Executive Level Schedules: Humphreys & Associates Methodology for Top Level Program Schedule Road-Mapping

Methodology for Top Level Program Schedule Road-Mapping

The lack of a useful, concise, easily understood top level plan for a project is an issue that our consultants have repeatedly noted. It is way past time for the adoption of more useful and understandable executive level schedules. Having a distinctive top level plan linked to the lower level Integrated Master Schedule (IMS) planning can help differentiate one approach or one project from another.

With the advent of modern scheduling software such as Microsoft Project or Primavera, we have been assisting clients in developing more and more complex Integrated Master Schedules. However, a bigger and more complex IMS does not make the project plan any more accessible or understandable. In fact, it makes having an attractive and useful top level schedule more important.

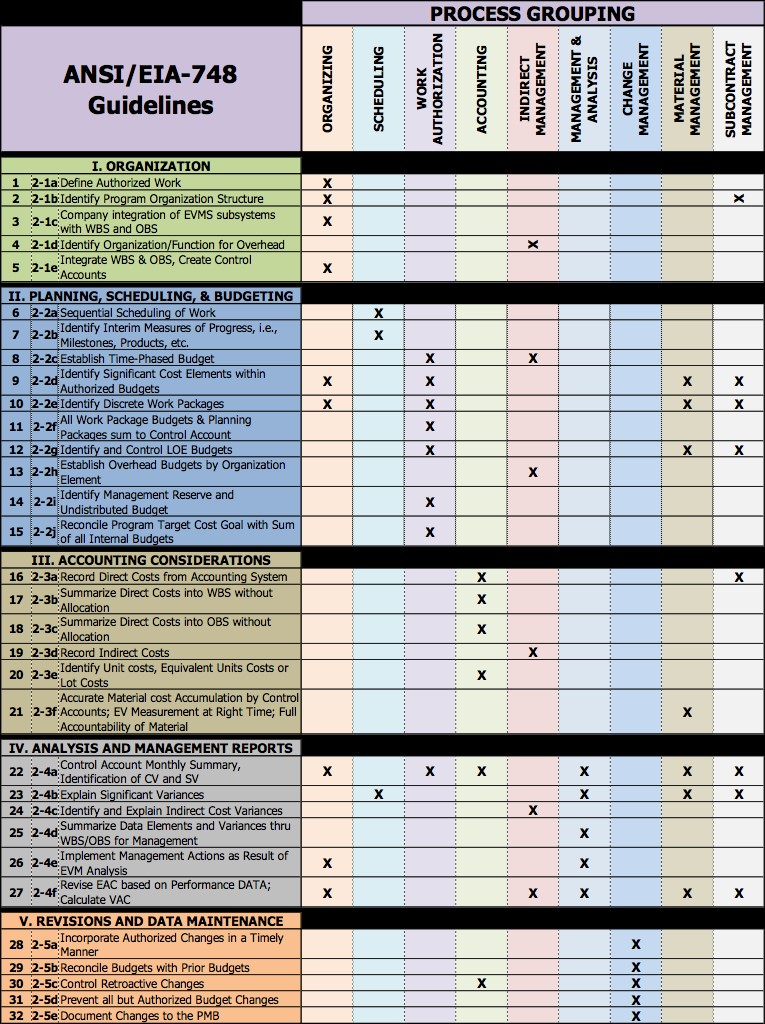

The Data Item Description (DID) that governs the IMS, the Integrated Program Management Report (IPMR) DI-MGMT-81861, requires a Summary Master Schedule and describes it as:

3.7.1.3.2 Summary Master Schedule. A top-level schedule of key tasks/activities and milestones at the summary level which can be sorted by either the Work Breakdown Structure (WBS) or IMP structure (if applicable). It shall be a vertically integrated roll up of the intermediate and detailed levels within the IMS.

The Planning & Scheduling Excellence Guide (PASEG) developed by the NDIA Program Management Systems Committee is a wonderful resource for schedulers. The guide discusses the Summary Master Schedule in a way that avoids specifying it is to be sorted either by WBS or by Integrated Master Plan (IMP) the way the data item description does. It also does not describe the top level as a roll up. The PASEG describes the Summary Master Schedule as:

Summary Master Schedule – The Summary Master Schedule is ideally a one (1)-page schedule and may also be called a Master Phasing Schedule (MPS), Master Plan or Summary Schedule. As the highest, least detailed schedule, the program’s summary master schedule highlights the contract period of performance, program milestones, and other significant, measurable program events and phases.

The Program Team initially develops the program summary master schedule from the analysis of requirements data during the pre-proposal phase and similar past program efforts. The program team review and approve the program’s top-level schedule, which serves as a starting point in the Top Down planning approach (See Top Down vs. Bottom up Planning). This process continues until contract award to include any changes caused by contract negotiations.

Key components of summary master schedules could include significant items from the following list:

-

- Key elements of contract work

- Test articles

- Deliverable hardware, software, and documentation

- GFE/customer-furnished equipment deliveries

- Key program and customer milestones/events over the life of the contract

- Subcontract elements

The PASEG further describes the process for developing the Summary Schedule. H&A agrees that this process is the effective one for creating an executable plan. The process makes the top level summary schedule even more important. The process outlined by the PASEG is:

-

- Read and understand the RFP.

- Make a high level plan to meet the requirements of the RFP.

- Use the high level plan to guide the top-down development of the IMS. This includes building the milestones that represent the Integrated Master Plan (IMP) events, accomplishments, and criteria.

- Validate lower level planning back against the top down plan.

In addition to the Data Item Description and the PASEG, H&A suggests that the Summary Schedule have some specific attributes that make it useful. It should be:

-

- Complete – show the key milestones and the entire project top to bottom and across time at a level of condensation that makes sense and is natural to the project.

- Easy to read – graphically it should portray the plan in a visually pleasing way that is easy to read.

- Easy to follow – flowing from left to right and top to bottom in a sequence that follows the progression of the work of the project.

- Self-explanatory – it should tell the story of the project even if adding notes are needed to make the story stand out.

Because the graphics in the IMS tools do not provide those attributes, H&A most often sees clients building some sort of “cartoon” plan, manually drawn in Excel or PowerPoint, and used during the proposal phase until the IMS can be considered solid enough to start using the roll up in the IMS as a Summary Schedule. The problem with this approach is that it is not linked electronically to the IMS; it is not part of the IMS and the data in the two can easily become different.

The maintenance of the cartoon version is continued in some cases or abandoned. When it is continued it involves labor effort to draw and redraw the plan based on changes and updates. Often the cartoon is abandoned and the roll up approach from the IMS tool takes over. At this point the top level executive type schedule no longer exists and the project plan is no longer readily accessible.

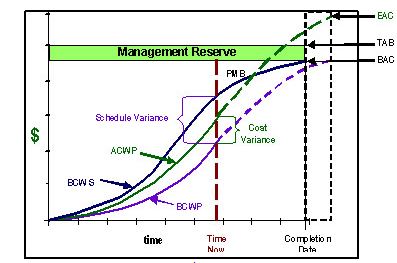

One of the main benefits of having an executive level summary schedule is that the program manager and team can easily tell the story of the project in a one page, coherent, easily understandable plan; and with the proposed methodology this summary schedule is linked to the IMS so the two do not become separated.

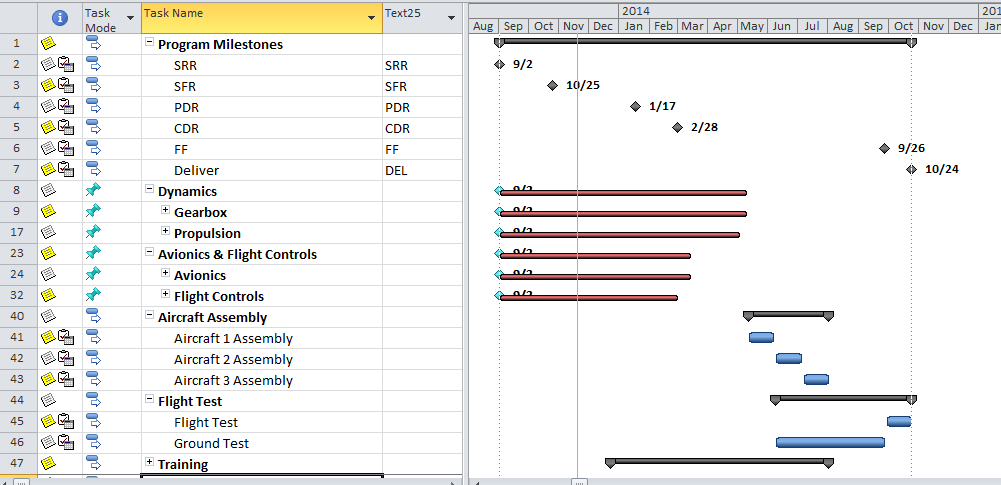

Looking at the two examples of a master schedule for the same project shown below, it is apparent that the first one is from Microsoft Project; it has the roll up look and feel to it. The summary bars do not really provide much information other than to indicate there is more information below.

The other example from the H&A methodology is a top level schedule that tells the story of the project in a form that flows the way the project does. It may be in WBS or OBS order but those may not be natural to the flow of the project. This example is grouped in the order that displays the evolution of the project the way the team thinks of the project. The tie to the underlying IMS is built into the plan. Each milestone or bar on the top level represents one or more tasks within the IMS so a user can find the identification of the corresponding work in the depths of the IMS when needed.

H&A now has developed a methodology supported by commercially available software that follows the guidance of the NDIA Planning & Scheduling Excellence Guide (PASEG) and provides the ease of use and executive level visibility needed in a top level schedule. Now a project can have a useful and demonstrative top level schedule that drives the top down planning effort as recommended in the PASEG.

This methodology was recently used successfully in the aerospace industry to develop the top level executive schedule view that drove the planning of a proposed multi-billion dollar project and to tell the story of the proposed project convincingly. The benefits perceived in that instance were:

- Enhanced communication with the customer – the story could readily be told on one page.

- Enhanced communication with company executives – they could easily see what was being planned by the proposal team.

- Top down planning from the proposal leadership into the Integrated Product Teams (IPTs) early in the proposal process when it counted most and kept all the teams focused on the same plan – everyone knew the plan.

- Establishment of the System Engineering approach and the Technical/Program reviews as the key points in the plan.

- Top down electronically linked planning into the Integrated Master Schedule (IMS) so that the development of the 5000 line proposed project schedule could be compared upward to constantly verify that the developing plan would support the top level plan.

- Establishment of time-fences that alert proposal leadership when lower level plans were moving away from established time goals.

- Rapid effective translation of the developing IMS into the understandable project plan – especially useful in planning meetings within the proposal teams.

- Because the top level is linked to the lower level, it can be used in meetings to rapidly isolate and find sections of the lower level IMS relating to a particular topic – no more paging, filtering, and searching for a particular area of the project’s IMS.

- Proposal quality graphics that did not require artists or artwork to tell the story.

To learn more about the H&A top level project road-map methodology and other EVMS topics, visit our website or call us to discuss your project.

![]()

")