Issues with a contractor’s estimate at completion (EAC) process is a common Earned Value Management System (EVMS) surveillance finding H&A earned value consultants are frequently asked to help resolve. The EAC process can become a major issue when the government customer lacks confidence in the contractor’s EAC data.

Why does a credible EAC matter?

EACs are important because they provide a projection of the cost at contract or project completion, which is also an estimate of total funds required by the customer. It matters because EACs represent real money. When the most likely EAC exceeds the negotiated contract cost, the contractor’s profit margins may be at risk. It also creates a problem for the customer when the most likely EAC exceeds the funding limits. The customer may either need to secure additional funding or modify the work scope. No one likes cost overrun surprises.

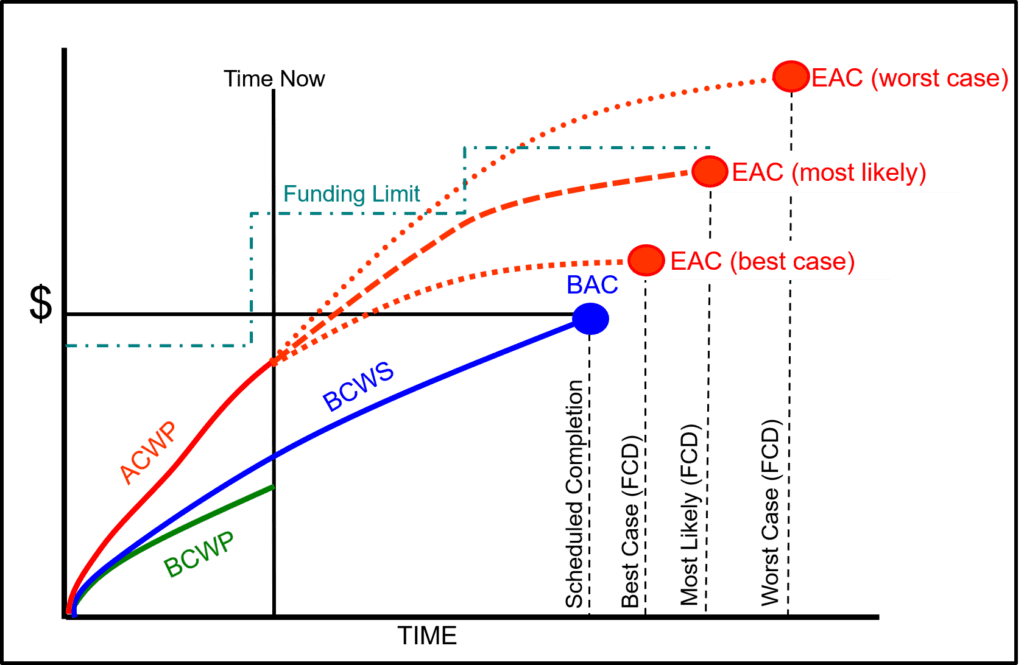

Figure 1 illustrates comparing the funding limits with the range of contractor’s EACs to verify they are within the bounds of the funding available to complete the scope of work.

What determines whether an EAC is credible?

A credible EAC reflects the cumulative to date actual costs of work performed (ACWP) (costs the contractor has already incurred) plus the current estimate to complete (ETC). The ETC must provide a realistic estimate of what is required to complete the remaining authorized work and represents the time phased estimate of future funds required.

EACs should be based on performance to date, actual costs to date, projections of future performance, risks and opportunities, economic escalation, expected direct and indirect rates, and material commitments. As illustrated in Figure 1, a project manager should routinely evaluate their project’s ACWP, ETC, and EAC along with the funding profile to verify amounts expended and committed are within the parameters of available contract funds.

What project control practices help to ensure EACs are realistic?

Three recommended best practices H&A earned value consultants either help implement or have observed that ensure the EAC data are credible include:

- Actively maintain the bottom up ETC data every reporting cycle. This starts with updating the current schedule resource loaded activities based on performance to date and the latest planning (timing and resource requirements) for work in progress as well as upcoming work effort. This becomes the basis for updating the time phased cost estimate for work in progress that is added to the cumulative to date actual costs or the cost estimate for future work/planning packages. The current schedule and time phased cost estimate should be in alignment. When data is routinely maintained, it minimizes the time required to update it and capture useful information. The control account managers (CAMs) have the basis to substantiate their estimates as well as relevant data they can use to analyze and take action to address a significant variance at completion (VAC).

- Actively monitor project EACs from the top down. Project managers that actively maintain a range of data driven EACs (best case, most likely, and worst case) are better prepared to verify the bottom up EACs are realistic, handle realized risks, and prepare for emerging risks. They routinely incorporate metrics such as comparing the Cost Performance Index (CPI) to the To Complete Performance Index (TCPI) to test the realism of the EAC. They can demonstrate their EACs are credible with backup data, rationale, and narratives they provide to management as well as the customer.

- Maintain open communications at all levels of management, subcontractors, and the customer. As a result, project personnel can quickly handle issues or project changes. The project manager is often the main conduit to handle impacts to their project’s EAC such as when corporate management changes direct or indirect rates, changes in resource availability, a spike in commodity prices, or the customer modifies the scope of work or funding.

What are some things to avoid?

H&A earned value consultants often observe practices that negate the purpose and value of maintaining the ETC and EAC data. Issues with the EAC process are often captured in the government customer’s EVMS corrective action requests (CARs). The CARs frequently point out ad-hoc processes or corporate culture issues. Examples:

- Management provides a target EAC number the CAMs must match. This approach increases the likelihood the ETC data are unrealistic. There may be a valid reason for this directive as a management what-if exercise. When done as a routine management strategy, it diminishes the value of the ETC data to manage the project’s remaining work and prevent financial surprises. The CAMs should be in a position where they can substantiate their schedule timeline, resource requirements, and cost estimate to complete the remaining work. The project manager should be in a position where they can verify the bottom up ETC/EAC data to establish a level of confidence in their project level EACs they provide to management as well as the customer.

- Project personnel take the path of least resistance. This is often a result of a lack of direction or an established process. They either do not create the ETC data or maintain it on a routine basis. A typical approach is to set a cost management tool option where the EAC is static; the CAM may manually update the EAC number once a quarter. The ETC data has limited to no value. This usually surfaces as a major issue when the contractor must provide an Integrated Program Management Report (IPMR) Format 7 (time phased history and forecast data), or the Integrated Program Management Data and Analysis Report (IPMDAR) Contract Performance Dataset (CPD) to the customer. The customer quickly discovers the ETC data is lacking for their own analysis.

- Schedule and cost are created/maintained separately. This often occurs when the schedule and cost tools are not integrated for the duration of the project. A good deal of effort may go into ensuring the schedule and cost data are in alignment to establish the performance measurement baseline (PMB). The integrated master schedule (IMS) resource loaded activities may be used as the basis for the time phased budget baseline in the cost tool. However, the ETC data in the current schedule may not exist or actively maintained. Project personnel only maintain the ETC data in the cost tool and fail to verify it aligns with the current schedule activities (timing) and resource requirements. Once again, personnel are often lacking an established best practice EAC process.

Pay Attention to Your EAC Process

The ETC and EAC data are just as important as the PMB budget plan because it represents real money. As discussed in the blog How Integrated Baseline Reviews (IBRs) Contribute to Project Success, the goal of the IBR is to verify an executable PMB has been established for the entire contractual scope of work. Similarly, the goal of maintaining a credible ETC and EAC is to verify an executable plan is being regularly updated to accomplish the remaining scope of work within the contract’s schedule, cost, and funding targets. The customer must have confidence in the contractor’s ability to deliver and meet the remaining contract objectives.

The best way to avoid an EAC process CAR is to ensure you have an established process personnel follow, and they know how to use the schedule and cost tools to consistently maintain quality ETC and EAC data. H&A earned value consultants have worked with numerous clients to design or enhance their EAC process. H&A also offers EVMS training workshops that include content on how to develop a realistic EAC. Regular EVMS training always helps to reinforce best practices. Call us today at (714) 685-1730 to get started.

Ref: Maintaining a Credible EAC – March 7, 2023

A good article.

Will there be a future article on EAC Realism Analysis?

You have one sentence that discusses CPI vs TCPI but no mention of IEACs.

The automated evaluation of IEACs and CPI vs TCPI can provide a consistent implementation of Control Account EAC Realism Analysis.

With the exception of CPI vs TCPI > 0.1, I do not see any Industry Standards on the choice of IEACs, thresholds, nor handling of division by zero and multiplication of zero.

If H&A were to publish a white paper it could quickly become a standard for everyone to measure against.

It has come to our attention that one of the industry earned value analysis tools does not perform IEAC calculations in a consistent manner.

An industry accepted white paper would help to address this issue.

We recently posted another blog titled “Using Earned Value Management (EVM) Performance Metrics for Evaluating EACs” as a follow up to this blog. We have also taken the action to conduct a study on the IEAC metrics contractor’s are using to evaluate the likely final cost of a contract. We announced the launch of this study, Enhancing the Use of IEACs to Test EAC Quality, at the NDIA IPMD meeting on May 17, 2023. We are working through the details to collect data from a variety of contractors for this analysis. Look for follow up blogs and articles on our progress.

Pingback: Using Earned Value Management (EVM) Performance Metrics for Evaluating EACs - Humphreys & Associates