answered “yes” to any of these, don’t feel like the Lone Ranger. Even though the Earned Value concept has been around for over 50 years, the requirement can still be new to your company, new to your contract, and new to your employees. Most will not have learned EVM in college. Even companies that have been using EVM for years face a recurring need for training. We’re pretty consistently seeing a turnover of 20-40% of our experienced CAMs each year across the industry.

If you answered “yes” to several, I’m sure you’re a bit overwhelmed and asking yourself, how can we possibly meet all these requirements?

H&A has trained over 950,000 people around the world in all aspects of the Earned Value requirements and has built the largest, most comprehensive library of training materials in the Earned Value Management consulting industry. We have tailored training materials and have trained and supported contractors whose customers have been from DOD, DOE, NASA, FAA, HHS, as well as international customers such as the Australian DOD, the Canadian DND, Sweden Defense, and the UK.

Basic and Advanced Courses in Earned Value Management and

Control Account Manager/Project Controls Staff Training and Certification;

EVMS Review training to prepare upper management and project teams for:

Earned Value Management System Review,

Integrated Baseline Review (IBR), and

Internal/Joint/External Surveillance;

Specialized training in:

Developing a WBS,

Planning Techniques,

Project Scheduling,

Baseline Establishment,

Materials Management,

Subcontract Management,

Basic and Advance Variance Analysis,

Estimating,

Change Management,

Government Reporting requirements,

OTB/ OTS incorporation, and

Agile Software Development

Real-World Application

Our curriculum makes extensive use of real-world examples and case studies to extend the process of learning into application. We offer these hands-on courses in a variety of settings and formats to meet your needs.

Public offerings are open to the industry at large and are particularly useful when you have a limited number of individuals needing the training or those individuals who are widely geographically separated.

In-house offerings at your facilities allows us to meet the training need at one location or for one specific team and can include specifics of your system description.

Earned Value Webinars

Webinar offerings of the two courses above and our Virtual Learning Lab (VLL) format are available, especially in these times of limited travel. Webinars of the public and in-house training courses rely on the same content as the in-person courses with the addition of virtual interaction opportunities to increase student involvement and enhance learning. Our Virtual Learning Lab (VLL) format provides an opportunity for busy individuals to learn at their own pace and time of their choice – even if they are working from home. The VLL makes extensive use of video presentations and application case studies to enhance the learning environment and ensure the students continue to apply the knowledge they have gained.

Training Materials

If you have an existing training staff, H&A can even be your source for training materials. Most of our courses are available for purchase/licensing and our staff of EVMS experts can tailor them to any company environment. The big benefit here is you leveraging H&A active involvement with EVM requirement changes to keep the material up to date and your training staff don’t have to do it. In the end you get an up-to-date course without out committing the staff and costs to do the work. This approach also aligns your material across all our offerings to provide you delivery flexibility with a consistent core content.

In addition to providing course materials, H&A also can provide Train-The-Trainer sessions in those courses, so your company’s training department can understand and become comfortable with the training materials and updates.

EVMS Certification Programs

Our Certification programs go beyond the public or in-house training courses to create the Qualified CAMs and Project Controls (PC) personnel that are integral parts of a successful EVMS implementation. These roles are where “the rubber meets the road” for EVMS. CAMs and PCs will be expected to demonstrate how the company’s EVM System is actually operating on a day-to-day basis. H&A offers comprehensive and rigorous Certification Courses for both of these important functions so you can be assured that your people not only understand Earned Value concepts but have demonstrated the ability to address the requirements or even problems that can arise on a Project.

Mock Reviews

To enhance the review training listed above (EVMS, IBR, and Surveillance) and best prepare your organization for these events, H&A also provides teams of our consultants who can conduct Mock Reviews for all three of these events. These mock reviews simulate each type of government review, including the conduct of CAM and other manager interviews, the running of metrics testing, and the preparation of in-briefs and exit briefs all of which are integral parts of a government EVMS Review. These Mock reviews can also be used as on-the-job training for company personnel who may be required to conduct IBRs or Surveillance at a subcontractor’s facility. H&A can also augment your company teams in conducting these subcontractor reviews to extend the training while helping your team complete required tasks.

Agile

H&A has a team of experienced Agile Coaches who are also experts in integrating Agile and Earned Value Management methodologies. H&A also has a vast library of Agile and EVM training materials that can be tailored to meet specific client needs.

Specialized and Experienced Training

Our specialized training courses have been developed over time to address the specific training needs of past clients and provide in-depth, focused training in a variety of topics to enhance your application EVM to effectively manage your projects. These courses build on the general knowledge provided by the basic courses to make your team more effective and efficient in each topic area. In cases where your team needs specific, focused training and you don’t find it listed here, we would be happy to discuss the situation and provide a recommended approach to make you successful.

Each H&A Senior Team Lead typically has over 30 years of experience in Industry, in Government, and/or in consulting – so there is virtually no situation or problem that they have not encountered before. So, although your company may be overwhelmed by the EVMS requirements and the expectations of your customer, you can rely on our H&A team of experts to get you through it all successfully.

So please, take a look at the H&A website and all that we have to offer, and then give us a call at (714) 685-1730, or email us so we can get you started on the road to EVMS success. We look forward to helping you be successful!

The world of Earned Value Management (EVM) can sometimes be daunting with a seeming overabundance of resources, guides, training, and services designed to help the user. Depending on which industry and/or government agency you are dealing with, the EVM interpretation can differ. Below is a listing of free online training resources meant to help you in finding the right information for the right situation. Each online source provides a summary of resources available and the URL to find them.

The EVMS Education Center is an online Earned Value Training resource for cutting-edge thought and insight on Earned Value Management Systems. The user can select an EVM category from the list below to access more detailed information:

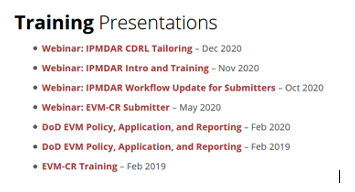

The Policy & Guidance page provides the user with OMB Circular A-11, FAR, and DFARS, 5000 series documents, Data Item Descriptions as well as sample CDRLs and Guides and References. In addition, Training Presentations on IPMDAR Application, Tailoring and Reporting are provided.

The EVM-CR is a data repository managed by the IPM division of OUSD(A&S) AAP, the office of Acquisition, Analytics and Policy.

The purpose of the EVM-CR is to establish a source of authoritative Earned Value Management (EVM) and Integrated Program Management (IPM) data for the Department and to provide prompt access for PMOs, Services, OSD, and DoD Components.

Government users with Analyst role can access all published reports in the EVM-CR

Contractors that support DOD HQ organizations can be granted similar access by providing appropriate NDAs

Training includes an EVM Tutorial which consists of 8 modules and provides a high-level overview of EVM principles and reporting, intended for novice EVM users.

In addition, a series of 34 short video snippets, sponsored by the Office of Project Management (PM), provides training in a variety of EVMS topics.

Includes several downloadable handbooks for reference including:

· Integrated Baseline Review (IBR) Handbook

· Schedule Management Handbook

· Link to request STAT Access and to download the STAT User’s Guide

· Work Breakdown Structure Handbook

· EVM Implementation Handbook

· NASA/SP 2016-3708 EVM P-CAM Reference Guide

NASA IPMR DRD

The Integrated Program Management Report (IPMR) is a consolidation of the Contract Performance Report (CPR) and the Integrated Master Schedule (IMS) and is required on all new contracts when an EVMS is a requirement.

In conjunction with PMI, this website includes several webinar presentations, templates and articles designed to aid the student in a greater understanding of Earned Value Management. The site is continuously updated by contributors across the world and is applicable to both commercial and government environments.

This site provides a comprehensive list of guidance documents applicable across the DoD Environment. Complementary documents to the EIA-748 Standard for Earned Value Management Systems include:

· EIA-748-C Designation Memo

· Earned Value Management System Acceptance Guide

· Earned Value Management System Guideline Scalability Guide

· Earned Value Management Systems Application Guide

· Earned Value Management Systems Intent Guide to the EIA Standard for EVMS (EIA-748)

· Intent Guide Appendix Compliance Map Template

· Guide to Managing Programs Using Predictive Measures

· Industry Practice Guide for Agile on Earned Value Management Programs

· Integrated Baseline Review Guide

· Master Definitions List for IPMD Guides

· Planning and Scheduling Excellence Guide (PASEG)

In Part 2 we talked about the over-application of EOCs at or below the Work Package level and how a CAR assuming that a charge against an Element Of Cost (EOC) equals a charge against a “zero-budgeted WP” was inaccurate.

Use a New EOC

Both of the examples from part 2 were over-applications of the EOC requirement. The point here was that the work (it was to design a circuit card), was planned as labor and was also accomplished (earned) in the month it was planned; so the value would be “earned” as planned. In that period, however, it happened that the planned resource was not available, so the work was actually accomplished using a different EOC such as a subcontractor engineer. The contractor’s system properly showed that the design had been completed and the value earned and that the ACWP for that completion was also in the system (i.e. consistent with the BCWP). However, it just happened to be the Subcontract EOC instead of the Labor EOC originally planned, and the CAM addressed the cost difference in the VAR for the Control Account. The team’s comments on the CARs were that the CAM should have replanned the effort using the new EOC instead of the original one. The problem with this is that in many cases the CAM does not know the original resource is not going to be available until the day it happens. There would (1) be no time to process the change and (2) the change would occur in the “freeze period” (actually in the current month), and (3) this could result in unnecessarily large numbers of Change Requests since these types of events commonly occur in the industry.

Noted instances:

Work planned and earned as internal labor (Labor EOC) had to be performed by contract support (subcontract EOC) in that period because of the non-availability of the planned resource.

[Some Contractors consider each labor grade a separate EOC within labor] Work planned and earned for an Engineer 2. However, the period the work was performed used an Engineer 3 (higher cost).

The plan was to build sub-assemblies in-house (Labor EOC), but a machine breakdown necessitated having a vendor provide substitute off-the-shelf assemblies (Material EOC) that month.

In each of these cases, the “EOC ACWP substitution” was temporary, and the work resumed the next period as planned, using the originally planned Element of Cost. The key here is that in each case, the work was performed, and so it was earned; as it should have been. The only difference was that a different EOC was used to accomplish the work – a simple Cost Variance. While it is certainly true that each WP (and PP) should be planned and WPs earned using a single EOC, the misinterpretation here was that every EOC then is a Work package and they are not. In other words, temporarily using a different Engineer category than planned, or using contract support instead of internal labor, or substituting a purchased material item instead of fabricating internally, etc. simply represents a Cost Variances, and should not be cited as a violation of the EVMS Guidelines.

The “consistency” required by the Guideline and the sub-question is that the EOC actually used was expended in the same period in which the work was completed and the Earned Value claimed (i.e. consistent with the BCWP). The variance analysis would show BCWS, BCWP, and ACWP at the CA level with the EOC details at lower levels.

Now for the big “HOWEVER”!

If the switch in use of the alternate EOC is short term, then the differences should be addressed as a Cost Variance (which could be higher or lower than with the planned EOC); HOWEVER, if the change is expected to be permanent or long term, then the CAM should replan the remainder of the work package using the new EOC, and the EAC should be updated, as well, to reflect the new anticipated total cost using that revised EOC.

Note: Some contractors have what is called a “gray badge” environment, whereby a subcontractor charges their labor directly into the Prime contractor’s labor system. Under this arrangement, for this subcontractor, there would be no difference in EOC if the subcontractor performed the work instead of the prime contractor.

In part one of our series on Elements of Cost (EOC), we explained what EOCs are and gave an analogy of how EOCs would relate to building a patio. We also reviewed how EOCs can be “over thought” and emphasized the importance of properly applying indirect cost rates. This post is going to be focused on the Over-Application of EOCs.

Over-Application of EOCs

During some government reviews, the teams issued Corrective Action Requests (CARs) citing multiple examples of ACWP occurring on “zero-budgeted” Work Packages within Control Accounts. On the surface, this sounds pretty serious, but there were several “over-applications” in play here.

First, the review was being performed at (and in some cases below) the Work Package (WP) level, when the intent of the Guidelines has always been for variance analysis to be performed at the Control Account (CA) Level;

Second, the CAR assumption was that a charge against an Element Of Cost (EOC) equals a charge against a “zero-budgeted WP”.

For the first point we’ll look at Guideline 22 in the EVM Standard 748:

GL 22. At least on a monthly basis, generate the following information at the Control Account and other levels as necessary for management control using actual cost data from, or reconcilable with, the accounting system:

1) Comparison of the amount of planned budget and the amount of budget earned for work accomplished. This comparison provides the schedule variance.

2) Comparison of the amount of the budget earned and the actual direct costs for the same work. This comparison provides the cost variance.

Even the government’s sub-question e. under GL 22 reiterates this requirement:

e. Are the following elements for measuring performance available at the levels selected for control and analysis (at a minimum at the control account level):

While the intent of the words “and other levels” and “at a minimum” was to ensure that contractors did not only perform analysis at some higher, summary level, the government’s choice of those sub-question words also opens up the application of the analysis at lower levels. Be that as it may, the over-application still exists where it should not. Variance Analysis is supposed to be at the CA level and rolled up to higher levels for analysis. The bottom line for each of the CARs written is that BCWS, BCWP, and ACWP existed at the Control Account level, and the EOC visibility was available for variance analysis explanations at the lower levels in the contractors’ systems.

For the second point, let’s look at all the EVM Standard 748 Guidelines, specifically Guideline 16.

There is no Guideline that specifically requires BCWP to be claimed the exact same way BCWS was planned; however, it is intuitive that this has to be true in order for cumulative values for BCWP and BCWS to equal BAC so that the work can be considered complete. [While the government’s sub-question b. under Guideline 22 expects BCWP to be calculated “consistent with the way the work is planned”, GL 22 itself (above) is silent on that inferred expectation.] The Guideline 16 and its sub-question b. also require consistency of the direct costs:

GL 16. Record direct costs in a manner consistent with the budgets in a formal system controlled by the general books of account.

Are elements of direct cost (labor, material, subcontractor, and other direct costs) accumulated within control accounts in a manner consistent with budgets using recognized acceptable costing techniques and controlled by the general books of account?

In the examples noted for the CAR referenced above, the work package task was a specific Element Of Cost (EOC) and was planned and completed in the same period, but no ACWP was accumulated for that specific EOC because the work was accomplished using another resource that fell into another EOC category. When the team looked at that EOC containing the ACWP, they interpreted the finding as a “zero-budgeted Work Package” with ACWP against it. [They also cited the original Work Package itself for having BCWP with no ACWP for the element of cost that was planned and earned.]

Labor, Materials, Subcontracts, Other Direct Costs, and their Indirect Costs (Overhead including General and Administrative —G&A) are the typical building blocks for any project: personal projects and projects we manage for the customers we support. These items are also what the Earned Value Management System (EVMS) Guidelines call elements of cost (or EOCs). So, when the Guidelines call for us to plan and manage by EOC, it really should not cause us any undue anxiety – it is just the natural way to manage any project.

Example: Outdoor Backyard Patio

Let’s use a simple home project example of building an outdoor backyard patio: What do you have to do to determine how much it will cost for this Backyard Patio Project (BPP if you like acronyms)? Generally, you look at such things as:

How much concrete; lumber for decking; nails, screws, bolts, washers, and other hardware, etc.; and weather-coating and paints/stains you will need (Material Element of Cost – EOC).

Work you cannot do by yourself: electricity for lights and power, and natural gas for the Barbecue/fireplace (Subcontract EOC).

Work you will do yourself (Labor EOC).

Costs unique to this project’s completion, such as: Home Owners Association permits, building code permits, local excavation application fee, etc. (Other Direct Cost EOC).

Costs incurred that do not necessarily go into the final product, such as: cleaning supplies, brooms, solvents, turpentine, weather tarpaulins, lighting and electricity, etc. (Indirect Costs/Overheads).

Unfortunately, when operating under the EVM requirement, often managers tend to overthink, and sometimes over apply the management of EOCs. Let’s look at the overthinking part first.

Overthinking EOCs

Guideline 9 of the EIA Standard 748 (Revision D) for EVM Systems requires:

Establish budgets for authorized work with identification of significant cost elements (labor, material, etc.) as needed for internal management and for control of subcontractors.

Some might propose: “I’ll have one Work Package for the Control Account with all the EOCs in it, and I’ll be okay.” That might meet the intent of that first part of the guideline, but would probably fail the requirement that says “as needed for internal management and control of subcontractors.” For example, what EV technique would you use for a “work package” that had labor, material, and subcontract work in it? The labor occurs as the work is performed, the material might be earned at the point of receipt on the dock, and the subcontract might earn value with the receipt of an Integrated Program Management Data and Analysis Report (IPMDAR) dataset at the end of a month. Since the Control Account (CA) has one total dollar budget, the “identification of significant cost elements” has to occur at the Work Package (WP) and Planning Package (PP) level within the CA, which requires each WP and PP to be identified as one of the EOCs mentioned above.

For Instance

In our example, if we lumped concrete and lumber into one “Material WP” and we incurred a serious overrun in material, how would we identify what caused the overrun: the concrete pour or the lumber portion? These are different categories of material that would “earn value” (be accomplished) in different ways and at different times. In order to determine the “guilty party” in the overrun, we should also have separate WPs for the different significant material categories. Some might call these major, or high value, or critical material items, which should be tracked separately.

On the other hand, for the lower-value materials, it may not be significant enough to management to know that a variance might have been caused by a 1-cent washer or a pint of deck stain. Consequently, a grouping of these low-value material items may be all that is required for visibility. Conversely, Management might actually want to break out categories such as, separating the paints/stains, and weather-coating from the nuts, bolts, washers and other hardware, since they are different categories of low-value material that could also earn value differently.

Indirect Cost Rates Must be Applied Properly

For Indirect Costs, some contractors put the burden of planning and managing these overhead costs on the CAMs, while others apply the indirect rates at a summary level of the Work Breakdown Structure (WBS) or organizational structure. Regardless of how a particular contractor does it, the indirect cost rates must be applied properly to the various direct elements of cost:

Material handling charges applied to material items

Indirect Labor rates applied to the direct labor hours

Subcontract overhead applied to the subcontract direct costs

ODC overheads charged to the ODCs identified.

Applying and managing overheads at the CA level would entail hundreds of applications across the number of Control Accounts on a project, but applying these at a summary level would require only a handful of Overhead lines in reports. Doing so would significantly reduce the number of possible errors in application – which is why many contractors do not require CAMs to “manage” overheads in their Control Accounts. [Our BPP example does not have the above types of Indirect Costs that are related to specific Direct Costs, but it does have its own specific Overheads related to the labor to build the Patio.]