I have read several Earned Value Management (EVM) reports, papers, and articles that debate what company organization should “own” EVM and the company’s Earned Value Management System (EVMS). These debates most often mention the finance department and program organization as common EVM “owners.” The majority opinion seems to be that because EVM is a program management best practice it belongs in the program organization. A minority opinion is that because EVM is denominated in dollars, schedule included, and because EVM reports are financial in nature, EVM belongs in the finance department. Before we dive into this debate, a summary of the responsibilities of a Chief Financial Officer (CFO) and the head of programs is useful. In the Company A and Company B examples to follow, both the CFO and the head of programs reported to the company president.

What are the duties of a Chief Financial Officer (CFO)?

A CFO has three duties; each measured in the time domain. The first duty of the CFO is as the company’s controller and is responsible to accurately and honestly report past company financial performance. The CFO is also responsible for the current financial health of the company – to ensure that today’s decisions create rather than destroy value. And lastly, the CFO must protect the company’s future financial health and that all expenditures of capital maximize that future financial health. Every business decision, especially those of the CFO, are either good decisions (are accretive – increase shareowner value) or are bad decisions (are dilutive – destroys shareowner value).

What are the duties of the Head of Programs?

The head of programs is typically a Vice President or higher and all program and project managers report to them. The head of all programs has profit and loss responsibility for their portfolio of programs and projects. In addition, each program and project manager is responsible for achieving the technical, schedule, and cost requirements of the contracts they are executing on behalf of the company’s customers.

A Tale of Two Companies

I have first-hand experience with two companies and how each company decided who should “own” EVM that illustrates the nuances to these two approaches.

Company “A” had EVM assigned to the finance department. All EVM employees were overhead, even those assigned to a program. A new CFO arrived and quickly decided to reduce indirect costs, declaring that he was “coin-operated.” The new CFO terminated the employment of all EVM employees. Each program attempted to create an EVM branch office but failed. DCMA issued a Level 3 Corrective Action Request (CAR) detailing the EVMS deficiencies and the CFO was fired. A second new CFO arrived and agreed to transfer EVM to the head of programs. The head of programs was instrumental in changing the disclosure statement making EVM personnel assigned to a program a direct charge to that program or contract. The head of programs created a Program Planning and Control (PP&C) organization and demanded all Program Managers and their program members to quickly learn, use, and master EVM. A program control room was built with five screens. Daily 2 pm EVM data-driven reviews were held on short notice. These daily reviews became known as “CAM Bakes.” The EVM and program management culture changed quickly and dramatically at Company “A.”

Company “B” had EVM assigned to the CFO who was as “coin-operated” and unaware of EVM as was the first new CFO of Company “A.” The culture of company “B” was very hostile to EVM, so it probably did not matter who “owned” EVM. The company failed 16 of the EIA-748 Standard for EVMS 32 guideline requirements and they lost their DCMA approved EVMS status. Significant withholdings were imposed and the company’s reputation was damaged. Several top managers hostile to EVM sought employment elsewhere. A new CFO arrived who was also coin-operated – with one difference – the CFO was an expert in EVM. The new CFO formed a partnership with the head of programs. The new CFO was as much a program manager as he was a CFO. The new CFO told his direct reports assigned to each program to “make the program managers successful.” And they did exactly that.

The new CFO understood that the company was the sum of all its contracts and that every dollar flowed from its customers. The EVM and program management culture at Company “B” changed rapidly.

Who Should “Own” EVM? Programs or Finance?

Returning to our original question of who should “own” EVM, the majority theory is that the program organization should “own” EVM. All else being equal, I tend to agree with this theory.

However, while theory is suggestive, experience is conclusive. My experience at Company “A” proved that a strong program leader could rapidly change the EVM and program management culture of a company. My experience at Company “B” proved that a CFO could “own” EVM and be successful at changing the company’s EVM and program management culture. The CFO and the head of programs must form an EVM partnership no matter who “owns” EVM.

Who “owns” EVM at your company?

Mr. Kenney is a senior business executive with over 35 years of experience in the aerospace industry as well as over 10 years as a consultant to industry. He is an experienced practitioner of program management best practices as an Executive Vice President of Government Programs, Vice President of Naval Programs, and Program Manager at various aerospace and defense contractors. He is also a retired U.S. Marine Corps Colonel with 27 years of active and reserve duty.

As a result of an Earned Value Management System (EVMS) compliance or surveillance review, the Defense Contract Management Agency (DCMA) or DOE Office of Project Management (PM-30) may issue a corrective action request (CAR) to a contractor. H&A earned value consultants frequently assist clients with developing and implementing corrective action plans (CAPs) to quickly resolve EVMS issues with a government customer.

A recent trend our earned value management consultants have observed is an uptick in the number of CARs being issued related to over target baselines (OTB) and/or over target schedules (OTS). On further analysis, a common root cause for the CAR was the contractors lacked approval from the contracting officer to implement the OTB and/or OTS even though they had approval from the government program manager (PM).

So why was a CAR issued? It boils down to knowing the government agency’s contractual requirements and EVMS compliance requirements.

What is an OTB/OTS and when it is used?

During the life of a contract, significant performance or technical problems may develop that impact schedule and cost performance. The schedule to complete the remaining work may become unachievable. The available budget for the remaining work may become decidedly inadequate for effective control and insufficient to ensure valid performance measurement. When performance measurement against the baseline schedule and/or budgets becomes unrealistic, reprogramming for effective control may require a planned completion date beyond the contract completion date, an OTS condition, and/or a performance measurement baseline (PMB) that exceeds the recognized contract budget base (CBB), an OTB condition.

An OTB or OTS is a formal reprogramming process that requires customer notification and approval. The primary purpose of formal reprogramming is to establish an executable schedule and budget plan for the remaining work. It is limited to situations where it is needed to improve the quality of future schedule and cost performance measurement. Formal reprogramming may be isolated to a small set of WBS elements, or it may be required for a broad scope of work that impacts the majority of WBS elements.

Formal reprogramming should be a rare occurrence on a project and should be the last recourse – all other management corrective actions have already been taken. Typically, an OTB/OTS is only considered when:

The contract is at least 35% complete with percent complete defined as the budgeted cost for work performed (BCWP) divided by the budget at completion (BAC);

Has more than six months of substantial work to go;

A significant determining factor before considering to proceed with a formal reprogramming process is the result from conducting a comprehensive estimate at completion (CEAC) where there is an anticipated overrun of at least 15 percent for the remaining work.

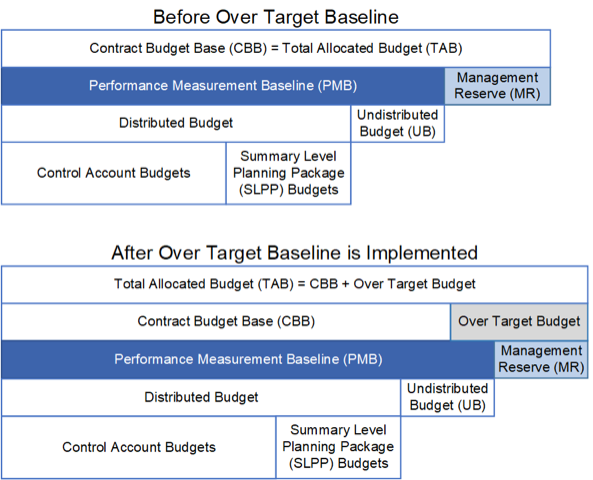

When an OTB is approved, the total allocated budget (TAB) exceeds the CBB, this value referred to as the over target budget. Figure 1 illustrates this.

Figure 1 – Over Target Baseline Illustration

When an OTS is approved, the same rationale and requirements for an OTB apply. The planned completion date for all remaining contract work is a date beyond the contract completion date. The purpose of the OTS is to continue to measure the schedule and cost performance against a realistic baseline. The process must include a PMB associated with the revised baseline schedule. Once implemented, the OTS facilitates continued performance measurement against a realistic timeline.

Contractual Obligations

An OTB does not change any contractual parameters or supersede contract values and schedules. An OTS does not relieve either party of any contractual obligations concerning schedule deliveries and attendant incentive loss or penalties. An OTB and/or OTS are implemented solely for planning, controlling, and measuring performance on already authorized work.

Should you encounter a situation where it appears your best option is to request an OTB and/or OTS, the DoD and DOE EVMS policy and compliance documents provide the necessary guidance for contractors. It is imperative that you follow agency specific guidance to prevent being issued a CAR or your OTB/OTS request being rejected.

DoD and DOE both clearly state prior customer notification and contracting officer approval is required to implement an OTB and/or OTS. These requirements are summarized the following table.

Reference

DoD/DCMA1

DOE

Regulatory

DFARS 252.234-7002 Earned Value Management System “(h) When indicated by contract performance, the Contractor shall submit a request for approval to initiate an over-target baseline or over-target schedule to the Contracting Officer.”

Guide 413.3-10B Integrated Project Management Using the EV Management System 6.1.2 Contractual Requirements. “…if the contractor concludes the PB TPC and CD-4 date no longer represents a realistic plan, and an over-target baseline (OTB) and/or over-target schedule (OTS) action is necessary. Contracting officer approval is required before implementing such restructuring actions…” Attachment 1, Contractor Requirements Document “Submit a request for an Over-Target Baseline (OTB) or Over-Target Schedule (OTS) to the Contracting Officer, when indicated by performance.”

EVMS Compliance2

Earned Value Management System Interpretation Guide (EVMSIG)3 Guideline 31, Prevent Unauthorized Revisions, Intent of Guideline “A thorough analysis of program status is necessary before the consideration of the implementation of an OTB or OTS. Requests for establishing an OTB or an OTS must be initiated by the contractor and approved by the customer contracting authority.

EVMS Compliance Review Standard Operating Procedure (ECRSOP), Appendix A, Compliance Assessment Governance (CAG) Subprocess G. Change Control G.6 Over Target Baseline/Over Target Schedule Authorization “An OTB/OTS is performed with prior customer notification and approval.” See Section G.6 for a complete discussion on the process.

Contractor EVM SD4

DCMA Business Process 2 Attachment, EVMS Cross Reference Checklist (CRC), Guideline 31. “b. Are procedures established for authorization of budget in excess of the Contract Budget Base (CBB) controlled with requests for establishing an OTB or an OTS initiated by the contractor, and approved by the customer contracting authority?”

DOE ESCRSOP Compliance Review Crosswalk(CRC), Subprocess Area and Attribute G.6 “Requests for establishing an OTB or an OTS are initiated by the contractor and approved by the customer contracting authority.”

Notes:

When DoD is the Cognizant Federal Agency (CFA), DCMA is responsible for determining EVMS compliance and performing surveillance. DCMA also performs this function when requested for NASA.

Along with the related Cross Reference Checklist or Compliance Review Crosswalk, these are the governing documents the government agency will use to conduct compliance and surveillance reviews.

For additional guidance, also see the DoD EVM Implementation Guide (EVMIG) , Section 2.5 Other Post-Award Activities, 2.5.2.4 Over Target Baseline (OTB) and Over Target Schedule (OTS). The EVMIG provides more discussion on the process followed including the contractor, government PM, and the contracting authority responsibilities.

Your EVM System Description (SD) should include a discussion on the process used to request an OTB/OTS. The EVM SD content should be mapped to the detailed DCMA EVMS guideline checklist or the DOE Compliance Review Crosswalk (subprocess areas and attributes) line items.

Best Practice Tips

The best way to avoid getting a CAR from a government agency related to any OTB or OTS action is to ensure you have done your homework.

Verify your EVM SD, related procedures, and training clearly defines how to handle this situation. These artifacts should align with your government customer’s EVMS policy and regulations as well as compliance review guides, procedures, and checklists. Be sure your EVM SD or procedures include the requirement to notify and gain approval from thegovernment PM and contracting officer, as well as what to do when the customer does not approve the OTB or OTS. Also discuss how to handle approving and managing subcontractor OTB/OTS situations; the prime contractor is responsible for these actions. Your EVMS training should also cover how to handle OTB/OTS situations. Project personnel should be aware of contractual requirements as well as your EVMS requirements and be able to demonstrate they are following them.

Maintain open communication with the customer. This includes the government PM as well as the contracting officer and any other parties involved such as subcontractors. Requesting an OTB or OTS should not be a surprise to them. Verify a common agreement has been reached with the government PM and contracting officer that implementing an OTB or OTS is the best option to provide visibility and control for the remaining work effort.

Verify you have written authorization from the government PM and the contracting officerbefore you proceed with implementing an OTB or OTS. You will need this documentation for any government customer EVMS compliance or surveillance review. Your baseline change requests (BCRs) and work authorization documents should provide full traceability for all schedule and budget changes required for the formal reprogramming action.

Does your EVM SD or training materials need a refresh to include sufficient direction for project personnel to determine whether requesting an OTB or OTS makes sense or how to handle OTB/OTS situations? H&A earned value consultants frequently help clients with EVM SD content enhancements as well as creating specific procedures or work instructions to handle unique EVMS situations. We also offer a workshop on how to implement an OTB or OTS . Call us today at (714) 685-1730 to get started.

Originally published March 2023 | Revised May 13, 2026

Quick Summary

EVMS compliance and surveillance reviews continue to identify issues related to poor-quality estimates at completion (EAC), underscoring the need for credible EACs to support effective project management, financial integrity, customer confidence, and funding decisions.

Credible EACs require actively maintained, data-driven estimates to complete (ETCs) that integrate schedule, resource, cost, and risk information along with regular management realism assessments and open communications with all stakeholders.

Organizations can improve EAC credibility by avoiding management imposed targets, keeping schedule and cost systems aligned, routinely reviewing the quality of the ETC data, leveraging evolving tools and analytics, and updating processes to align with the revised EIA-748-E guidelines.

The Defense Contract Management Agency (DCMA) as well as other government entities responsible for Earned Value Management System (EVMS) compliance and surveillance continue to identify issues with the quality of contractor estimates at completion (EAC). Using DCMA statistics, EIA-748-D Guideline 27, Maintain Estimates at Completion, is one of three guidelines1 that represent a third of all EVMS Corrective Action Requests (CARs).

Why Credible EACs Matter

A credible EAC is essential to all stakeholders and a foundation for managing projects successfully. Executive management and project managers must have a complete and accurate understanding of the projected contract or project EAC to ensure financial data is not misrepresented (Sarbanes-Oxley). The customer must have confidence in a contractor’s forecast completion date (FCD) and EAC data to understand whether the remaining work can be completed within the contractual period of performance and target cost, or, if not, how long it will take and how much it will cost.

When the most likely EAC exceeds the negotiated contract cost, the contractor’s profit margins may be at risk. Should the most likely EAC exceed the customer’s funding limit, they will need to secure additional funding, modify the work scope, or slow the pace of the project. No one likes schedule or cost surprises.

What determines whether an EAC is credible?

A credible EAC reflects the cumulative to date actual costs of work performed (ACWP) (costs the contractor has already incurred) plus the current ETC. The ETC must provide a realistic estimate of the time and resources required to complete the remaining authorized work using projected rates. It represents the time phased estimate of spending which translates to the future funds required.

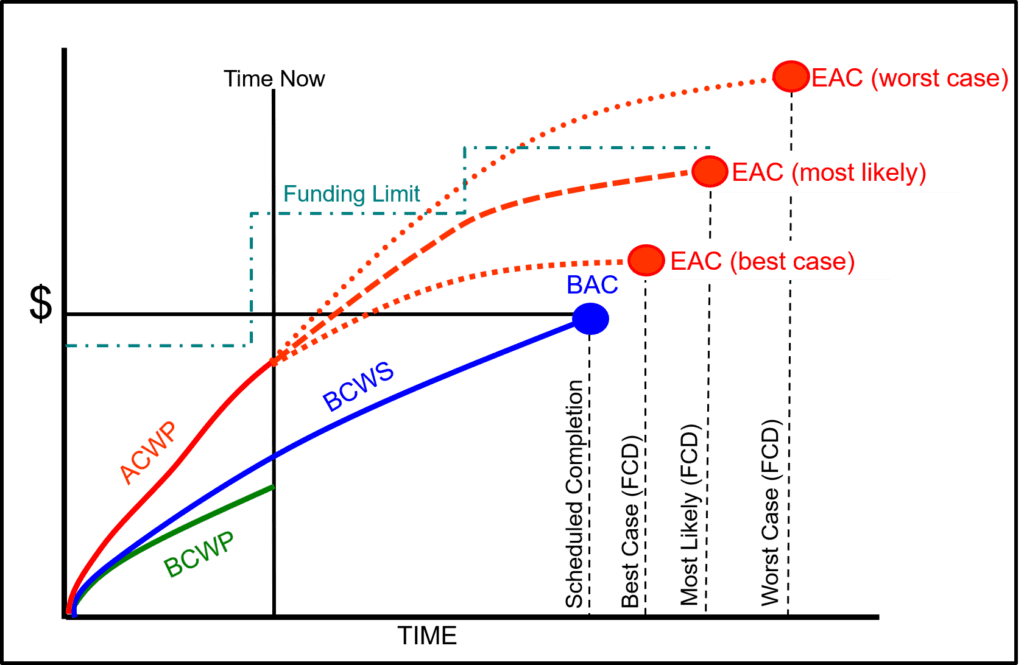

EACs should be based on actual costs and performance to date, the nature and amount of remaining scope, assumptions about and projections of future performance for that scope, risks and opportunities, economic escalation, expected direct and indirect rates, subcontract, and material commitments. As illustrated in Figure 1, project managers should routinely evaluate their project’s ACWP, ETC, and range of EACs along with the funding profile to verify amounts expended and forecasted are within the parameters of available contract funds.

Figure 1: Range of Project EACs with Funding Profile

What project control practices help to ensure EACs are realistic?

Three recommended best practices include:

Actively maintaining the detail ETC data every reporting cycle. This starts with updating the current schedule to include all authorized remaining scope along with the resource loaded activities to reflect performance to date and the latest planning (timing and resource requirements) for work in progress and future work effort. This is the basis for updating the time phased cost estimate for in progress work packages that is added to the cumulative to date actual costs as well as the cost estimate for future work/planning packages. Subcontract forecasted schedules and cost must be included. The current schedule forecast dates and time phased cost estimate must be aligned. Actively maintaining the detail data ensures the current schedule and ETC data reflect the project’s current state. The control account managers (CAMs) can substantiate their ETC with relevant data for analysis and take action to address a significant variance at completion (VAC).

Actively monitoring project FCDs and EACs. Project managers that routinely maintain a range of data driven FCDs and EACs (best case, most likely, and worst case) are better prepared to verify the control account FCDs and EACs are realistic, realized risks have been handled, and emerging risks have been identified, assessed, and addressed. Experienced practitioners use various metrics such as comparing the Cost Performance Index (CPI) to the To Complete Performance Index (TCPI) to test the realism of the EAC. They also include a realism check of the baseline and current integrated master schedule (IMS) to identify any potential disconnects with the cost-based indices discussed in a previous blog, Incorporating IMS Information Directly into IEAC Formulas. Managers should scrub the detail ETCs to assess the quality of the estimates and verify the content of the backup data. A good understanding of the detail ETCs is necessary to produce credible project level EACs with crisp rationale and narratives provided to executive management and the customer.

Maintaining open communications with all levels of management, subcontractors, and the customer. The project manager is the main conduit to manage impacts to their project’s FCD and EAC such as when finance changes direct or indirect rates, there are changes in resource availability or a spike in material prices, or the customer modifies the work scope or funding. As a result, project personnel can quickly handle issues or project changes. Direct and open communications with executive management ensures there is a clear understanding of their project’s FCD and EAC.

What are some things to avoid?

H&A consultants often observe practices that negate the value of maintaining the ETC/EAC and can result in an EVMS corrective action request (CAR). The root cause often points to ad-hoc processes or corporate culture. Examples:

Management provides a target FCD and EAC number the CAMs must match. The ETC/EAC should be “the voice of the CAM”. The CAM is saying “if you give me these resources as scheduled, I can finish the job this way.” Any approach that does not respect the voice of the CAM can cause the ETC/EAC to be unrealistic or at least unsubstantiated. Giving the CAM “the date and number” increases the likelihood the FCD and ETC are unrealistic. There may be a valid reason for this directive as a management what-if exercise or to gain a deeper understanding of the situation. When done as a routine management strategy, it diminishes the value of the ETC data to manage the project’s remaining work and prevent cost overruns. The CAMs should be in a position where they can substantiate their schedule timeline, resource requirements, and cost estimate to complete the remaining work. Project managers should be in a position where they can verify the detail ETC/EAC data to establish a level of confidence in their project level EACs they provide to executive management and the customer.

Project personnel take the path of least resistance. This is often an indication of a lack of direction or an established process. They either do not create the ETC data or maintain it on a routine basis. In some instances, the CAMs manage their ETC data to avoid oversight. An old but valid saying is “the tall grass gets mowed” – the CAM purposely doesn’t raise their ETC to a value that would attract attention. Another troublesome approach is to set a cost management tool option to a static EAC; the CAM may manually update the EAC number quarterly at best. The result? The FCD and ETC data isn’t current; there is zero insight into potential emerging issues. DCMA or the customer can easily identify this when they analyze the time-phased ETC data in the Integrated Program Management Data and Analysis Report (IPMDAR) Contract Performance Dataset (CPD) submittal.

Schedule and cost are created/maintained separately. This often occurs when the schedule and cost tools are not kept in sync for the project’s duration. Significant effort may go into ensuring the data are in alignment to establish the performance measurement baseline (PMB). The IMS resource loaded activities are used as the basis for the time phased budget baseline in the cost tool. However, the ETC data in the current schedule may not exist or be actively maintained. Project personnel only maintain the ETC data in the cost tool and fail to verify it aligns with the current schedule activity forecast dates and resource requirements. It is not part of their routine status and analysis process every month.

Taking Action to Review and Enhance Current Processes

A simple step to start with is to use the IMS Current Execution Index (CEI). This is a useful measure of how well a team can forecast just a single month into the future. If a team cannot achieve a high accomplishment rate against just a one-month forecast, any longer-term ETC is questionable. Start simple and focus on improving the one-month accuracy then move on to longer periods. Build confidence in the team’s ability to see and manage the future.

Another basic step. Build time into the process for managers to scrub ETCs. Maybe it is not possible to scrub every control account ETC every reporting period, but a rotational approach where ETCs are scrubbed as often as possible will improve the ETC and improve the understanding of the ETCs.

Innovate. AI tools are rapidly becoming capable of assuming skilled roles such as project analysts and can yield valuable insight. Tools are already available that can evaluate variances and variance analysis reports (VARs). Poor quality analysis translates to poor quality ETCs. Take action that supports improved analysis.

At a higher level, with the publication of the EIA-748-E Standard for EVMS revised 27 guidelines along with the evolving regulatory environment discussed in a previous blog, Revitalizing Earned Value Management Systems, this is a perfect time to review current EVMS ETC/EAC processes. The EIA-748-E split the EIA-748-D Guideline 27 into two parts: EIA -748-E Guideline 20 focuses on the control account level EACs and Guideline 23 focuses on the project level EACs. The DoD EVMS Interpretation Guide (EVMSIG) for Revision E has been updated accordingly.

We recommend reviewing approved EVM System Descriptions to ensure existing content supports the EIA-748-E Guideline revised text as well as remapping content to the EIA-748-E Guidelines and applicable government guides such as the DoD’s updated EVMSIG. Take the time to determine whether the documented processes make sense. If project personnel are ignoring the current process, it may be an indication it needs a revisit; it may need to be simplified or redone.

Consider reviewing the schedule data quality assessment process. Are project schedules providing an accurate forecast of the time required to complete the remaining work effort? This includes assessing whether task duration estimates are realistic as discussed in another blog, Improving IMS Task Duration Estimates. The IMS is the first line of defense to identify the potential that a cost overrun issue is likely to occur.

Lastly, open communication is essential to ensure technical, schedule, or cost realized risks are visible to all stakeholders. What is certain in any project plan is that things will not go as planned. Success depends upon quickly identifying the root cause of an issue and correcting course to reduce or eliminate the impact.

Reminder of the Objective of the ETC/EAC

The ETC is the detailed step-by-step plan the CAM provides to show how the remaining work will be accomplished. The goal of maintaining a credible ETC and EAC is to verify an executable plan is being regularly updated to accomplish the remaining scope of work within the contract’s schedule, cost, and funding targets for internal management visibility and control. The customer must also have confidence in the contractor’s ability to deliver and meet the remaining contract objectives.

The best way to prevent an ETC/EAC process CAR is to ensure you have a useful established process personnel follow, and they know how to use the schedule and cost tools to consistently maintain quality schedule as well ETC and EAC data. H&A scheduling and earned value consultants have worked with numerous clients to design or enhance their ETC/EAC process. H&A also offers EVMS training workshops that include content on how to develop a realistic EAC. Regular EVMS training always helps to reinforce best practices. Call us today at (714) 685-1730 to get started.

In part one of our series on Elements of Cost (EOC), we explained what EOCs are and gave an analogy of how EOCs would relate to building a patio. We also reviewed how EOCs can be “over thought” and emphasized the importance of properly applying indirect cost rates. This post is going to be focused on the Over-Application of EOCs.

Over-Application of EOCs

During some government reviews, the teams issued Corrective Action Requests (CARs) citing multiple examples of ACWP occurring on “zero-budgeted” Work Packages within Control Accounts. On the surface, this sounds pretty serious, but there were several “over-applications” in play here.

First, the review was being performed at (and in some cases below) the Work Package (WP) level, when the intent of the Guidelines has always been for variance analysis to be performed at the Control Account (CA) Level;

Second, the CAR assumption was that a charge against an Element Of Cost (EOC) equals a charge against a “zero-budgeted WP”.

For the first point we’ll look at Guideline 22 in the EVM Standard 748:

GL 22. At least on a monthly basis, generate the following information at the Control Account and other levels as necessary for management control using actual cost data from, or reconcilable with, the accounting system:

1) Comparison of the amount of planned budget and the amount of budget earned for work accomplished. This comparison provides the schedule variance.

2) Comparison of the amount of the budget earned and the actual direct costs for the same work. This comparison provides the cost variance.

Even the government’s sub-question e. under GL 22 reiterates this requirement:

e. Are the following elements for measuring performance available at the levels selected for control and analysis (at a minimum at the control account level):

While the intent of the words “and other levels” and “at a minimum” was to ensure that contractors did not only perform analysis at some higher, summary level, the government’s choice of those sub-question words also opens up the application of the analysis at lower levels. Be that as it may, the over-application still exists where it should not. Variance Analysis is supposed to be at the CA level and rolled up to higher levels for analysis. The bottom line for each of the CARs written is that BCWS, BCWP, and ACWP existed at the Control Account level, and the EOC visibility was available for variance analysis explanations at the lower levels in the contractors’ systems.

For the second point, let’s look at all the EVM Standard 748 Guidelines, specifically Guideline 16.

There is no Guideline that specifically requires BCWP to be claimed the exact same way BCWS was planned; however, it is intuitive that this has to be true in order for cumulative values for BCWP and BCWS to equal BAC so that the work can be considered complete. [While the government’s sub-question b. under Guideline 22 expects BCWP to be calculated “consistent with the way the work is planned”, GL 22 itself (above) is silent on that inferred expectation.] The Guideline 16 and its sub-question b. also require consistency of the direct costs:

GL 16. Record direct costs in a manner consistent with the budgets in a formal system controlled by the general books of account.

Are elements of direct cost (labor, material, subcontractor, and other direct costs) accumulated within control accounts in a manner consistent with budgets using recognized acceptable costing techniques and controlled by the general books of account?

In the examples noted for the CAR referenced above, the work package task was a specific Element Of Cost (EOC) and was planned and completed in the same period, but no ACWP was accumulated for that specific EOC because the work was accomplished using another resource that fell into another EOC category. When the team looked at that EOC containing the ACWP, they interpreted the finding as a “zero-budgeted Work Package” with ACWP against it. [They also cited the original Work Package itself for having BCWP with no ACWP for the element of cost that was planned and earned.]

In EVM Consulting, we deal with Corrective Action Requests (CARs) on a regular basis, so we have plenty of real-world experience. We created an outline of valuable information about DRs / CARs based on our collective experience. Part 1 of the guide is designed to inform you of why CARs are received and who issues them, so you can work to prevent them. Part 2 will prepare you to respond to a CAR in an effective and efficient way.

In Part 1 of the series we illuminated the varied sources of Corrective Action Requests: 1) Standard Surveillance Instruction (SSI) 2) Agencies that do not use the DCMA for surveillance, such as the Department of Energy. 3) Integrated Baseline Review (IBR) 4) Procedures that are compliant with the EIA-748 Guidelines 5) Contract Performance Report (CPR) 6) Integrated Project Management Report (IPMR) 7) Integrated Master Schedule (IMS) 8) Discrepancy Reports (Levels I-IV)

In part 2 of the series, we addressed responding to a Corrective Action Request (CAR): 1) Review the DRs/CARs with the customer 2) Organize for successful CAP management 3) Begin a thorough Root Cause Analysis 4) Develop and evaluate Corrective Action Plans 5) Develop verification closure steps 6) Develop a detailed Integrated Master Schedule for CAP implementation 7) Submit CAP and CAP IMS to the customer for approval prior to implementing the Corrective Actions 8) Implement Corrective Action Plans and track progress to successful completion 9) CAR closure and follow-up

I’ll answer this provocative question now. DCMA, local and headquarters, are an EVM contractor’s “friend” with remarkable, but not unlimited, patience. When required, DCMA can become the contractor’s “tough love” friend.

DCMA and the contractor share the same interests – successful contract performance. DCMA is part of a triad that includes the Government’s program team, the contractor’s program team and their DCMA counterparts.

The title “Defense Contract Management Agency” reminds me of “grilled cheese sandwich” – the recipe and the product are in the name – “contract management” leads to well managed contracts.

EAC Vignette – Part One:

Contractor A has learned that their collocated DCMA has concerns about the company’s EAC process and resulting declared EACs. The company has learned that a Level III CAR on GL # 27 is being considered. Contractor A’s senior management decides to replace their EVM Core Leader with “new blood” to improve the company’s “relationship” with DCMA and avoid a Level III CAR.

Contractor A’s new EVM leader meets with her team and with the program managers that have an EVM contractual requirement. Company A’s new EVM leader is told that DCMA’s EAC concerns are a new issue. The company’s new EVM leader asks to meet with her DCMA counterpart to discuss their GL # 27 concerns, and to present a draft of a Corrective Action Plan (CAP).

During the meeting with DCMA’s EVM leader she mentions that the EAC concerns were a surprise to the company. The company’s new EVM leader briefs her draft CAP to her DCMA counterpart.

After the draft CAP has been briefed, the DCMA EVM leader comments, “your draft CAP is a good start. After I have time to fully digest your draft CAP I will send my comments and suggestions. As for being surprised by our EAC concerns, here is a file with 3+ years of letters, emails, meeting minutes from DCMA to your company outlining our continuing and growing concerns with your company’s EAC process.”

EAC Vignette – Part Two:

DCMA issued a Level III Corrective Action Request (CAR) to the contractor and is considering withholdings as an incentive for the company to quickly improve their EAC processes.

As promised, the DCMA EVM leader sent the following note to the company’s new EVM leader:

“I sent your draft GL # 27 CAP to my team for their comments and recommendations. My team’s key recommendations are:

1). Identify the weaknesses in your existing EAC processes. For each weakness, identify a corrective action. As much as possible, “mistake proof” your new processes. You should consider a review of several 100% complete contracts, and “replay” those contracts month-by-month using your new EAC processes to test their effectiveness.

2). As noted in our CAR, the company is required to report progress on the Corrective Action Plan (CAP). You should treat your CAP as a program. At a minimum, you should have an IMS and use appropriate earned value techniques to measure progress.

3). A sister division in your parent corporation, has a very mature and effective EAC process. You should considering asking for their assistance as you develop your CAP and begin its execution.

4). If you have questions as you execute your CAP, please don’t hesitate to contact me. If I don’t know the answer to your question, I’ll find someone that does know the answer and will share it with you.”

Personal Observations:

Based on my 32 years as an employee of defense contractors, and 7 years in earned value consulting, I offer the following:

1). DCMA “local” knows your company much better than you might think.

2). DCMA “headquarters” has knowledge and insight into many companies. From DCMA’s website: “We are the independent eyes and ears of DoD and its partners, delivering actionable acquisition insight from the factory floor to the front line …. around the world.”

3). A CAR from DCMA informs the company of “what” needs corrected but not “how” to correct the issue. That said, DCMA knows what will or will not work. Maintain a dialogue with DCMA.

4). “Compliance” is a lower bound for performance. DCMA will not object if a company decides to improve well beyond mere compliance.

5). Please consider the possibility that what may appear to be a “new” problem for your company, may have already been solved by another company. Find who has already solved your “new” problem. Ask for help.

(1)")