Comprehensive Guide to EVMS Training

Section 1: Understanding the Basics of EVMS

Earned Value Management Systems are a critical component in the project management landscape. At its core, an Earned Value Management System (EVMS) offers a systematic approach to integrating scope, schedule, and cost. Implementing an EVMS enables project managers to measure project performance and progress in an objective manner that increases management visibility and control.

Key Principles and Terminology

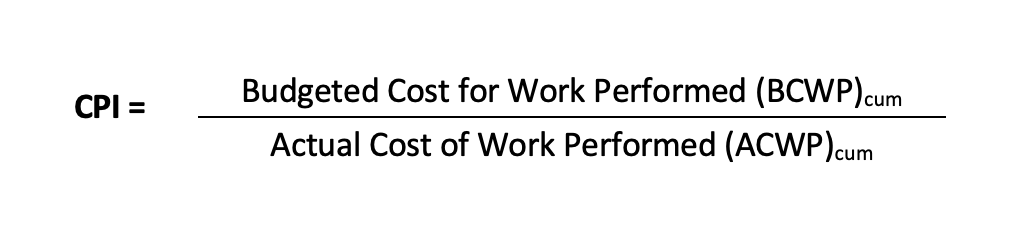

To grasp the fundamentals of Earned Value Management, one must become familiar with its primary principles and associated terminology. Some of these key terms include Planned Value (PV), Earned Value (EV), and Actual Cost (AC), which form the basis for evaluating project performance and predicting future outcomes. Understanding these concepts is essential for anyone seeking to implement an EVMS.

The Role of EVM in Project Management

Effective project management hinges on the ability to forecast potential issues and measure ongoing performance against the project plan. An EVMS provides a structured framework for this purpose, allowing managers to identify variances in cost and schedule before they become critical. By integrating scope, schedule, and cost, an EVMS serves as a compass for project managers, guiding them through the complexities of project execution.

The Benefits of Implementing an EVMS

Implementing an EVMS reaps several benefits, including enhanced visibility into the health of a project and the ability to make data-driven decisions. An EVMS enables stakeholders to objectively assess project performance against the baseline, ensure alignment with strategic objectives, and encourage accountability among team members. Moreover, with an EVMS in place, organizations are better equipped to meet contractual requirements, especially for government contracts which oftentimes mandate the use of such systems.

By grasping the basic principles of EVM and the role it plays in project management, professionals can start their journey toward effective project control and successfully implementing an EVMS. With a comprehensive understanding of the basics, they can build a solid foundation for further exploration of the practices and principles that will lead to mastery of Earned Value Management.

Section 2: Steps to Obtain a Professional EVM Certification

Eligibility Criteria for a Professional EVM Certification

Before embarking on the journey to obtain a Professional EVM Certification, it is important to clarify the prerequisites. Typically, these may include a certain level of experience in project management, understanding basic accounting principles, and familiarity with the EIA-748 Standard for EVMS Guidelines. Professionals who wish to get a professional certification should review the specific eligibility requirements as dictated by the certifying body to ensure they qualify to undergo the certification process.

Detailed Step-by-Step Guide to the Professional Certification Process

- Research and Select a Certifying Organization: Begin by identifying an organization that offers an EVM Certification.

- Undergo Formal EVM Training: Enroll in and complete a formal training program that covers the core components of Earned Value Management. This step is pivotal, as it lays the groundwork for the practical application and understanding of EVM. Humphreys & Associates provides online EVM Training for employees of contractors that do business with the DOD, DOE, NASA, and other U.S. government agencies such as the FAA.

- Study the Standards and Guidelines: Gain a comprehensive understanding of industry standards, such as the EIA-748 Guidelines. Knowledge of these standards is fundamental, as they will inform the set-up and management of an EVMS.

- Prepare for the Examination: Most certifications will require passing an exam to demonstrate your proficiency. This will involve rigorous study and attending review courses to prepare.

- Apply for the Certification Exam: Submit your application along with any necessary documentation and fees to the chosen certifying body. Ensure all prerequisites have been met before applying.

- Take the Certification Exam: Schedule and sit for the certification exam. This will typically cover a range of topics, from the basic principles of EVM to more advanced concepts.

- Receive Certification: Upon successful completion of the exam, you will receive your EVM Certification, which endorses your knowledge and understanding of EVM.

Essential Documentation and Preparation Tips

To ensure a smooth certification process, maintain an organized file of all coursework, training certificates, and professional references. Consider using study guides, practice exams, and other preparatory materials to fully equip yourself for the certification exam.

How to Maintain and Renew EVM Certification

An EVM Certification is not a one-time event but requires ongoing professional development to maintain. Stay abreast of any Continuing Education Units (CEUs) or Professional Development Units (PDUs) required to keep your certification active. Engage with the community of practice, attend EVMS workshops, and continue learning to stay current in Earned Value Management best practices.

Section 3: EVM Consulting and Expert Guidance

The Need for Expert Consultancy in the Professional EVM Certification Process

As professionals navigate the path towards EVM certification, expert consultancy can play a pivotal role. These consultants have extensive experience with EVM principles and the process for implementing an EIA-748 compliant EVMS. They can offer personalized guidance, which is often critical to ensuring a smooth and successful journey to compliance with EIA-748 Standard for EVMS.

How to Choose the Right EVM Consultant

When selecting an EVM consultant, consider the following criteria to ensure you make an informed decision:

- Experience and Credentials: Look for consultants with a proven record of accomplishment in EVMS implementations and a robust portfolio of successful client engagements. Certified consultants, particularly those with additional qualifications in project management, bring a wealth of knowledge.

- Industry Reputation: Investigate the consultant’s standing within the industry through testimonials, case studies, and peer recommendations. A reputable consultant will have positive feedback and be recognized as an authority in the field.

- Approach to Training and Consulting: Evaluate the consultant’s methodology. The right consultant should offer a tailored approach, adapting their expertise to your organization’s specific needs and challenges.

- Compatibility with Organizational Culture: Ensure the consultant’s style and communication align with your organization’s culture. A collaborative and adaptable consultant can integrate more seamlessly into your team.

- Maintenance and Support: It is not just about successfully completing a Cognizant Federal Agency (CFA) EVMS Compliance Review, it is also about sustaining the EVMS and how project personnel implement it on their project. Check whether the consultant offers support and guidance to ensure ongoing compliance and effectiveness.

The Role of Consultants in Ensuring Compliance and Efficient System Implementation

An EVM consultant’s role extends beyond just advice on CFA compliance reviews—it involves hands-on assistance in setting up an EVMS that complies with industry standards, training staff to understand and use the system effectively, and preparing the organization for the rigorous CFA compliance review process. Furthermore, consultants can help identify any gaps in current practices and tailor the EVMS to best fit the organization’s unique environment.

By providing insights into best practices, drawing from a wide range of experiences with different clients, and offering objective assessments of current systems, consultants can ensure that an organization’s EVMS is both compliant and optimized for performance.

Earned Value Consulting provides valuable expertise that can streamline the CFA compliance process, facilitate the successful adoption of EVM, and ensure long-term compliance. By leveraging the knowledge and experience of a seasoned EVM consultant, organizations can overcome obstacles more efficiently and optimize their project management practices for greater success. Thus, engaging the right consultant is a strategic investment that can lead to significant dividends in project execution and management.

Section 4: EVM Training Course List

To enhance your skills in this area, H&A offers a comprehensive list of EVM Training Courses tailored to meet the needs of various stakeholders, from project managers to government contractors. Whether you’re preparing for a customer Integrated Baseline Review (IBR), seeking to improve your EVM proficiency, or aiming to pass professional certification exams, these courses offer valuable insights and practical experience. Delivered in an online format, these courses provide the flexibility to learn at your own pace while ensuring a deep understanding of EVM principles and their application in real-world scenarios.

CAM Discussion: The CAM Discussion serves as an essential component of the preparation process for a customer Integrated Baseline Review (IBR), compliance review, or surveillance review. This simulation offers a practical experience of a CAM documentation review and interview session, illustrating how a proficient CAM conducts an interview with a government customer. Additionally, it provides a useful recap emphasizing key technical points along with suggestions for follow-up action items.

CAM Essentials_DOD: CAM Essentials provides comprehensive training to improve EVM proficiency and understanding of the basics. This online training bundle features the EVMS Virtual Learning Lab (DOD), Scheduling Virtual Learning Lab, and CAM Discussion courses, all available separately.

CAM Essentials_DOE: CAM Essentials offers comprehensive tools for improving EVM skills and understanding the fundamentals. This online training bundle includes the EVMS Virtual Learning Lab (DOE), Scheduling Virtual Learning Lab, and CAM Discussion courses, each available separately.

CAM Essentials_NASA: CAM Essentials provides comprehensive training to improve EVM proficiency and understanding of the basics. The online training bundle includes the EVMS Virtual Learning Lab (NASA), Scheduling Virtual Learning Lab, and CAM Discussion courses, which are also available individually.

CPR/IPMR/CFSR Completion and Reconciliation: The Integrated Program Management Report (IPMR) and Contract Funds Status Report (CFSR) are crucial communication tools between contractors and their customers. This online course provides valuable insights into the proper completion of these reports and their reconciliation.

EVMS Certification and Preparation Quiz: This online course comprises 120 questions in four separate quizzes, covering the nine EVMS process groups, the Integrated Program Manager Report (IPMR), earned value data analysis, Integrated Baseline Review (IBR), and compliance reviews. It serves as an excellent study and preparation resource for the AACE International Earned Value Professional (EVP) or the PMI Project Management Professional (PMP) certification exams.

EVMS DOD Virtual Learning Lab: The EVMS Virtual Learning Lab offers a comprehensive 21-hour instruction program. This online training delivers Humphreys & Associates’ acclaimed three-day EVMS workshop in an interactive, multimedia format. The video content includes all workshop coursework, quizzes, and case studies, allowing students to assess their understanding and receive prompt feedback through scored quizzes and exams.

EVMS DOE Virtual Learning Lab: The EVMS Virtual Learning Lab offers a comprehensive 21-hour online training program. This interactive multimedia format is based on Humphreys & Associates’ acclaimed three-day EVMS workshop, delivering all course content, quizzes, and case studies in a video format. Students can assess their understanding through scored quizzes and exams.

The course can be used for project personnel to enhance their EVM proficiency or for someone who wants to learn the basics of earned value management at their own pace.

EVMS NASA Virtual Learning Lab: An intensive 21-hour online training program that offers a complete presentation of Humphreys & Associates’ three-day EVMS workshop. The course has been adapted into an interactive multimedia format, including all quizzes and case studies from the original workshop. Students can test their knowledge and receive immediate feedback through scored quizzes and exams.

The course can be used for project personnel to enhance their EVM proficiency or for someone who wants to learn the basics of earned value management at their own pace.

IBR – Online Video: The Integrated Baseline Review (IBR) course is designed to provide a comprehensive understanding of the IBR process. It is a fast-paced presentation that is essential for ensuring a clear grasp of the technical requirements of a project and establishing accurate schedule and cost goals. This course offers a detailed explanation of the review process and can be tailored to provide training for specific needs and timings. The approximate duration of the course is 2 hours.

OTB/OTS Implementation – Online Video: Learn about Over Target Baseline (OTB) and Over Target Schedule (OTS) Implementations in this approximately 1 hour and 30-minute video.

A formal re-programming action, known as an OTB and/or an OTS, may occur during risky major acquisitions. Understanding the rationale for and the various methods used to implement an OTB/OTS, as well as correctly completing the IPMR formats in accordance with the Data Item Description (DID) instructions, is not a simple process. Our video provides clarity on this complex process.

The video includes completed IPMR Formats 1, 2, and 3, showcasing four OTB methods, along with before and after Baseline graphs for each method. It also contains examples and Baseline graphs for Over Target Schedule, Format 3.

Scheduling Virtual Learning Lab: The Scheduling Virtual Learning Lab offers an intensive 21 hours of instruction covering critical path fundamentals, schedule baseline, float, network logic development, risk assessment, changes, and scheduling in an EVMS environment. The content is based on the well-regarded three-day Project Scheduling Workshop by Humphreys & Associates, adapted to a video format and featuring quizzes and case studies for immediate knowledge testing and feedback.

The course is designed for project personnel looking to enhance their project scheduling skills and for individuals who want to learn the fundamentals of project scheduling at their own pace.

A student who completes the Scheduling course will earn 21 Professional Development Units (PDUs) or 2.1 Continuing Education Units (CEUs).

Evaluating the Effectiveness of Your EVM Training

To ensure that the EVM training investment yields the expected results, it is important to monitor and evaluate its effectiveness. This can be done through various means, such as feedback surveys, performance assessments, and observing improvements in project management practices post-training. Metrics like increased efficiency, reduced project variances, and improved forecasting accuracy can indicate the success of the training program.

Additionally, incorporating a continuous improvement process for training—where feedback is used to refine and enhance the training offerings—can help ensure that the organization continues to improve on your EVMS over time.

Properly tailored EVM training programs are not the only key to successful professional certifications and EVMS implementation—they empower organizations to achieve strategic objectives and enhance overall project management proficiency. With the right training program, professionals and teams can develop the expertise needed to leverage EVM capabilities fully, leading to improved project outcomes and sustained success.

The journey through the complexities of building an Earned Value Management System (EVMS) underscores its pivotal role in effective project management. By committing to understanding the basic principles of an EVMS and striving for formal certification, professionals elevate their ability to forecast, monitor, and steer complex projects toward success.

EVM training equips project teams with the tools and strategies necessary to implement and manage robust project control systems. This, in turn, fosters informed decision-making, enhanced accountability, and improved alignment between project objectives and outcomes. Professional certification recognizes proficiency that benefits the individual and the organization by establishing credibility and assurance in project management capabilities.

Having traversed this guide, the next steps involve consolidating your newfound knowledge and venturing into tailored training programs that suit your or your organization’s specific requirements. From here, it is essential to consistently apply, adapt, and refine the skills gained through training to real-world scenarios.

Encourage yourself and your peers to persist in your journey towards EVM mastery. Continued learning, networking with other EVM professionals, and staying abreast of evolving practices will ensure that your expertise remains current and beneficial. May this guide serve as both a foundation and steppingstone on your path to excelling in the discipline of Earned Value Management.

For information on Corporate or Quantity Discount pricing, please contact us at products@humphreys-assoc.com or call us at (714) 685-1730.

Comprehensive Guide to EVMS Training Read Post »