We are starting a new series that will share some of the adapted video content from our EVMS Workshops. This first video is a brief overview of Earned Value Management, what it is, where it came from, and why it was developed.

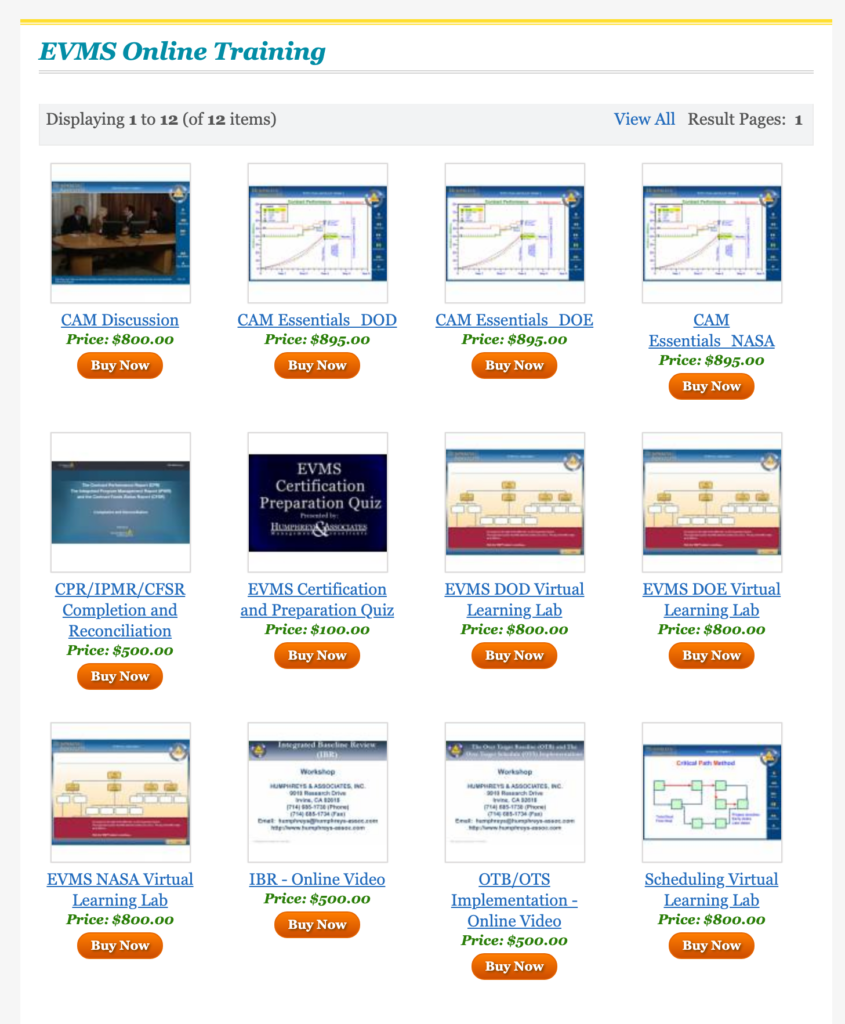

More EVMS Training

If you liked this video you can purchase the entire course below. This video is an excerpt from the Department of Defense (DOD) version of this eLearning module. We also offer the same course customized for the Department of Energy’s (DOE) specific Earned Value Management (EVM) implementation/requirements, as well as a version of the course customized for NASA’s EVM implementation/requirements.

Not sure what the different requirements are between the DOE and NASA? Can’t remember if Cost and Software Data Reporting (CSDR) is required for an NSA contract? Check out our easy to read Earned Value Management Systems Document Matrix

At first glance, it may seem that EVM and Agile development methodologies are incompatible. Agile is all about rapid incremental product deliveries and responding quickly to an evolving understanding of the desired deliverable or outcome. Depending on how an EVMS is implemented, the EVMS can often seem rigid in comparison.

Can the two methodologies coexist and complement each other to create an effective integrated project management system? The answer is yes, provided you have thought through how you intend to use the two systems together and map how and where they integrate. The goal is to leverage the benefits of each system and without forcing either system to do something it wasn’t meant to do.

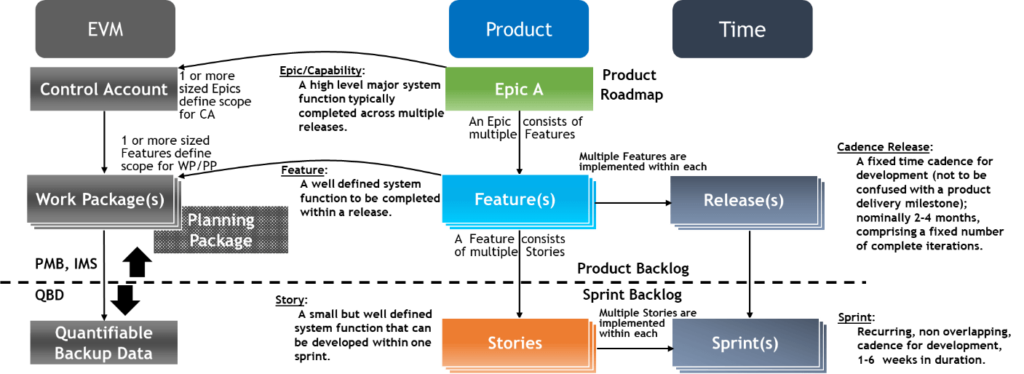

There is a natural top down and bottom-up process integration when defining the scope of work and acceptance criteria. This process integration continues for planning and scheduling the feature estimates of effort, establishing the budget baseline, and ultimately maintaining the estimate to complete (ETC) in the EVMS. It also supports an integrated process for measuring completed work. The Agile daily standup meetings provide current information about accomplishments and impediments at the lowest level of the project. The Agile system provides the quantifiable backup data for claiming earned value in the EVMS for performance reporting.

The following image illustrates the relationship between the two systems.

The source for this image is the NDIA IPMD Industry Practice Guide for Agile on EVM Programs, Revision May 2019, Figure 2-4.

The Foundation for Integrating EVM and Agile: Defining the Scope of Work

A work breakdown structure (WBS) is commonly used to organize and decompose a project’s scope of work into manageable, product-oriented elements. It is an essential communication tool for the customer and contractor so they have a common frame of reference to capture and manage requirements as well as expected deliverables or outcomes. It establishes a common basis for measuring progress and defining accomplishment criteria. It is the framework for developing a project’s schedule (timing of tasks), identifying resources to accomplish the scheduled tasks, creating cost estimates as well as the budget baseline, and identifying risks. In an EVMS, the WBS is often decomposed to the control account level which is further decomposed into work packages or planning packages. Once extended to the lower level, it provides a framework for tracking technical accomplishments, measuring completed work, and identifying variances from the original plan to complete the work.

There is a similar planning hierarchy to Agile projects – the Product Backlog is the foundation for defining the scope of work. The Product Backlog starts at the Epic or Capability level and is further defined through product planning. The process includes prioritizing the capabilities and defining the sequence of deliverables to create the Product Roadmap (timing). The capabilities are decomposed into features along with an estimate of the effort to deliver the feature. Features should include exit criteria (definition of done) and have minimal dependencies. At the lowest level, features are decomposed into Sprint Stories and related tasks forming the basis for the schedule and measuring completed work in the EVMS. As illustrated in the image above, in the Product Backlog hierarchy, an Epic/Capability relates to the control account level in the EVMS. Features relate to the work packages in the EVMS.

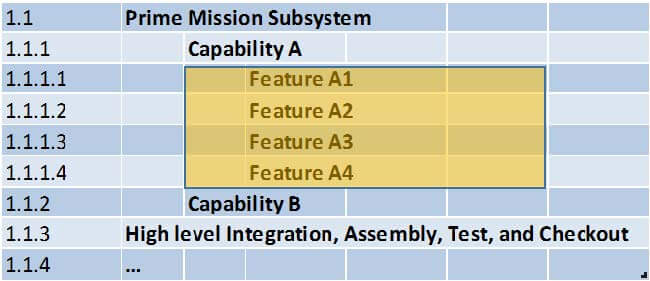

In an integrated environment, there can be a natural mapping between the WBS and the Product Backlog regardless of the starting point. When starting from the Agile system, the Product Backlog could be used to create the project’s WBS. The customer may also pre-define the top level WBS elements that could form the backlog structure. The DoD uses MIL-STD-881, Work Breakdown Structures for Defense Materiel Items, for this purpose so they have a set of common templates they can use across programs to capture historical actual cost data for cost estimating and should cost analysis. Even though the top level WBS elements may be pre-defined, the lower-level content can reflect an outcome based Agile structure that focuses on customer driven deliverables. An example is illustrated here.

Possible Agile software development MIL-STD-881 WBS breakout. The source for this image is the DoD ADA Agile and Earned Value Management: A Program Manager’s Desk Guide, Revision November 2020, Figure 2.

What’s common between the two systems? You have:

Decomposed a common understanding of the scope of work into manageable, product or outcome-oriented elements of work.

Defined the agreed upon accomplishment criteria or definition of done for a given deliverable or outcome.

Built a framework to determine the timing of tasks, identifying the resource requirements, creating a cost estimate to do the work, and means to objectively measure completed work. Ideally, you have also identified the risks or uncertainties so you know where potential issues may surface.

Best Practices for Integrating the WBS and Product Backlog

Keeping in mind you have a similar decomposition of work between the two systems, you can set up the WBS and Product Backlog to align with each other. The goal is to ensure traceability so you can easily support the EVMS requirements.

Here are a few best practices for integrating the WBS and Product Backlog.

Verify the WBS aligns with the prioritized Product Backlog to at least the Epic/Capability level (control account level in the WBS). Determine how you intend to maintain traceability between the WBS elements and the work items in the Product Backlog so it doesn’t matter which system you use to review or confirm the agreed upon scope of work. Identify and document how you intend to map the WBS elements to a work item in the Product Backlog so you always have the necessary cross references identified. Keep it simple. Where possible, minimize the need to enter something more than once.

Use the Product Backlog to tailor the WBS. This is particularly true for projects where Agile development is central to the final deliverable. Consider your two end objectives: you need to provide project performance reporting via the EVMS and organize the items in the Product Backlog so you can decompose them from the Epic/Capability level to the Feature level and then to the Sprint Story and task level.

Watch the level of detail in the WBS. Avoid driving the WBS to too low a level of detail. Depending on the project, it may be appropriate to go no lower than the Epic/Capability level (control account level). The reasoning: in the Agile system, the lower-level Stories and tasks are flexible and subject to change. You are focused on completing current near-term work effort within a Sprint. Better to let the Agile system manage and track what is happening at the rapidly changing detail level – it is designed to do that. For EVMS purposes, project monitoring and control should be at a higher level where scope can be consistently defined, aligned to the schedule and budget, and claimed as done (technical accomplishment). The WBS should reflect the level of detail that is aligned to the permissible variation in requirements or configuration. Otherwise, you create too much change “noise” in the EVMS.

Confirm the WBS and Product Backlog contains 100% of the contract scope of work. Verify the statement of work has been mapped to the WBS elements or work items in the Product Backlog. Why is this important? You need to demonstrate you have captured the entire technical scope of work to at least the Epic/Capability level. You need this for internal planning purposes so your development teams have an understanding of the technical requirements and expected outcomes as well as managing changes. Your customer also needs confidence that you have an understanding of the entire scope of work and have planned accordingly for the duration of the project.

Verify you have defined the Feature accomplishment criteria or definition of done so it is easy to measure completed work. This could be in the WBS dictionary or documented in the Agile system Product Backlog. Determine where that information can be found and document the process to maintain it. Ideally it is in one place so you only have to maintain it in one system and everyone on the project knows they are referencing current information. Clearly defined accomplishment criteria mean you can objectively measure accomplishments – in both systems. Enable that capability right from the start when you set up a new project in the two systems.

Are your EVM and Agile systems are sharing useful information? Perhaps you have learned the hard way the WBS and Product Backlog aren’t sufficiently mapped for you to maintain traceability between the two systems. We can help. Call us today at (714) 685-1730

Do any (or many) of these situations apply to you?

The Project has to comply with the EIA-748 EVMS Standard! What is that? How do we do that?

You have a new contract of over $20 Million, and you need to get yourself, your staff, and all the Project personnel up to speed on your new contractual Earned Value requirement.

The RFP says the company must have an Earned Value Management (EVM) certification. How can we respond to the RFP?

Your contract is over $100 Million and now you must have and demonstrate a Certified Earned Value Management System (EVMS). How do you do that?

How do you get a compliant EVMS Description in the first place?

You reviewed company training materials and everything dealing with Earned Value is out of date; and it is going to cost thousands to update the materials and keep them up to date!

What are Control Account Managers (CAMs)? Must we have CAMs to do Earned Value? How do I get CAMs/Train them?

I used to have great CAMs, but none of my new CAMs can spell EV. How do I train them?

You Are Not Alone

If you answered “yes” to any of these, don’t feel like the Lone Ranger. Even though the Earned Value concept has been around for over 50 years, the requirement can still be new to your company, new to your contract, and new to your employees. Most will not have learned EVM in college. Even companies that have been using EVM for years face a recurring need for training. We’re pretty consistently seeing a turnover of 20-40% of our experienced CAMs each year across the industry.

If you answered “yes” to several, I’m sure you’re a bit overwhelmed and asking yourself, how can we possibly meet all these requirements?

H&A has trained over 950,000 people around the world in all aspects of the Earned Value requirements and has built the largest, most comprehensive library of training materials in the Earned Value Management consulting industry. We have tailored training materials and have trained and supported contractors whose customers have been from DOD, DOE, NASA, FAA, HHS, as well as international customers such as the Australian DOD, the Canadian DND, Sweden Defense, and the UK.

Basic and Advanced Courses in Earned Value Management and

Control Account Manager/Project Controls Staff Training and Certification;

EVMS Review training to prepare upper management and project teams for:

Earned Value Management System Review,

Integrated Baseline Review (IBR), and

Internal/Joint/External Surveillance;

Specialized training in:

Developing a WBS,

Planning Techniques,

Project Scheduling,

Baseline Establishment,

Materials Management,

Subcontract Management,

Basic and Advance Variance Analysis,

Estimating,

Change Management,

Government Reporting requirements,

OTB/ OTS incorporation, and

Agile Software Development

Real-World Application

Our curriculum makes extensive use of real-world examples and case studies to extend the process of learning into application. We offer these hands-on courses in a variety of settings and formats to meet your needs.

Public offerings are open to the industry at large and are particularly useful when you have a limited number of individuals needing the training or those individuals who are widely geographically separated.

In-house offerings at your facilities allows us to meet the training need at one location or for one specific team and can include specifics of your system description.

Earned Value Webinars

Webinar offerings of the two courses above and our Virtual Learning Lab (VLL) format are available, especially in these times of limited travel. Webinars of the public and in-house training courses rely on the same content as the in-person courses with the addition of virtual interaction opportunities to increase student involvement and enhance learning. Our Virtual Learning Lab (VLL) format provides an opportunity for busy individuals to learn at their own pace and time of their choice – even if they are working from home. The VLL makes extensive use of video presentations and application case studies to enhance the learning environment and ensure the students continue to apply the knowledge they have gained.

Training Materials

If you have an existing training staff, H&A can even be your source for training materials. Most of our courses are available for purchase/licensing and our staff of EVMS experts can tailor them to any company environment. The big benefit here is you leveraging H&A active involvement with EVM requirement changes to keep the material up to date and your training staff don’t have to do it. In the end you get an up-to-date course without out committing the staff and costs to do the work. This approach also aligns your material across all our offerings to provide you delivery flexibility with a consistent core content.

In addition to providing course materials, H&A also can provide Train-The-Trainer sessions in those courses, so your company’s training department can understand and become comfortable with the training materials and updates.

EVMS Certification Programs

Our Certification programs go beyond the public or in-house training courses to create the Qualified CAMs and Project Controls (PC) personnel that are integral parts of a successful EVMS implementation. These roles are where “the rubber meets the road” for EVMS. CAMs and PCs will be expected to demonstrate how the company’s EVM System is actually operating on a day-to-day basis. H&A offers comprehensive and rigorous Certification Courses for both of these important functions so you can be assured that your people not only understand Earned Value concepts but have demonstrated the ability to address the requirements or even problems that can arise on a Project.

Mock Reviews

To enhance the review training listed above (EVMS, IBR, and Surveillance) and best prepare your organization for these events, H&A also provides teams of our consultants who can conduct Mock Reviews for all three of these events. These mock reviews simulate each type of government review, including the conduct of CAM and other manager interviews, the running of metrics testing, and the preparation of in-briefs and exit briefs all of which are integral parts of a government EVMS Review. These Mock reviews can also be used as on-the-job training for company personnel who may be required to conduct IBRs or Surveillance at a subcontractor’s facility. H&A can also augment your company teams in conducting these subcontractor reviews to extend the training while helping your team complete required tasks.

Agile

H&A has a team of experienced Agile Coaches who are also experts in integrating Agile and Earned Value Management methodologies. H&A also has a vast library of Agile and EVM training materials that can be tailored to meet specific client needs.

Specialized and Experienced Training

Our specialized training courses have been developed over time to address the specific training needs of past clients and provide in-depth, focused training in a variety of topics to enhance your application EVM to effectively manage your projects. These courses build on the general knowledge provided by the basic courses to make your team more effective and efficient in each topic area. In cases where your team needs specific, focused training and you don’t find it listed here, we would be happy to discuss the situation and provide a recommended approach to make you successful.

Each H&A Senior Team Lead typically has over 30 years of experience in Industry, in Government, and/or in consulting – so there is virtually no situation or problem that they have not encountered before. So, although your company may be overwhelmed by the EVMS requirements and the expectations of your customer, you can rely on our H&A team of experts to get you through it all successfully.

So please, take a look at the H&A website and all that we have to offer, and then give us a call at (714) 685-1730, or email us so we can get you started on the road to EVMS success. We look forward to helping you be successful!

Likely you have been on the receiving end of this advice. The common solution to every problem seems to be: do more training. Well, yes, that is often a logical conclusion. The hard part is, how do you implement earned value training that actually helps project personnel improve their knowledge levels and skill sets that makes a difference in how projects are managed? Conducting training just to check something off a to-do list is a waste of everyone’s time.

Here are a few tips to help you implement an effective EVM training plan.

Tip 1 – What’s the problem you want to resolve?

A clear understanding of the problem you want to solve helps determine the scope of the training, who needs the training, and what kind of training will make a difference. Here are a few examples to illustrate a range of the scope of the training from the complex to targeted training.

The good news? You just won a government contract with EVMS contract clauses. The bad news? Your company’s project control system is immature at best and will need to become more disciplined to support the contractual EVMS requirements. You are going to need a robust education and training plan to rapidly increase the project control maturity level of your company. Likely you will need to enhance your current project control practices, add process and procedures, perhaps implement new software tools, and educate a variety of functional managers and project personnel on the upgraded best practices they will need to follow.

You have an influx of new project personnel that need to learn the ropes. Where are they with their current skill sets and what will help them improve? Perhaps they have a basic understanding of project control or scheduling, but don’t know how to apply your company’s preferred practices or how to effectively use the software tools. They may need a broader earned value training plan that covers a number of disciplines or hands-on workshops that combine process training and using the software tools to effectively perform their project control tasks.

You have a contractual or audit event coming up. Examples include an Integrated Baseline Review (IBR) for a new project or the DCMA is coming in to do a compliance review. That means you need to make sure all levels of project personnel are prepared for the review and that quality schedule and cost data have been established. Different types of focused training or mentoring is often required to prepare for these events where there is interaction with the customer project manager or audit agency personnel. Personnel knowledge, the EVMS, how they apply the EVMS on their project, and data traceability will all be assessed.

As part of your internal process improvement activities, you discover a number of control account managers (CAMs) are having difficulty producing useful variance analysis report (VAR) narratives. Or, perhaps the schedulers are having trouble creating or maintaining their integrated master schedules (IMS) to the level of data quality you expect. Targeted or role specific training could make a difference here.

Tip 2 – Determine what you need to accomplish your training objective

Here is a sort list of factors to consider as you begin to sort out what type of training or training materials you need to have in place to accomplish your training objectives.

Do you intend to create and maintain a set of EVM related training materials internally? What types of materials you intend to maintain? This could be a range of materials such as instructor led presentation and course materials, role specific training materials or templates, desktop instructions, online help, or self-paced instructional videos. Do you have the personnel, time, and budget to do this? Do you have the internal EVM expertise? You may need help creating your internal materials or you may need to rely on outside services to supplement your internal training.

How do you intend to deliver the earned value training, how often, and how many people? A day or two dedicated to classroom instruction may or may not be option. Perhaps project personnel need to complete the training remotely or are only available for a short duration. How do you accomplish your training objectives and verify personnel are applying what they are learning?

You need to prepare a contractual event such as an IBR. This presents a different set of factors and you may or may not have a process or EVM expertise in place to handle this. Depending on your company, you may have the internal project management resources you can pull from another division to help the project personnel prepare for the event and perform an independent review of the schedule and cost data. How do you intend to handle these events?

Targeted training to address a recurring issue or a unique project situation such an implementing an over target baseline/over target schedule (OTB/OTS). For example, targeted training would be useful for CAMs or schedulers that need help getting to the next level of proficiency. One option could be to solicit the help of an internal “power user” to help mentor project personnel in how to do things or how to effectively use the software tools. Or, you could leverage the expertise of outside services to help mentor them and expand the base of proficient project personnel over time.

Tip 3 – Who you select to help you with your earned value training objectives matters

There are a number of companies that offer earned value and related training. There are a number of factors to consider as you start to evaluate their services, expertise, scope and availability of training materials, and range of training options.

There is a reason why H&A has been the leading provider of earned value training and earned value consulting services for over four decades. We have proven, cost effective approaches to increasing your project control team’s skills so they become more valuable assets to your organization. For example:

We have built the largest, most comprehensive library of training materials in the EVM consulting industry including basic and advanced courses as well as specific topic areas such as developing a WBS, OTB/OTS, preparing a VAR or government performance report, subcontract management, change management, or IBRs.

What’s the benefit to you? Should you need source material for a training course, our courses are available for lease and can be tailored to your environment. You don’t have to start from scratch. We actively maintain our course materials and provide updates as requirements change over time including specific versions for DoD, DOE, and NASA. This takes the burden off you and reduces the cost of keeping up with changes. We provide train-the-trainer sessions for the courses, so your company’s training department can become proficient with the materials to build out your internal training library over time.

We offer our hands-on courses as public workshops, in-house, or remotely. We also offer our most popular three-day workshops as distance learning courses. We refer to these as our EVMS Virtual Learning Lab and Scheduling Virtual Learning Lab (VLL) so your project personnel can learn at their own pace – even if they are working from home. The benefit is you can select a combination of training options to fit your needs as well as personnel availability or location.

We offer two career path certifications you could leverage to assist project personnel looking to advance their knowledge and skills. We created the H&A Control Account Manager (CAM) Certification program over 5 years ago and approximately 600 people have gone through this rigorous certification process. We also created a Project Control/Analyst (PC/A) Certification for personnel that support CAMs and Project Managers. These certifications mean the individual has demonstrated a knowledge level that establishes a sound foundation for success as a CAM or PC/A.

H&A senior personnel typically have over 30 years of experience in industry, government, and consulting across a variety of industries. When you need help with an IBR or government compliance review, our consultants can help prepare and mentor your project personnel to successfully navigate the review process as well as perform data traces with them to verify the quality of the schedule and cost data. When you need help training personnel on a specific EVM topic such as OTB/OTS or how to prepare a VAR that requires additional EVM expertise, we can conduct the training for you whether in-house or remotely.

You can rely on the H&A team of experts to help you with your EVM, scheduling, and related training needs. For more information about our courses, descriptions, and delivery options, visit our web page at: https://www.humphreys-assoc.com/evms/evms_training_courses.php.

The New Integrated Program Management Data and Analysis Report (IPMDAR) Data Item Description (DID) and Implementation Guide

On March 12, 2020, the Defense Department (OUSD/AAP) instituted the new Integrated Program Management Data and Analysis Report (IPMDAR), issuing the Data Item Description (DID) Number: DI-MGMT-81861B. The IPMDAR is to be used for solicitations and RFPs for contracts with an EV reporting Requirement starting from March 12, 2020 forward. The IPMDAR can also be applied to modified contracts or to existing contracts (under the old IPMR or CPR requirements), but this has to be through a bi-lateral agreement (Government Program Office and Contractor).

Significant Change

This IPMDAR is a significant change from the previous iterations, the Integrated Program Management Report (IPMR) and the old Contract Performance Report (CPR). The IPMDAR has dispensed with the delivery of physical reports (Formats 1 – 7 of the old IPMR/ CPR), instead now requiring contractors to provide three (3) specific electronic data sets:

The Contract Performance Dataset (CPD)

The Schedule, comprised of

The Native Schedule File and

The Schedule Performance Dataset (SPD)

The Performance Narrative Report, comprised of

The Executive Summary and

The Detailed Analysis Report

The DID states: “The IPMDAR’s primary purpose to the Government is to reflect current contract performance status and the forecast of future contract performance.”

Implementation & Tailoring Guide

To help expedite the adoption of the New IPMDAR, on May 21, 2020, the AAP office also issued the 87-page Integrated Program Management Data Analysis Report (IPMDAR) Implementation & Tailoring Guide: “This guide covers the application of the DID, how to tailor the DID in the Contract Data Requirements List (CDRL), and clarification on the intent of the DID.”

Interesting Features

The IPMDAR has introduced some interesting features that are clarified in the Guide:

The default reporting is at the Control Account, but there is the option to have Work Package Level reporting (negotiated item)

Reporting is by Hours and Elements of Cost (EOCs) (for either the CA or WP level)

Time-phased Future Baseline (BCWS) and ETC Forecast (for either CA or WP level)

Best Case/Worst Case/Most Likely EACs reported by hours and dollars

The Native Schedule is a direct export from the contractor’s scheduling tool

The SPD must match the CA or WP level negotiated

The Government may have any subcontractors provide the IPMDAR directly to the Government

Even if this is required, the subcontractors must still provide the IPMDAR data to their prime contractor

The IPMDAR reporting components must be delivered to EVM-CR not later than 16 business days after a contractor’s accounting period

Incremental deliveries may be authorized, but all the items must be in NLT the 16th business day and the incremental deliveries are negotiated. A potential example is IMS by third working day after close-of-month, the raw data by fifth working day, and format 5 narrative by the sixteenth working day.

Historical Contract Performance Data – The Government may request this “time-phased historical data from contract award” in place of the normally provided CPD (typically no more than annually).

Applicability

IPMDAR Applicability:

IPMDAR is intended to be applied completely (i.e., not tailored) for cost or incentive contracts ≥ $20M – unless tailoring is specified within the DID and coordinated with the Service/ Agency EVM Focal Point.

If EVM reporting is required on contracts less than $20M, tailoring is more flexible, BUT the Native Schedule and Performance Narrative Report are recommended.

IPMDAR typically not required on FFP.

Humphreys & Associates, Inc. can help you properly implement the new IPMDAR requirements, please contact us at (714) 685-1730

Do you know basic Earned Value Management terms and how they relate to an EVMS graph? Before watching this video take the quiz and see if you can identify all of the parts of the EVM graph example.

If you are not sure about a specific term, use the links below to skip to that term’s definition.