A common Earned Value Management System (EVMS) compliance and surveillance review finding are issues with a contractor’s estimate at completion (EAC) process. A credible EAC is essential to successfully manage all contracts and projects.

EACs are important because they provide a projection of the cost at contract or project completion, which is also an estimate of total funds required by the customer. It matters because EACs represent real money. When the most likely EAC exceeds the negotiated contract cost, the contractor’s profit margins may be at risk. It also creates a problem for the customer when the most likely EAC exceeds their funding limits.

We recently updated our blog titled Maintaining a Credible Estimate at Completion (EAC) to highlight why this is a good time to review and potentially update your estimate to complete (ETC) and EAC processes. The updated blog added content specific to:

Incorporating integrated master schedule (IMS) analysis to test the realism of the EAC to identify any disconnects with the cost-based independent EACs (IEACs). It is equally important to determine a realistic forecast completion date (FCD).

Ensuring control account managers (CAMs) are in a position to substantiate their schedule timeline, resource requirements, and cost estimate to complete the remaining work. It is equally important that project managers proactively take the action of “scrubbing” the CAM’s detail ETC/EAC and verifying the data to gain a better understanding of the project’s current state. This improves the quality of the project-level forecast completion date as well as the range of project-level EACs.

Suggested actions to review and enhance current processes from basic steps, such as incorporating an analysis of the IMS Current Execution Index (CEI) to gain an understanding of how well project personnel can forecast into the future, and taking advantage of AI tools to provide additional data analysis insight.

In addition, the publication of the EIA-748-E Standard for EVMS revised 27 guidelines and related updates to government agency guidance such as the DoD EVMS Interpretation Guide (EVMSIG) will require contractor’s to review and remap EVM System Description content to the revised set of guidelines. The updated blog emphasizes this is a good time to revisit internal ETC/EAC processes and procedures to determine where improvements can be made as well as to ensure project personnel are following the documented processes. The EIA-748-E split the EIA-748-D Guideline 27 into two guidelines. The EIA-748-E Guideline 20 is specific to the control account level EACs and Guideline 23 is specific to the project level EACs. An EVM System Description should have content specific to the process at the control account level as well as the project level that can easily be mapped to the EIA-748-E Guidelines 20 and 23.

Do Your Internal Processes and Procedures Need a Refresh?

H&A earned value consultants routinely assist contractors with updating their internal processes and procedures to reflect the evolving EVMS requirements and guides, regulatory environment, and toolset capabilities. Workflow steps can often be simplified and the quality of performance analysis can be improved with a refreshed approach that reduces the time needed to produce reliable and actionable information. Call us today at (714) 685-1730 to get started.

A budget is a project management metric used to plan and measure performance, while funds are real dollars recorded in the accounting system and spent to perform the work.

Earned Value Management distinguishes planned values (e.g., BCWS, BCWP, BAC) from actual costs and estimates (e.g., ACWP, ETC, EAC) to provide insight into project performance and funding needs.

Contract funding profiles influence how budgets are time-phased, and regular EAC analysis is essential to forecast total funding requirements and avoid breaching funding limits.

While working with numerous clients over the years, H&A earned value consultants frequently observe people using the term “money.” Typically, they mean “funds” when they really mean “budget.” People often confuse the terms, even though they have been used within the project management community long before the advent of earned value management practices.

The intention of this blog is to highlight the difference between “budget” and “funds” and promote a common understanding of the terms. Using the correct term helps to eliminate confusion and improve communication between project team members, management, and the customer.

Examples of Budget and Funds Confusion

Here are a couple of common statements H&A earned value consultants have heard many times:

I am requesting management reserve (MR) to fund my overrun.

I underran my budget, so I am going to return funds to MR.

Why are these inaccurate statements? The people making them have confused the terms or may think that “budget” and “funds” mean the same thing.

Explaining the Difference Between Budget and Funds

The simple definition is that “budget” is a project management metric, a planned value. It cannot be used as funds (i.e., money) to buy something tangible, such as a cup of coffee. “Funds” are real dollars. The purpose for budget is to measure project performance so that as funds are expended (the actual costs) to perform the authorized work, any difference, more or less than what was planned, can alert management.

The table below summarizes the differences between the two terms.

Budget

Funds

Cannot be spent

Money – real dollars being spent or forecasted to be spent. Funding represents the customer’s ability and commitment to pay.

A number on a piece of paper, in a spreadsheet or database – it is a project management metric

Actual costs recorded in the accounting system of record used for financial reporting

Budgeted Cost for Work Scheduled (BCWS)

Time phased budget for required resources to accomplish tasks scheduled in the integrated master schedule (IMS)

Forms the performance measurement baseline(PMB)

Estimate to Complete (ETC)

Funding required to complete the remaining work, exclusive of prime contractor fee

ETC plus ACWP results in the Estimate at Completion (EAC)

Budgeted Cost for Work Performed (BCWP)

The budget value for completed work

Actual Cost of Work Performed (ACWP)

The costs incurred and recorded to accomplish the work performed

Budget at Completion (BAC)

Budget representing all authorized scope of work (SOW)

Cannot change without a change to the SOW with appropriate approval

Estimate at Completion (EAC)

Funding number representing all the money (at the cost level – does not include fee) that will be spent

Can change without a commensurate change in the SOW

An Overview of Budget Terms

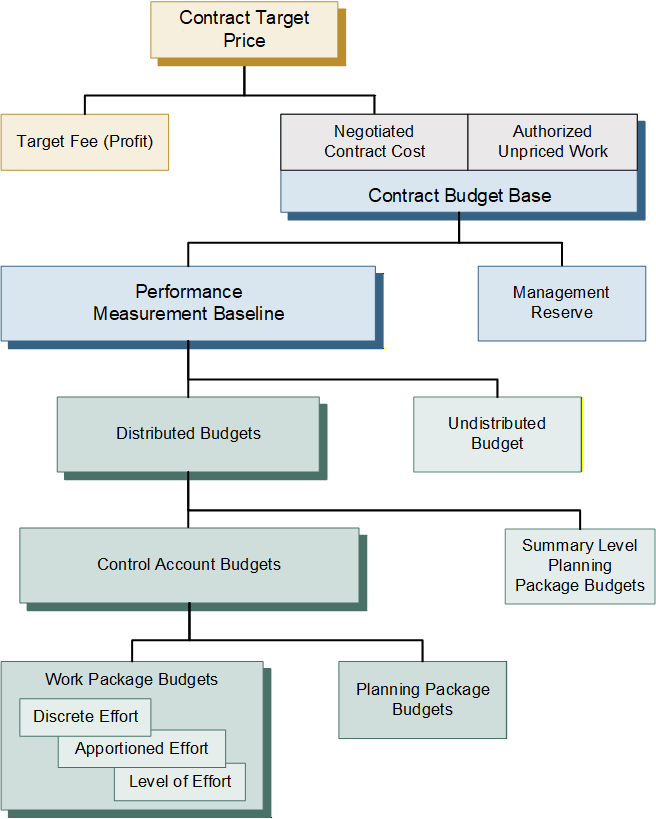

It is often helpful to review the basis for determining and distributing a project’s total budget used for planning and measuring project performance, as illustrated in Figure 1. Note: this is a simplified discussion to highlight the budget terms and does not include nuances such as an Over Target Baseline (OTB) situation.

Figure 1: Budget Distribution and Terms Illustrated

The budgeting process begins with the Contract Target Price (CTP). This is the total negotiated contract value. It includes the negotiated contract cost (NCC) plus the contractor’s planned (target) profit or fee. The Contract Budget Base (CBB) is the starting point for a contractor’s internal budgeting process outlined below.

Budget Component

Definition

Contract Budget Base (CBB)

Represents the financial authorization of the contract and is based on the negotiated contract cost (i.e., price less fee). The CBB is always equal to the negotiated cost for definitized work and the estimated cost for all authorized unpriced work (AUW), also known as Undefinitized Contact Action (UCA). The CBB equals the sum of distributed budgets, undistributed budget, and management reserve (MR). It also equals the sum of the performance measurement baseline (PMB) and MR.

Management Reserve (MR)

Amount of contract budget set aside to handle realized risks and emerging in-scope effort. This effort is in scope to the contract, but out of the scope of distributed and undistributed budget.

Performance Measurement Baseline (PMB)

The PMB is the sum of all distributed direct and indirect budgets against which contract performance is measured. The PMB is the sum of the distributed budgets and undistributed budget. The PMB plus MR is equal to the CBB.

Undistributed Budget (UB)

Budget for authorized work scope that has not yet been identified to a specific WBS element and/or responsible organization at or below the lowest level of reporting to the customer.

Distributed Budgets

Distributed budgets may be comprised of summary level planning package (SLPP) and control account budgets.

Summary Level Planning Package (SLPP) Budgets

Budget may be set aside in SLPPs at the lowest WBS element until the future work effort can be defined in more detail. SLPPs have a high-level scope of work and are scheduled in the IMS with time-phased budgets. They are converted to one or more control accounts with subordinate work packages and planning packages as soon as possible.

Control Account Budgets

Control accounts have a defined scope of work, scheduled start and finish dates, and time-phased budget that reflects the work decomposed to the work package or planning package level. The sum of the time-phased work package and planning package budgets equals the total control account budget.

Work Package/Planning Package Budgets

Work packages and planning packages have a defined scope of work, scheduled start and finish date, and time-phased budget based on the parent control account. This lowest level of budget includes the element of cost detail (labor, material, subcontract, and other direct costs) and value detail (hours, units/quantities, direct costs, and indirect costs).

Notes about Management Reserve

Remember that MR is a budget, is not a financial reserve (i.e., a source of funds). It is not time-phased and is not included in the PMB because there is no related work scope, although it is a part of the CBB. MR budget cannot be used to eliminate cost variances, cover cost overruns, or recover underruns. There is only one MR set aside for a project and the value is never negative.

MR is decreased to provide budget for realized risks or unplanned activities within the contract scope of work. It may be increased whenever the work scope is decreased along with the allocated budget (a contract modification). Customer authorized contract changes, including AUW, should be incorporated into the CBB and PMB as soon as possible; this may include MR budget set aside for added work scope. Only contract changes authorized by the customer’s designated contracting officer may change the CBB value.

Additional note. The MR budget belongs to the contractor’s program manager, not the government customer. MR is not a cost reserve (contingency) for the government customer and may neither be eliminated from contract prices by the customer during subsequent negotiations nor used to absorb the cost of contract changes. For the government customer, contingency is the cost reserve they own, typically associated with a Program Risk-Adjusted Budget (PRB). It is held outside of the project scope, schedule, and budget already provided to the contractor. Reserves held above the program permit senior government management to balance resources within portfolios and among programs. The government customer’s cost reserve could be used to modify the contract to include additional work scope (increases the contractor’s CBB) or provide the funds needed to cover a contract cost overrun.

Budget, Estimates, and Funding Profiles

Contract funding also influences how the PMB budget is allocated and time-phased. The budget distributions are a result of the project planning process (scope of work definition, detailed schedule development, initial cost estimates), MR set aside (risk and opportunity planning), and the funding profile. This is an iterative process to develop the baseline schedule and time-phased budget plan. The budget distributed to the control accounts and any SLPPs is compared to the total PMB/UB value. As needed, adjustments to activities, sequence of work, or resource assignments are made to ensure the overall budget plan reflects the budget limit for the PMB and the contract’s funding profile. For a real-world example of this, see this blog, Understanding the ALAP Scheduling Option in Practical Terms, where a front-loaded schedule was exceeding the funding cap, and how a H&A scheduling consultant helped resolve the issue.

Preparing an EAC every reporting cycle provides an accurate projection of cost at contract completion for internal and external management. It also represents the estimate of total funds required for the contract. The most likely EAC should be within the funding constraints for the contract. Any amounts expended in excess of the contract funding limit puts the contractor at risk. The contractor must notify the customer when their EAC analysis determines there is a potential to breach a funding constraint to address any contract funding issues as quickly as possible.

Figure 2 illustrates a funding profile along with the range of project EACs. In this figure, the most likely EAC is within the contract funding limit.

Figure 2: Management Level EACs with Funding Profile

Reinforcing a Commitment to EVMS Excellence

A common theme of the H&A blogs and articles is helping clients to achieve and maintain a commitment to a high level of excellence in all EVMS process areas. An important part of this is continuous EVM training and project scheduling training, whether for beginners or advanced practitioners. This includes targeted training when clients identify an area where project personnel could use a refresher, more hands-on training, or mentoring. Examples include basic and advanced EVMS workshops, Completing Variance Analysis Reports, Developing an ETC and EAC, as well as short, targeted courses on topics such as Budget versus Funds. Give us a call today at (714) 685-1730 to get started.

“When you need to discuss the schedule, look at the schedule.”

– A Scheduler’s Lament

There are many existing formulas for calculating an Independent Estimate at Complete (IEAC) from earned value data. A recent study of a sample of projects found that the calculated IEACs analyzed at the 25%, 50%, and 75% complete points were not accurate when compared to the final actual cost of work performed (ACWP). The following table lists the thresholds used to assess the accuracy of the IEACs at the different complete points for the sample projects.

Percent Complete

Accuracy Threshold

25%

Within +/- 10% of final ACWP

50%

Within +/- 7% of final ACWP

75%

Within +/- 5% of final ACWP

While working on that study of the accuracy of commonly applied IEAC formulas as well as on a small project as an analyst for a customer, the idea for using data directly from the integrated master schedule (IMS) in conjunction with the cost performance data to create a new IEAC formula emerged.

Using Data Directly from the IMS to Calculate an IEAC

It should be noted that none of the generally used IEAC formulas use data directly from the IMS. The IEAC formulas use data found in the cost performance portion of the earned value monthly reports to customers.

IMS data is only used indirectly in the IEAC formulas. When a task is started and progress updated, the earned value (the budgeted cost for work performed or BCWP) is developed from the progress reported. This is measured against the cost baseline (the budgeted cost for work scheduled or BCWS).

At the same time, in the IMS environment, the schedule analysts are calculating the Baseline Execution Index (BEI) for task completions/finishes. BEI (for finishes) measures how many of the tasks baselined to be completed by the cut-off date were completed. If all the tasks were done (BEI = 1), their value would have been earned. Of course, other tasks could have started, progressed, and maybe even finished. For this example, the Schedule Performance Index (SPI) calculated at that point (BCWP/BCWS) should be at least 1 and potentially higher. The SPI reflects the baseline value of completed tasks plus the in-process claimed baseline value. The in-process claimed value can be subjective in some cases.

The argument, if there were one, might be there is no need to try and include BEI or similar schedule measures in the IEAC formulas since they already include SPI.

However, there is a whole different and unique set of information coming from the IMS that is not currently used in the IEAC formulas. That information is what we chose to call “Duration Performance” and “Realism Ratio.” These are measures of the actual duration for completed tasks and the forecast duration for future tasks.

Calculating Duration Performance

The IMS data includes the baseline number of days assigned to each task as well as the actual number of days to complete each task. If a task is baselined to take 10 days (Baseline Duration = 10) and the task took 15 days to complete (Actual Duration = 15) then it is taking 150% of baseline to do the work.

This is similar to the Cost Performance Index (CPI) that uses the BCWP and the ACWP to determine how efficient the work performance has been. The formula BCWP/ACWP shows how the work accomplished compares to the cost of that work performed.

If we assume, for labor at least, that taking longer to complete a task often leads to costing more than baselined, we can use the Duration Performance to develop an IEAC.

To develop the Duration Performance, we would use the IMS from the month being analyzed to perform the following actions:

Filter out all summary tasks and look only at real work tasks.

Decide what to do with level of effort (LOE) – keep it or ignore it.

Filter for all tasks that are completed (100% complete).

Add up the baseline duration in days for all these completed tasks.

Add up the actual duration days for these same completed tasks.

Compare the actual duration days used to the baseline duration days.

An example would be:

100 completed tasks

Total baseline days duration = 1,000

Total actual days duration = 1,500

Duration Performance = 1,000 / 1,500 = .67

One of the common IEAC formulas is the “SPI times CPI” that is calculated like this: ACWP + Budgeted Cost of Work Remaining (BCWR) / (CPI x SPI) where BCWR = Budget at Completion (BAC) – cumulative to date BCWP.

Now that we have a duration performance factor, we can develop a new IEAC. The Duration Performance IEAC would be done using the CPI from the same month as the IMS where ACWP + BCWR / (CPI x Duration Performance Index).

Using some actual data from a project for a single month we see:

Duration Performance Index = .82

BEI = .72

CPI = .92

SPI = .94 (significantly higher than the BEI)

ACWP = $9.2M

BCWR = $18.3M

IEAC using standard formula with CPI x SPI = $9.2 + $18.3 / (.92 x .94) = $30.3M

When we look at the remaining tasks to be completed, we can use the Realism Ratio to assess how the future forecast durations compare to the performance so far.

The data needed are the baseline duration and the forecasted duration for all tasks that have not been started. This concept excludes in-process tasks. In our example from before, the data we created looked like this:

100 completed tasks

Total baseline days duration = 1,000

Total actual days duration = 1,500

Duration Performance = 1,000 / 1,500 = .67

We would use the same IMS to do this:

Filter out all summary tasks and look only at real work tasks.

Decide what to do with LOE – keep it or ignore it.

Filter for all tasks that are not started.

Add up the baseline duration in days for all these tasks not started.

Add up the forecasted duration days for these same tasks not started.

Compare the forecasted duration days to the baseline duration days.

Let’s say there were 100 tasks not started. If the forecasted days were 1,000 and the baseline days were 1,000 that would yield 100%. When we did the example, the Duration Performance was .67. This means that performance to date was .67 but the future will be 100% or 1. You can see the disconnect. That disconnect we call the Realism Ratio (in this example, .67/1).

Data from the actual project for the same month as discussed earlier shows:

Duration Performance = 122% of baseline

Future Performance = .86 or 86% of baseline.

This means that the future durations are cut significantly.

We would use this data to develop a factor called a Realism Ratio (86/122 = .70) and that would be used to develop an IEAC using this formula: IEAC (Realism Ratio) = ACWP + BCWR / (CPI x Realism Ratio).

Using the same sample project data from above and adding in an assessment of the forecasted durations for the remaining work, we see:

Duration Performance = .82

BEI = .72

CPI = .92

SPI = .94 (significantly higher than the BEI)

ACWP = $9.2M

BCWR = $18.3M

Realism Ratio = .70

IEAC using standard formula with CPI x SPI = $9.2 + $18.3 / (.92 x .94) = $30.3M

The project is not complete, so the final ACWP position is not known. There is a dramatic difference between the three IEACs. The difference between BEI and SPI indicates that in-process tasks and other factors such as LOE are potentially affecting SPI.

What can we learn from this sample project?

In this example, additional investigation is warranted. There are potential issues with the realism of the baseline and current schedule that are signaling a cost growth issue is likely to occur. Relying on just the time-phased cost data for IEAC calculations may not be sufficient to assess whether a contractor’s range of EACs included in their monthly cost performance reports are realistic. For more discussion, see the blog on Maintaining a Credible Estimate to Completion (EAC) and the blog on Using EVM Performance Metrics for Evaluating EACs.

Are there lurking cost growth surprises in your projects? You may want to consider revisiting your estimate to complete (ETC) and EAC process to verify there is an integrated assessment of the schedule and cost data to identify potential disconnects. H&A earned value consultants can provide an independent assessment of the quality of the data as well processes and procedures to help you verify your EACs are realistic. Call us today at (714) 685-1730.

“Data! Data! Data!” he cried impatiently. “I can’t make bricks without clay.”

-Sherlock Holmes, The Adventure of the Copper Beeches

There are many discussions about EACs and evaluating EACs including using Independent EAC (IEAC) formulae to compare with the contractor EACs. With good reason, we should wonder how accurate are those IEACs that we use so often and sometimes make decisions based on them. Are we misjudging contractor’s EACs based on formulae that are weak or inappropriate?

Humphreys & Associates has initiated a study to determine how accurate IEACs are, and we would like your help. The study will compare different IEAC formulae against the Program Manager (PM) most likely EAC at the 25, 50, and 75 percent complete point for completed projects. The objective is to assess how closely the IEACs and PM most likely EAC were able to predict the final cost outcome for the project.

How Accurate are IEAC Formulae?

Many formulae exist for using recorded data from an earned value management system (EVMS) to make independent estimates of the final cost at completion (EAC) for the element in question. The element might be a control account, a Work Breakdown Structure (WBS) element, or even an entire project.

What is not known is how accurate these methods are at forecasting the final actual cost for the project. This study hopes to determine that answer.

Real World IEAC Data

This study was initiated by collecting earned value data from 12 completed projects. We need projects that are completed because, on a completed project, the final actual outcome is known. We collected project data at the 25, 50, and 75 percent complete points. At each of these points, the IEAC formulae were applied to determine how closely they were able to predict the final actual cost outcome for the project. The quest is to learn how the various IEACs performed. Is any one of them more accurate than the others?

From this investigation, any indication of the relative efficacy of the formulae would be used to inform future use of the IEAC methods.

Our Method for Testing IEACs

In general, the IEAC approach is to use existing recognized formulae. We have chosen these IEACs as a starting point:

IEAC 1 = BAC/CPIe at the percent point reported. This formula can be stated in words as “the entire project is performed at the same efficiency as experience to date.”

IEAC 2 = ACWP + [BCWR/CPI (.5) + SPI (.5)]. This formula uses weighted SPI and CPI which theoretically allows for sensitivity to both cost and schedule historical performance. The weights used in this application are even at .50 and .50.

IEAC 3 = ACWP + [BCWR/CPI x SPI]. This formula uses the SPI and CPI multiplied together which theoretically allows for sensitivity to both cost and schedule performance to date.

IEAC 4 = ACWP + BCWR. This formula assumes the remaining work will be done as budgeted with no factoring.

One additional non-traditional IEAC will be used.

IEAC 5 = Use of IEAC 2 weighted SPI and CPI but decreasing the proportion applied to the SPI as the percent of project completion increases. In other words, the impact of schedule performance diminishes as the project becomes closer to completion.

We will also take the average of all the formulae to see how that works.

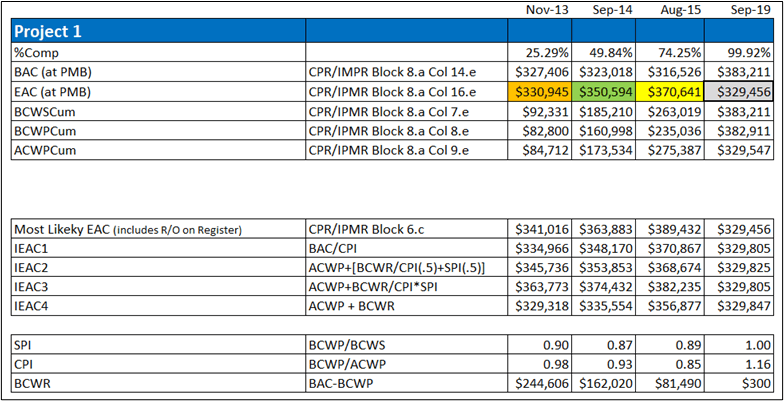

Initial Data Set

One aerospace contractor and one US Government agency have provided the required data for 12 completed projects with an interest in the outcome of the study. The source of the data and the specific projects will not be disclosed in the study.

These real-world projects did not have an exact 25%, 50%, or 75% dataset. The closest dataset to each of those completion percentages was used. One example dataset looks like this (color coding should be ignored):

How can you help?

We need more project data to gather enough varying project outcomes to make the test realistic. We do not plan to keep the types of projects or products separate but will take all the data we can get and look at them all.

Please consider providing data for the study. We have created an Excel spreadsheet template to help gather project data in a common format for analysis. You can download this template here. Add as many tabs as needed for each project. Send your completed spreadsheet to humphreys@humphreys-assoc.com.

In a separate blog we will outline other help we need to complete the study and to analyze the results.

A previous blog, Maintaining a Credible Estimate at Completion (EAC), discussed why producing a realistic EAC is essential to managing the remaining work on a contract. Internal management and the customer need visibility into the most likely total cost for the contract at completion to ensure it is within the negotiated contract cost and funding limits.

As noted in the earlier blog, one common technique to test the realism of the EAC is to compare the cumulative to date Cost Performance Index (CPI) to the To Complete Performance Index (TCPI).

Example of Using the Metrics for Evaluating Data

One example of documented guidance to industry for evaluating the realism of the EAC is the DOE Office of Project Management (PM) Compliance Assessment Governance (CAG) 2.0, and the related DOE EVMS Metric Specifications they use to assess the quality of schedule and cost data. This blog highlights the use of this guidance and how any contractor can incorporate similar best practices to verify EACs at a given WBS element, control account, or project level are realistic.

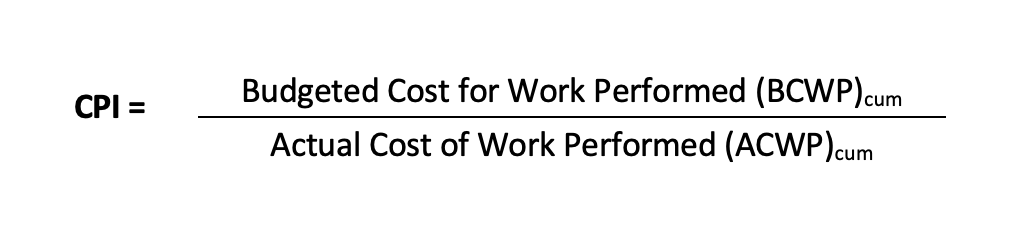

To refresh, the CPI is the efficiency at which work has been performed so far for a WBS element, control account, or at the total project level. The formula for the cumulative to date CPI is as follows.

Best practice tip: To ensure a valid CPI calculation, verify the BCWP and ACWP are recorded in the same month for the same work performed.

The TCPI provides the same information, however, it is forward looking. While the CPI is the work efficiency so far, the TCPI is the efficiency required to complete the remaining work to achieve the EAC. The formula for the TCPI is as follows.

Best practice tip: To ensure a valid TCPI, verify the BCWP and ACWP are recorded in the same month for the same work performed, and the BAC and EAC are for the same work scope. In other words, the scope of work assumptions are the same for the budget and remaining cost. This is why anticipated changes should not be included in the EAC.

The DOE uses the CPI in two of their assessment metrics and the TCPI in one, however, these are critical metrics partly because they are the only ones used to assess two different data evaluations: 1) commingling level of effort (LOE) and discrete work, and 2) EAC realism.

Commingling LOE and Discrete Work

The first use of CPI (no TCPI in this metric) falls under the Budgeting and Work Authorization subprocess. The primary purpose is to evaluate the effect of commingling LOE and discrete work scope has on control account metrics. The basic premise for this metric is that if the CPI for the LOE scope is significantly different than that for the discrete, the mixture of LOE in that control account is likely skewing overall performance reporting.

Here is the formulation DOE uses.

C.09.01: Control Account CPI delta between Discrete and LOE >= ±0.1

X = Number of incomplete control accounts (WBS elements) in the EVMS cost tool, where

The LOE portion of the budget is between 15% and 80% of the total budget, and

The difference between the CPI for the discrete work and the LOE work is >= ±0.1.

Y = Number of incomplete control accounts (WBS elements) in the EVMS cost tool.

Threshold = 0%

Best practice tip: Run this metric quarterly on your control accounts that commingle LOE and discrete work packages. When there is a significant discrepancy between the performance of the LOE versus discrete work effort, consider isolating the LOE effort from the discrete effort at the earliest opportunity. An example could be the next rolling wave planning window or as part of an internal replanning action. Alternatively, it may be necessary to perform the calculations at the work package level to assess the performance of just the discrete effort when it is impractical to isolate by other means.

Process and procedure tip: Ensure the LOE work packages within a control account are kept to minimum (typically less than 15%), during the baseline development phase. This helps to prevent discrete work effort performance measurement distortion during the execution phase. A useful best practice H&A earned value consultants have helped contractors to implement during the budget baseline development process is to perform an analysis of the earned value methods used within a control account and the associated work package budgets. This helps to verify any LOE work packages are less than the 15% threshold for the control account. In some instances, it may be logical to segregate the LOE work effort into a separate control account. The objective is to identify and resolve the issue before the performance measurement baseline (PMB) is set.

EAC Realism

One DOE metric uses the TCPI and this involves a comparison to the CPI. This falls in the Analysis and Management Reporting subprocess. This DOE EVMS Metric Specification states: “This metric confirms that estimates of costs at completion are accurate and detailed.” As noted above, the metric compares the cost performance efficiency so far to the cost efficiency needed to achieve the EAC and is specific to the EAC a control account manager (CAM) would review for their scope of work. Depending on the level actual costs are collected, this analysis may need to be performed at the work package level instead of the control account level.

Here is the formulation DOE uses assuming actual costs are collected at the work package level.

F.05.06: Work Package CPI – EAC TCPI > ±0.1 X = Number of incomplete (>10% complete) work packages where CPI –TCPI > ±0.1. Y = Number of incomplete (>10% complete) work packages in the EVMS cost tool. Threshold = 5%

There is no requirement that the forecast of future costs has a linear relationship with past performance. While there may be legitimate reasons why future cost performance will fluctuate from the past, outside reviewers who receive EVM data will look for a trend or preponderance of data that would indicate the EACs are not realistic. When a significant number of active work packages are outside the ±0.1 CPI-TCPI threshold, it is an indication that the EACs are not being maintained or are driven by factors other than project performance.

Best practice tip: Run this metric every month for each active work package prior to month-end close. For those work packages outside the ±0.1 threshold, review the EAC to ensure it is an intentional forecast of costs given the current conditions.

Process and procedure tip: One of the training courses H&A earned value consultants often conduct is a Variance Analysis Reporting (VAR) workshop. This workshop is designed to help CAMs become more proficient with using the EVM metrics to assess the performance to date for their work effort, identify the root cause of significant variances, and document their findings as well as recommended corrective actions. This analysis includes verifying their estimate to complete (ETC) is a reasonable assessment of what is required to complete the remaining authorized work and their EACs are credible.

Additional References

Further discussion on using the CPI and TCPI to assess the EAC realism at the project level can be found in the DOE CAG, Analysis and Management reporting subprocess, Estimates at Completion. This section provides a good overview of comparing the cumulative to date CPI to the TCPI as well as comparing an EAC to calculated independent EACs (IEACs) for further analysis to assess the EAC credibility.

Interested in learning more about using EVM metrics as a means to verify EACs at the detail or project level are realistic? H&A earned value consultants can help you incorporate best practices into your processes and procedures as well as conduct targeted training to improve your ETC and EAC process. Call us today at (714) 685-1730.

Originally published March 2023 | Revised May 13, 2026

Quick Summary

EVMS compliance and surveillance reviews continue to identify issues related to poor-quality estimates at completion (EAC), underscoring the need for credible EACs to support effective project management, financial integrity, customer confidence, and funding decisions.

Credible EACs require actively maintained, data-driven estimates to complete (ETCs) that integrate schedule, resource, cost, and risk information along with regular management realism assessments and open communications with all stakeholders.

Organizations can improve EAC credibility by avoiding management imposed targets, keeping schedule and cost systems aligned, routinely reviewing the quality of the ETC data, leveraging evolving tools and analytics, and updating processes to align with the revised EIA-748-E guidelines.

The Defense Contract Management Agency (DCMA) as well as other government entities responsible for Earned Value Management System (EVMS) compliance and surveillance continue to identify issues with the quality of contractor estimates at completion (EAC). Using DCMA statistics, EIA-748-D Guideline 27, Maintain Estimates at Completion, is one of three guidelines1 that represent a third of all EVMS Corrective Action Requests (CARs).

Why Credible EACs Matter

A credible EAC is essential to all stakeholders and a foundation for managing projects successfully. Executive management and project managers must have a complete and accurate understanding of the projected contract or project EAC to ensure financial data is not misrepresented (Sarbanes-Oxley). The customer must have confidence in a contractor’s forecast completion date (FCD) and EAC data to understand whether the remaining work can be completed within the contractual period of performance and target cost, or, if not, how long it will take and how much it will cost.

When the most likely EAC exceeds the negotiated contract cost, the contractor’s profit margins may be at risk. Should the most likely EAC exceed the customer’s funding limit, they will need to secure additional funding, modify the work scope, or slow the pace of the project. No one likes schedule or cost surprises.

What determines whether an EAC is credible?

A credible EAC reflects the cumulative to date actual costs of work performed (ACWP) (costs the contractor has already incurred) plus the current ETC. The ETC must provide a realistic estimate of the time and resources required to complete the remaining authorized work using projected rates. It represents the time phased estimate of spending which translates to the future funds required.

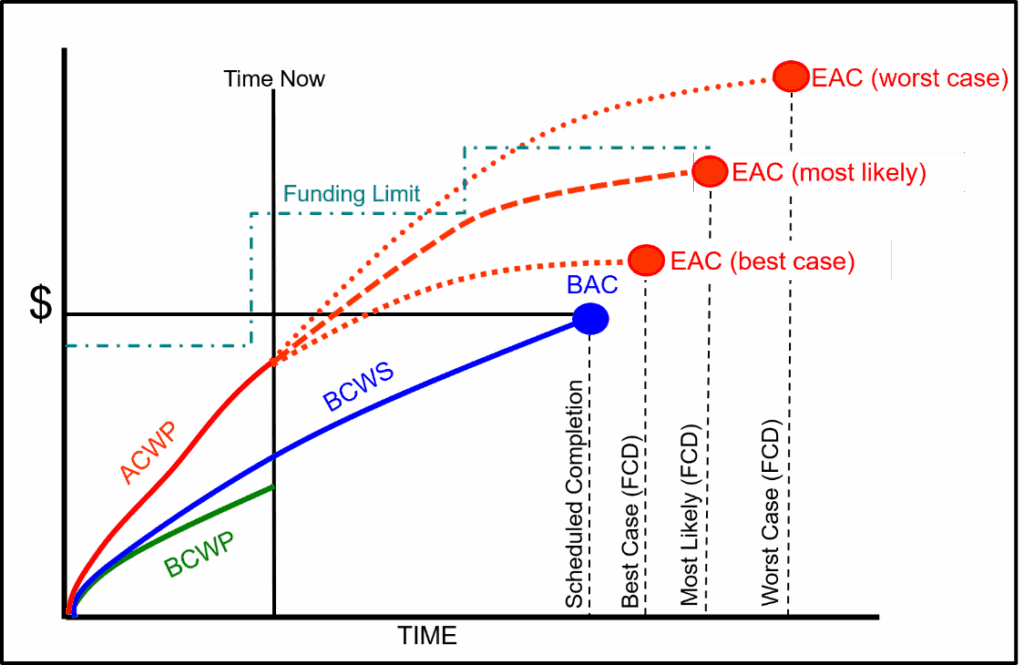

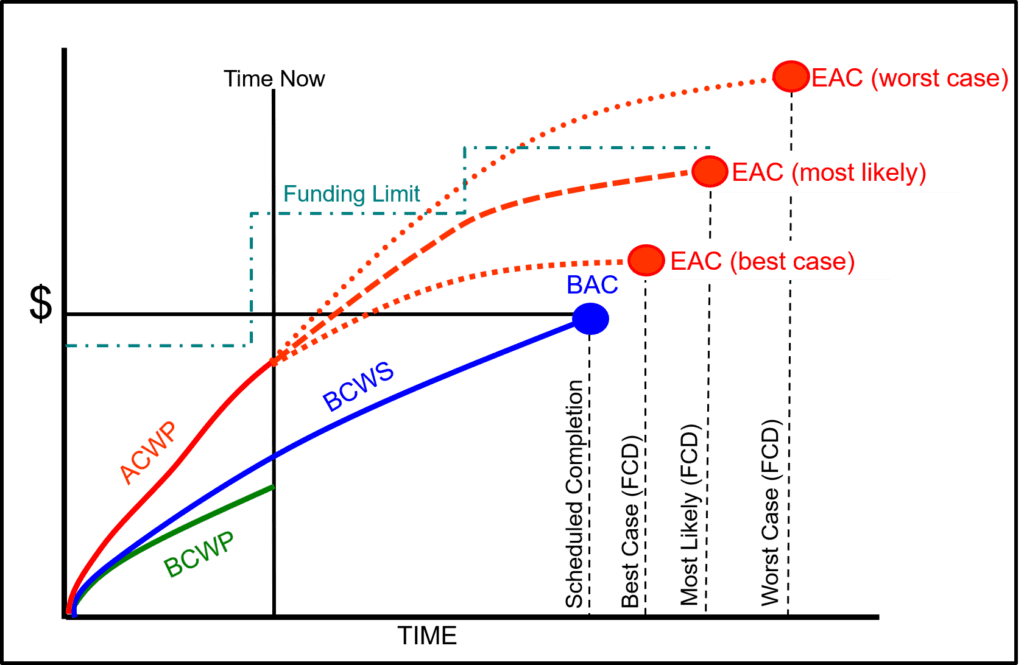

EACs should be based on actual costs and performance to date, the nature and amount of remaining scope, assumptions about and projections of future performance for that scope, risks and opportunities, economic escalation, expected direct and indirect rates, subcontract, and material commitments. As illustrated in Figure 1, project managers should routinely evaluate their project’s ACWP, ETC, and range of EACs along with the funding profile to verify amounts expended and forecasted are within the parameters of available contract funds.

Figure 1: Range of Project EACs with Funding Profile

What project control practices help to ensure EACs are realistic?

Three recommended best practices include:

Actively maintaining the detail ETC data every reporting cycle. This starts with updating the current schedule to include all authorized remaining scope along with the resource loaded activities to reflect performance to date and the latest planning (timing and resource requirements) for work in progress and future work effort. This is the basis for updating the time phased cost estimate for in progress work packages that is added to the cumulative to date actual costs as well as the cost estimate for future work/planning packages. Subcontract forecasted schedules and cost must be included. The current schedule forecast dates and time phased cost estimate must be aligned. Actively maintaining the detail data ensures the current schedule and ETC data reflect the project’s current state. The control account managers (CAMs) can substantiate their ETC with relevant data for analysis and take action to address a significant variance at completion (VAC).

Actively monitoring project FCDs and EACs. Project managers that routinely maintain a range of data driven FCDs and EACs (best case, most likely, and worst case) are better prepared to verify the control account FCDs and EACs are realistic, realized risks have been handled, and emerging risks have been identified, assessed, and addressed. Experienced practitioners use various metrics such as comparing the Cost Performance Index (CPI) to the To Complete Performance Index (TCPI) to test the realism of the EAC. They also include a realism check of the baseline and current integrated master schedule (IMS) to identify any potential disconnects with the cost-based indices discussed in a previous blog, Incorporating IMS Information Directly into IEAC Formulas. Managers should scrub the detail ETCs to assess the quality of the estimates and verify the content of the backup data. A good understanding of the detail ETCs is necessary to produce credible project level EACs with crisp rationale and narratives provided to executive management and the customer.

Maintaining open communications with all levels of management, subcontractors, and the customer. The project manager is the main conduit to manage impacts to their project’s FCD and EAC such as when finance changes direct or indirect rates, there are changes in resource availability or a spike in material prices, or the customer modifies the work scope or funding. As a result, project personnel can quickly handle issues or project changes. Direct and open communications with executive management ensures there is a clear understanding of their project’s FCD and EAC.

What are some things to avoid?

H&A consultants often observe practices that negate the value of maintaining the ETC/EAC and can result in an EVMS corrective action request (CAR). The root cause often points to ad-hoc processes or corporate culture. Examples:

Management provides a target FCD and EAC number the CAMs must match. The ETC/EAC should be “the voice of the CAM”. The CAM is saying “if you give me these resources as scheduled, I can finish the job this way.” Any approach that does not respect the voice of the CAM can cause the ETC/EAC to be unrealistic or at least unsubstantiated. Giving the CAM “the date and number” increases the likelihood the FCD and ETC are unrealistic. There may be a valid reason for this directive as a management what-if exercise or to gain a deeper understanding of the situation. When done as a routine management strategy, it diminishes the value of the ETC data to manage the project’s remaining work and prevent cost overruns. The CAMs should be in a position where they can substantiate their schedule timeline, resource requirements, and cost estimate to complete the remaining work. Project managers should be in a position where they can verify the detail ETC/EAC data to establish a level of confidence in their project level EACs they provide to executive management and the customer.

Project personnel take the path of least resistance. This is often an indication of a lack of direction or an established process. They either do not create the ETC data or maintain it on a routine basis. In some instances, the CAMs manage their ETC data to avoid oversight. An old but valid saying is “the tall grass gets mowed” – the CAM purposely doesn’t raise their ETC to a value that would attract attention. Another troublesome approach is to set a cost management tool option to a static EAC; the CAM may manually update the EAC number quarterly at best. The result? The FCD and ETC data isn’t current; there is zero insight into potential emerging issues. DCMA or the customer can easily identify this when they analyze the time-phased ETC data in the Integrated Program Management Data and Analysis Report (IPMDAR) Contract Performance Dataset (CPD) submittal.

Schedule and cost are created/maintained separately. This often occurs when the schedule and cost tools are not kept in sync for the project’s duration. Significant effort may go into ensuring the data are in alignment to establish the performance measurement baseline (PMB). The IMS resource loaded activities are used as the basis for the time phased budget baseline in the cost tool. However, the ETC data in the current schedule may not exist or be actively maintained. Project personnel only maintain the ETC data in the cost tool and fail to verify it aligns with the current schedule activity forecast dates and resource requirements. It is not part of their routine status and analysis process every month.

Taking Action to Review and Enhance Current Processes

A simple step to start with is to use the IMS Current Execution Index (CEI). This is a useful measure of how well a team can forecast just a single month into the future. If a team cannot achieve a high accomplishment rate against just a one-month forecast, any longer-term ETC is questionable. Start simple and focus on improving the one-month accuracy then move on to longer periods. Build confidence in the team’s ability to see and manage the future.

Another basic step. Build time into the process for managers to scrub ETCs. Maybe it is not possible to scrub every control account ETC every reporting period, but a rotational approach where ETCs are scrubbed as often as possible will improve the ETC and improve the understanding of the ETCs.

Innovate. AI tools are rapidly becoming capable of assuming skilled roles such as project analysts and can yield valuable insight. Tools are already available that can evaluate variances and variance analysis reports (VARs). Poor quality analysis translates to poor quality ETCs. Take action that supports improved analysis.

At a higher level, with the publication of the EIA-748-E Standard for EVMS revised 27 guidelines along with the evolving regulatory environment discussed in a previous blog, Revitalizing Earned Value Management Systems, this is a perfect time to review current EVMS ETC/EAC processes. The EIA-748-E split the EIA-748-D Guideline 27 into two parts: EIA -748-E Guideline 20 focuses on the control account level EACs and Guideline 23 focuses on the project level EACs. The DoD EVMS Interpretation Guide (EVMSIG) for Revision E has been updated accordingly.

We recommend reviewing approved EVM System Descriptions to ensure existing content supports the EIA-748-E Guideline revised text as well as remapping content to the EIA-748-E Guidelines and applicable government guides such as the DoD’s updated EVMSIG. Take the time to determine whether the documented processes make sense. If project personnel are ignoring the current process, it may be an indication it needs a revisit; it may need to be simplified or redone.

Consider reviewing the schedule data quality assessment process. Are project schedules providing an accurate forecast of the time required to complete the remaining work effort? This includes assessing whether task duration estimates are realistic as discussed in another blog, Improving IMS Task Duration Estimates. The IMS is the first line of defense to identify the potential that a cost overrun issue is likely to occur.

Lastly, open communication is essential to ensure technical, schedule, or cost realized risks are visible to all stakeholders. What is certain in any project plan is that things will not go as planned. Success depends upon quickly identifying the root cause of an issue and correcting course to reduce or eliminate the impact.

Reminder of the Objective of the ETC/EAC

The ETC is the detailed step-by-step plan the CAM provides to show how the remaining work will be accomplished. The goal of maintaining a credible ETC and EAC is to verify an executable plan is being regularly updated to accomplish the remaining scope of work within the contract’s schedule, cost, and funding targets for internal management visibility and control. The customer must also have confidence in the contractor’s ability to deliver and meet the remaining contract objectives.

The best way to prevent an ETC/EAC process CAR is to ensure you have a useful established process personnel follow, and they know how to use the schedule and cost tools to consistently maintain quality schedule as well ETC and EAC data. H&A scheduling and earned value consultants have worked with numerous clients to design or enhance their ETC/EAC process. H&A also offers EVMS training workshops that include content on how to develop a realistic EAC. Regular EVMS training always helps to reinforce best practices. Call us today at (714) 685-1730 to get started.